Xu Gao: The Future of Money, and China’s Choices

Chief Economist of Bank of China International argues China should expand the renminbi payment network while avoiding the heavy costs of reserve-currency dominance.

This is a very long article, so readers may wish to start with the brief summary below and the author’s own summary at the beginning of the article.

Xu Gao, Chief Economist of Bank of China International (China) Co., Ltd., examines the future of the international monetary system at a time when confidence in the dollar-centred Jamaica system is under growing strain. He argues that neither a return to gold or commodity backing, nor a eurozone-style single-currency area, nor sovereignless cryptocurrencies can provide a viable foundation for the next international monetary system. The more plausible long-term path, in his view, is the emergence of a supranational currency linked to a basket of sovereign currencies, gradually replacing the dollar’s central role in international payments.

For China, Xu argues, the priority should not be to overturn the dollar-centred system prematurely or to make renminbi internationalisation a bid to replace the dollar. China still benefits from the external-demand space created by global imbalances under the current system. Preserving the existing system, at least for now, helps China absorb some of the adjustment pressure created by insufficient domestic demand and excess supply. At the same time, making the renminbi the main international reserve currency brings costs that far outweigh the benefits.

Xu therefore argues that China should focus on securing international payment channels, expanding the renminbi payment network, developing mechanisms such as currency swaps and overdraft arrangements to supply renminbi liquidity, and supporting the longer-term development of a supranational currency through SDR reform or proposals such as a BRICS currency.

The article was originally published on 25 May 2026 on Xu’s personal WeChat blog 徐高经济观察 Xu Gao Economic Observation.

Xu has kindly authorised and reviewed the translation.

—Yuxuan Jia

国际货币体系的未来与中国的选择

The Futures of the International Monetary System and China’s Choices

The current dollar-centred international monetary system—the Jamaica system—has many flaws. Its main weaknesses are persistent global imbalances, the inequity created by the United States’ excessive issuance of dollars, and doubts over the system’s long-term sustainability. In recent years, U.S. unilateralism has further eroded global confidence in the dollar and shaken the foundations of the Jamaica system, prompting renewed debate over the future of the international monetary order.

To look ahead, one must first look back. Before the Jamaica system, the international monetary order had long been anchored to gold. Under gold-based arrangements, confidence in money was relatively easy to sustain, and trade imbalances among countries could be corrected automatically through cross-border gold flows. The dollar’s decoupling from gold in 1971, followed by the establishment of the Jamaica system, marked the transition from “anchored” to “unanchored” money. Once freed from the constraints of a physical anchor, monetary policy could be adjusted more freely and flexibly, thereby reducing volatility in the real economy. At the same time, monetary de-anchoring made global imbalances possible and, in turn, helped drive the expansion of globalisation. Any future international monetary system can replace the existing one only if it preserves the strengths of the Jamaica system while remedying its weaknesses.

Looking ahead, several scenarios for the future international monetary system can largely be ruled out: (1) a eurozone-style single-currency area among major economies; (2) a return to commodity-backed currencies or any other physical anchor; and (3) the rise of sovereignless cryptocurrencies as the main instruments of international payment. At the same time, the dollar’s network externalities give it a powerful incumbent advantage, making it highly difficult for any other sovereign currency to replace it at the centre of the system. Once these unlikely scenarios are excluded, the most plausible post-Jamaica path is a supranational currency linked to a basket of sovereign currencies, gradually replacing the dollar’s central role in international payments. The SDR is the embryonic form of such a currency, while proposals such as the BRICS R5 may also point in this direction.

In the long-term evolution of the international monetary system, China’s interests would be best served by the following choices. First, China should not seek to overturn the dollar-centred Jamaica system, from which it still benefits. Second, renminbi internationalisation should not aim to replace the dollar or make the renminbi the central currency of the international monetary system. Third, renminbi internationalisation should instead focus on ensuring that China has secure international payment channels and on expanding the renminbi payment network globally. Fourth, China should allow overdraft arrangements within the international renminbi payment system, thereby providing renminbi liquidity to other countries through the payment system itself. Fifth, China should support the development of a supranational currency linked to a basket of sovereign currencies, with a view to its eventually replacing the dollar as the main instrument of international payment.

In recent years, the rise of unilateralism, especially U.S. actions that have damaged the international economic and trading system, has put the current dollar-centred international monetary system, the Jamaica system, in turbulence. The unusual surge in gold prices since the second half of 2024 has reflected weakening international confidence in dollar-denominated assets. Against this backdrop, debate has intensified over the future of the international monetary system and possible alternatives to the dollar. But to look ahead, one must first look back. By reviewing the system’s historical evolution, this article seeks to identify the deeper forces behind its development and transformation, infer its possible future trajectory, and clarify the strategic choices China should make.

1. The Many Problems of the Existing International Monetary System

The “international monetary system” refers to the rules, conventions and institutions that enable cross-border trade, investment, capital flows, and other economic exchange. It determines the answers to several core questions: What should serve as international payment instruments and reserve assets? How are currencies exchanged, and how are exchange rates set? Should balance-of-payments disequilibria be corrected, and by what mechanisms? And how should international financial affairs be coordinated?

The current system took shape after the collapse of Bretton Woods in 1971. In 1976, IMF member states signed an agreement in Kingston, Jamaica, establishing the basic architecture of today’s international monetary order. It is therefore known as the Jamaica system1 and has several defining features.

First, it is a fiat-money system, in which the value of money rests entirely on public confidence. Under the Jamaica system, national currencies are not linked to gold or any other physical object, but derive their status as legal tender from government authority. Their purchasing power depends completely on belief. A government can require people to accept its currency, but it cannot fully determine what that currency can buy. If confidence collapses, fiat money will cease to function as a means of payment. In essence, fiat money works because people believe it can be used to buy goods and services, and because they believe others believe the same. This shared expectation gives fiat money real purchasing power, but it has no physical backing and depends entirely on sound policy management by the issuing country.

Second, fiat money gives governments an unconstrained capacity to create money in nominal terms. Since money is no longer tied to a physical anchor, its nominal supply is no longer subject to physical limits. Governments can create as much money as they wish. However, whether that money retains real purchasing power — that is, whether it can really buy stuff — is another matter. To preserve confidence and maintain the currency’s real purchasing value, the issuing government must use its money-creation capacity responsibly and keep monetary expansion aligned with real-economy conditions.

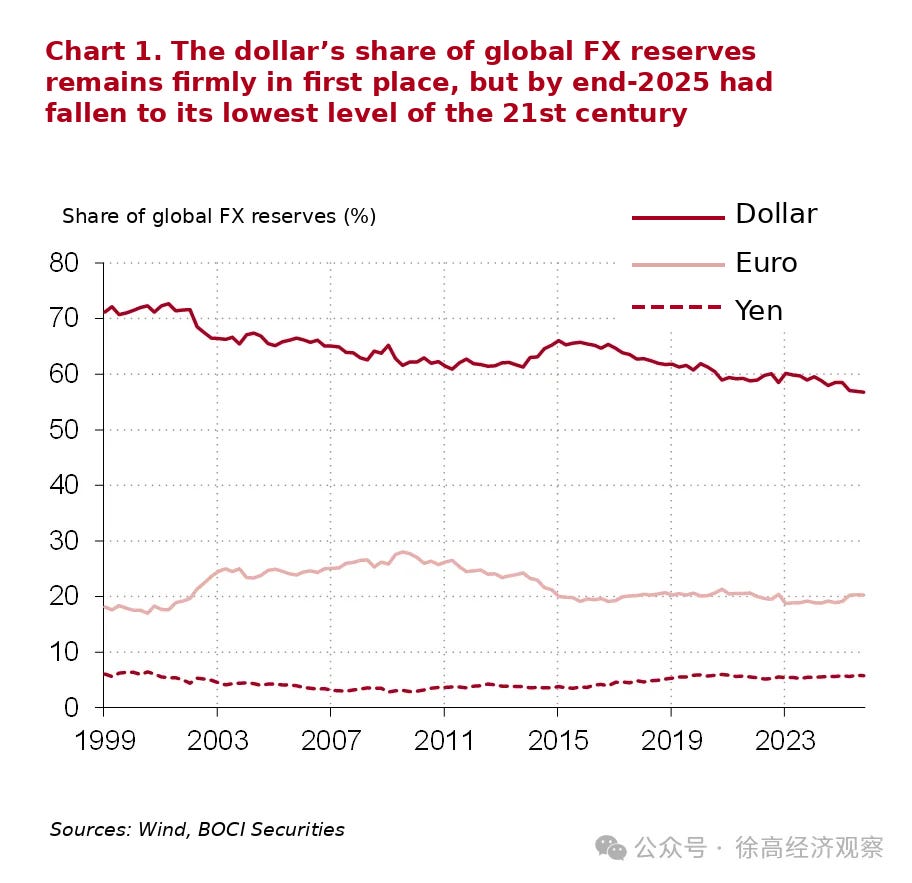

Third, the U.S. dollar remains the dominant currency for international payments and reserves. Under the postwar Bretton Woods system, the dollar was the only currency directly linked to gold, while other currencies were pegged to the dollar. This made the dollar the principal settlement currency in international trade and the preferred reserve asset for central banks. The Jamaica system inherited this dollar-centred structure. At the end of 2025, dollar-denominated assets still accounted for 56.8 per cent of global foreign-exchange reserves, the largest share by far and well ahead of the euro’s second-place share of 20.2 per cent. It is worth noting, however, that the dollar’s reserve share has been declining for the past decade and reached a new twenty-first-century low at the end of 2025. (See Chart 1)

Fourth, floating exchange rates have become the dominant arrangement. Under Bretton Woods, countries generally maintained fixed exchange rates, keeping currency conversion rates unchanged. Under the Jamaica system, floating exchange rates became the dominant arrangement. Currency conversion rates were allowed to fluctuate freely, giving countries a tool to respond to external shocks.

The Jamaica system has promoted globalisation, but it has also exposed a number of weaknesses. In the more than half-century since its establishment, it has contributed to widening global trade imbalances, facilitated the rise of globalisation, and witnessed major shifts in the global economic landscape. In the process, some of its shortcomings have become increasingly apparent.

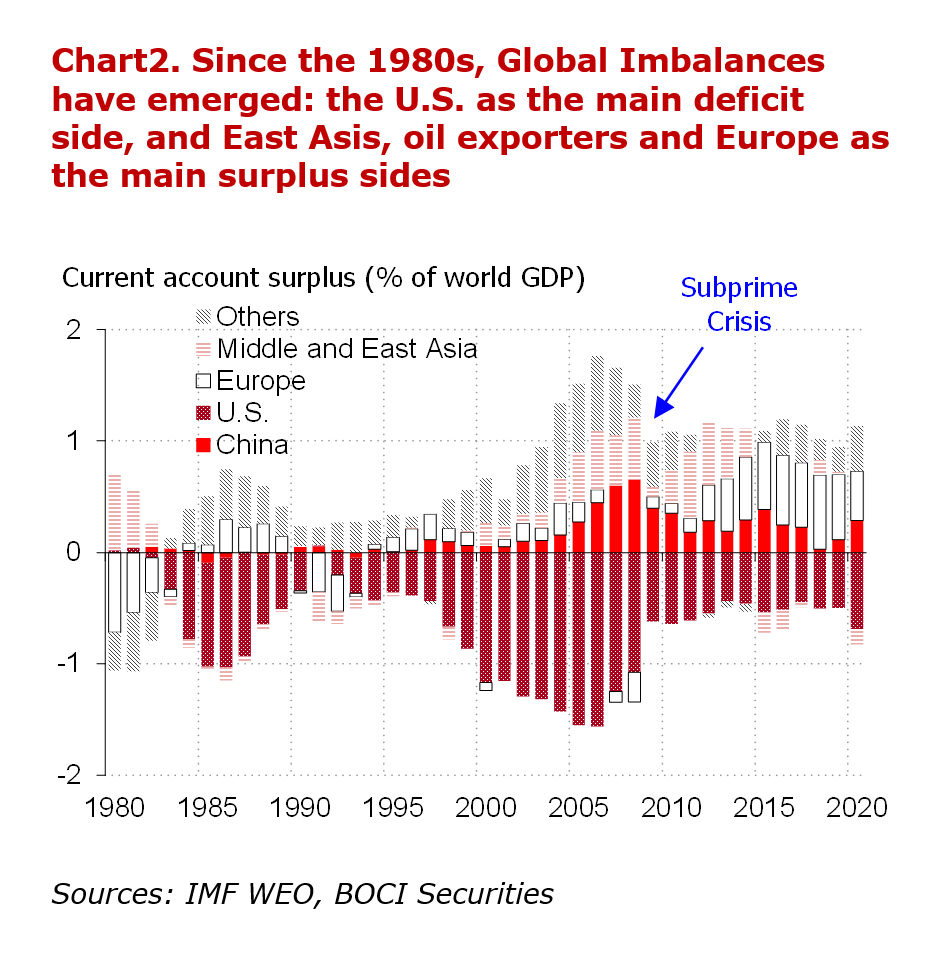

The first major weakness is the persistence of global imbalances. Since the 1980s, the world economy has settled into a pattern in which aggregate deficits and surpluses have both remained elevated, with the United States accounting for the overwhelming majority of global deficits. Under this pattern, goods and services flow continuously from surplus economies to the United States. Domestic structural imbalances mirror these external imbalances: the deficit-running United States has excess demand and insufficient supply, while surplus economies suffer from insufficient demand and excess supply. As discussed below, under a gold-standard-based international monetary system, trade imbalances would have been corrected automatically, and persistent global imbalances of this kind would not have arisen. By contrast, the Jamaica system’s inability to correct international trade imbalances automatically is one of its central defects. (See Chart 2)

The second major weakness is the inequity created by the United States’ excessive issuance of dollars. Under the Jamaica system, the dollar is the dominant currency for international transactions and reserves, generating enormous global demand. Because the dollar is no longer tied to any physical anchor, the United States has an unlimited capacity to create it in nominal terms. It can therefore extract seigniorage from the rest of the world by issuing dollars on a large scale. From 2001 to 2025, the United States ran cumulative current-account deficits of more than US$15 trillion. This represents the value of goods and services the United States obtained from the rest of the world using dollars. This ability to draw resources from the world through the dollar is the “exorbitant privilege” the currency gives the United States.2

The third major weakness is that, because of the “Fundamental Triffin Dilemma,” a dollar-centred international monetary system is difficult to sustain over the long run. In the January 2026 article “The ‘Fundamental Triffin Dilemma’ and the Rise and Fall of the Global Dollar Cycle,” I discussed the contradiction between “U.S. hegemony” and “U.S. dollar supremacy”: U.S. hegemony supports dollar supremacy, but dollar supremacy in turn erodes U.S. hegemony and ultimately leads to its own decline. This is what I call the “Fundamental Triffin Dilemma.” It means that international confidence in the dollar cannot be maintained indefinitely, and that a dollar-centred monetary system will eventually move toward self-negation.

In recent years, U.S. unilateralism has damaged global confidence in the dollar and shaken the Jamaica system. Since Donald Trump began his first presidential term in 2017, unilateralism has become increasingly pronounced in U.S. policy. Washington has increasingly treated international rules and institutions as constraints and has been more willing to bypass them. In April 2025, shortly after beginning his second term, Trump introduced a “reciprocal tariff” policy, agreesively imposing additional tariffs on countries around the world. This anti-globalisation move further weakened international confidence in dollar assets.3 The United States has also weaponised the dollar, turning the world’s leading payment currency into an instrument of sanctions against other countries.4 This has given other countries stronger incentives to search for alternatives.

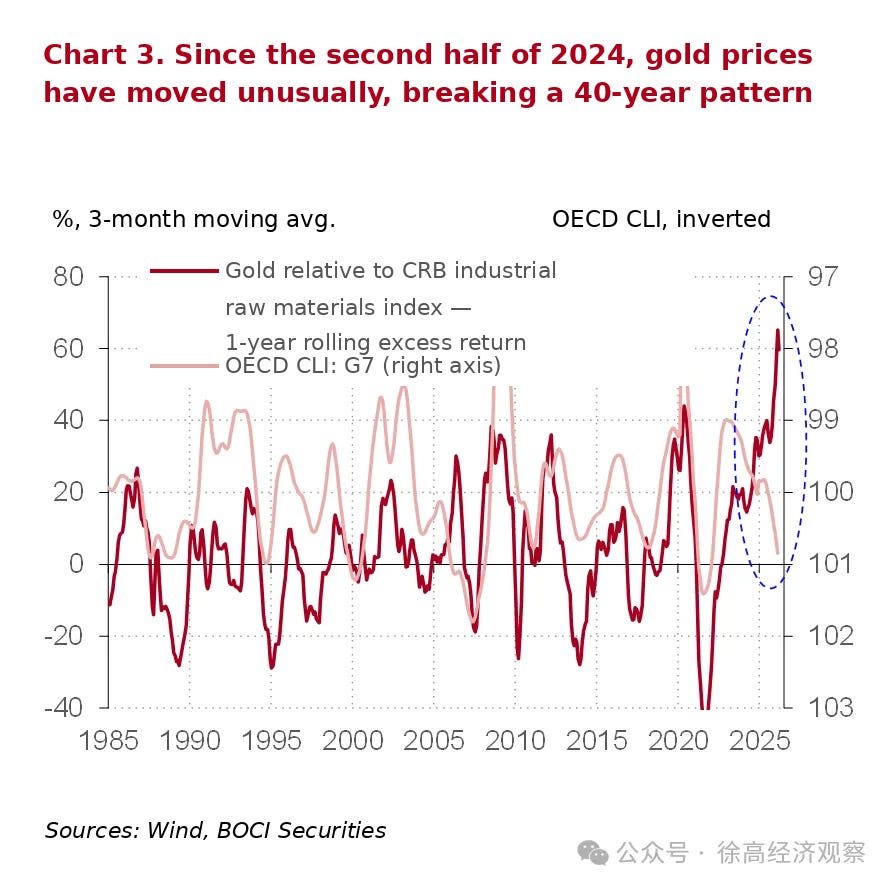

The unusual rise in gold prices since the second half of 2024 reflects declining international confidence in the dollar. After the dollar was decoupled from gold in 1971, gold lost its monetary role and became a special precious metal with safe-haven attributes. This safe-haven function is reflected in the countercyclical movement of gold prices relative to other commodities. Consider the one-year rolling outperformance of gold prices relative to the CRB industrial raw materials index. Over the past 40 years, this measure has been significantly negatively correlated with the OECD Composite Leading Indicator (CLI) for G7 Countries, a gauge of economic conditions. When the G7 economies strengthen, gold tends to underperform other commodities; when they weaken, gold tends to outperform. Since the second half of 2024, however, the OECD CLI has risen markedly, a situation in which gold should have underperformed. Instead, gold has significantly outperformed other commodities, producing a pattern not seen in four decades. Behind this unusual move is a decline in international confidence in the dollar and the conversion of some dollar-denominated assets into gold. (See Chart 3)

As the weaknesses of the Jamaica system become more apparent and international confidence in the dollar declines, more people are beginning to consider the future of the international monetary system. Long-term national development strategies and individual investment decisions alike must take its possible trajectory into account and prepare accordingly.

2. The Advantages and Disadvantages of Anchoring Money to Gold

Before looking ahead, one needs to look back. Before the Jamaica system, money had long been linked to gold. From the nineteenth century to the early twentieth century, the international monetary system operated under the gold standard, in which gold itself functioned as money. From the end of the Second World War to 1971, it operated under the Bretton Woods system, a variant of the gold standard known as the gold exchange standard. Under Bretton Woods, the dollar was linked to gold, while other currencies were linked to the dollar. To understand where the international monetary system may go after the Jamaica system, it is important to first understand how the earlier gold-anchored arrangements worked.

From the early nineteenth century to the early twentieth century, Western countries long operated under the gold standard, with the value of money anchored to gold. To avoid confusion, it is worth clarifying what “money” meant under this system. Gold itself was money, and gold coins could be used directly to purchase goods. But gold coins were inconvenient in everyday use, so money also took other forms, including bank notes and bank deposits. To say that money was linked to gold is to say that these other forms of money—especially paper money—derived their value from their link to gold.

Under the gold standard, Britain maintained the link between money and gold through three institutional arrangements: free coinage, free convertibility, and the free cross-border movement of gold. Free coinage meant that any citizen or institution could bring gold to the Royal Mint to be coined, and gold coins could also be melted back into bullion. Free convertibility meant that holders of banknotes and other non-gold forms of money could exchange them for gold at the statutory rate. In this sense, paper money under the gold standard was essentially a gold claim. This maintained the link between gold and other forms of money. The free cross-border movement of gold allowed gold to flow in and out of the country, keeping domestic and international gold prices aligned.

These three institutional arrangements locked together the values of gold, gold coins, and other forms of money. As a result, the total amount of money available to purchase goods in Britain—including both gold coins and other forms of money—was tied to the country’s gold reserves and could not be adjusted at will. In effect, monetary policy was placed in “golden handcuffs.” Governments accepted this self-imposed constraint because it imposed an external hard limit on the money supply and thereby helped stabilise public confidence in money.

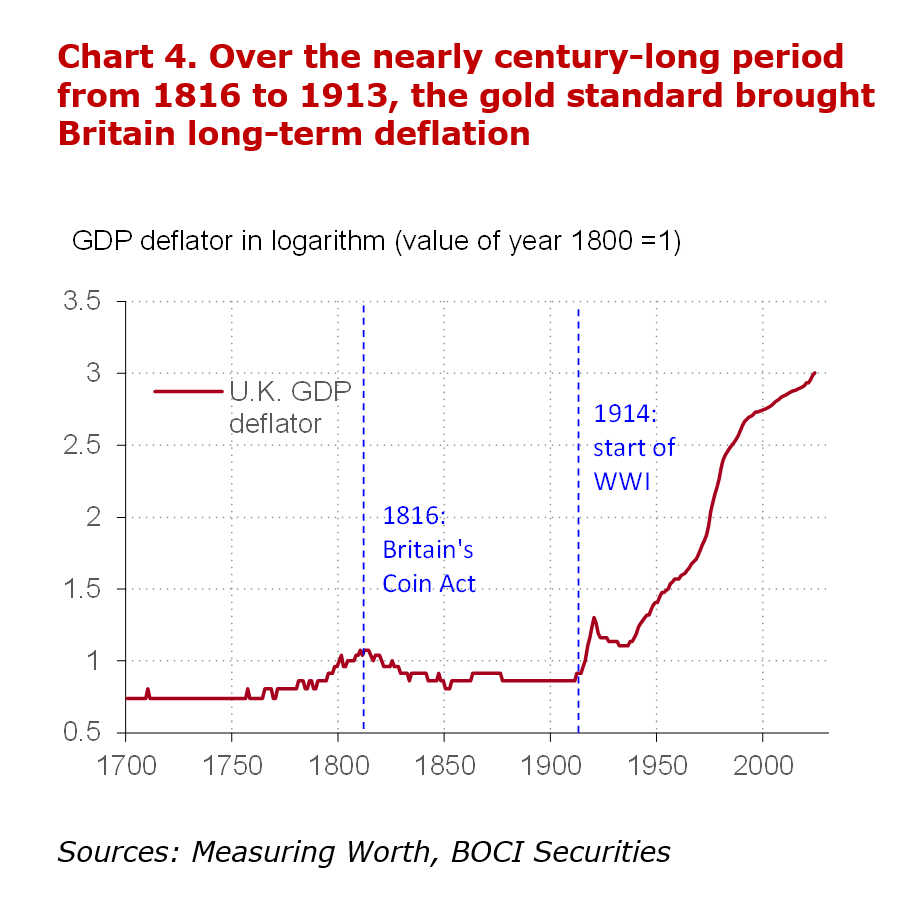

Under the gold standard, maintaining the credibility of money was relatively straightforward: as long as people trusted gold and believed that paper money could be converted into gold at any time, they would naturally trust paper money as well. In 1815, the British-led coalition defeated Napoleon at Waterloo, removing a formidable rival. But the high fiscal cost of the war with France, together with the excessive issuance of paper money, had pushed British prices sharply higher. To stabilise prices, Britain passed the Coinage Act 1816, setting the mint price for standard gold at £3 17s 10½d per troy ounce. This marked the beginning of Britain’s gold standard and brought the previous rise in prices under control.

Under the gold standard, governments largely lost the ability to manage the total quantity of money. Once the money supply was tied to domestic gold reserves, it was no longer at the government’s discretion but moved with the amount of gold held in the country. Banks could still create forms of money other than gold coins, including bank notes, but the quantity of such money was constrained by banks’ gold reserves and therefore ultimately by the amount of gold available.

To ensure the free convertibility of paper money into gold, governments required banks to hold gold reserves against the notes they issued. Britain’s Bank Charter Act 1844, for example, allowed the Bank of England to issue £14 million in notes backed by government securities rather than gold, but required every note issued beyond that limit to be backed by 100 per cent gold reserves. Similarly, the U.S. Gold Reserve Act of 1934 required the Federal Reserve to hold gold reserves equal to at least 40 per cent of the notes it issued. In this sense, under the gold standard, the amount of gold a country possessed roughly determined the size of its money supply, while money-supply growth was tied to the growth of gold holdings.

Under the gold standard, governments could expand the supply of paper money by devaluing it against gold, but doing so would undermine public confidence and therefore could not be used frequently. The U.S. Gold Reserve Act of 1934, for example, raised the official dollar price of gold from US$20.67 to US$35 per ounce. This reduced the gold content of each dollar to 59 per cent of its previous level, amounting to a 41 per cent depreciation of the dollar against gold. The devaluation allowed the United States to issue more paper money against the same level of gold reserves, thereby increasing the dollar money supply. But this was not a measure that could be repeated at will. Loosening the “golden handcuffs” could expand the money supply, but it would also weaken public confidence in money and could ultimately bring down the gold standard itself. Under that system, confidence in money rested primarily on the constraints that the “golden handcuffs” imposed on government money issuance.

Because the money supply under the gold standard was determined by gold reserves rather than real economy conditions, it could remain misaligned with the economy’s demand for money for extended periods. The supply of money was tied to the quantity of gold, while the demand for money was shaped by many factors, including the size of the economy, the stage of development and the volume of market transactions. The two did not necessarily match. When they diverged, the price level had to adjust to absorb the gap between money supply and money demand. Over the long term, the stock of gold generally grew more slowly than the economy. This was precisely why gold had value: its scarcity meant that its supply could not keep pace with economic development. When gold-stock growth remained below real economic growth for long periods, the gold standard produced sustained deflation. From the Coin Act 1816 to the eve of the First World War in 1913, Britain remained on the gold standard for almost a century. Over that period, its overall price level fell by a cumulative 18 per cent. (See Chart 4)

The “golden handcuffs” also constrained exchange rates. Because countries on the gold standard all linked their currencies to gold, exchange rates among them were fixed by gold parity. In 1871, for example, the German Reichstag passed the Coinage Act, stipulating that one mark contained 0.358423 grams of pure gold. At the same time, one pound sterling contained 7.32238 grams of gold. The exchange rate between the pound and the German mark was therefore 20.43 marks per pound, calculated as 7.32238 divided by 0.358423. This was the gold parity between sterling and the mark.

For countries on the gold standard, exchange rates were locked by gold parity, and gold moved freely across borders. Governments, therefore, could not use monetary policy to offset differences among national economies. Instead, internal and external imbalances were corrected automatically through cross-border gold flows. A country with insufficient domestic demand and excess supply would export its surplus output and earn gold from abroad. The resulting gold inflow would expand the surplus country’s domestic money supply and push up prices. Higher domestic prices would restrain exports and stimulate imports, narrowing the trade surplus. In the process, domestic demand in the surplus country would rise, as cheaper foreign goods encouraged consumption, while domestic supply would fall as weaker demand for local products restrained production. Conversely, a deficit country would experience gold outflows, monetary contraction and falling prices, which would narrow its trade deficit, reduce domestic demand and expand supply.

This gold-standard mechanism, under which cross-border gold flows automatically corrected economic imbalances, is known as the price-specie flow mechanism. Since it was first proposed by the Scottish philosopher David Hume, it is also known as the Hume mechanism.

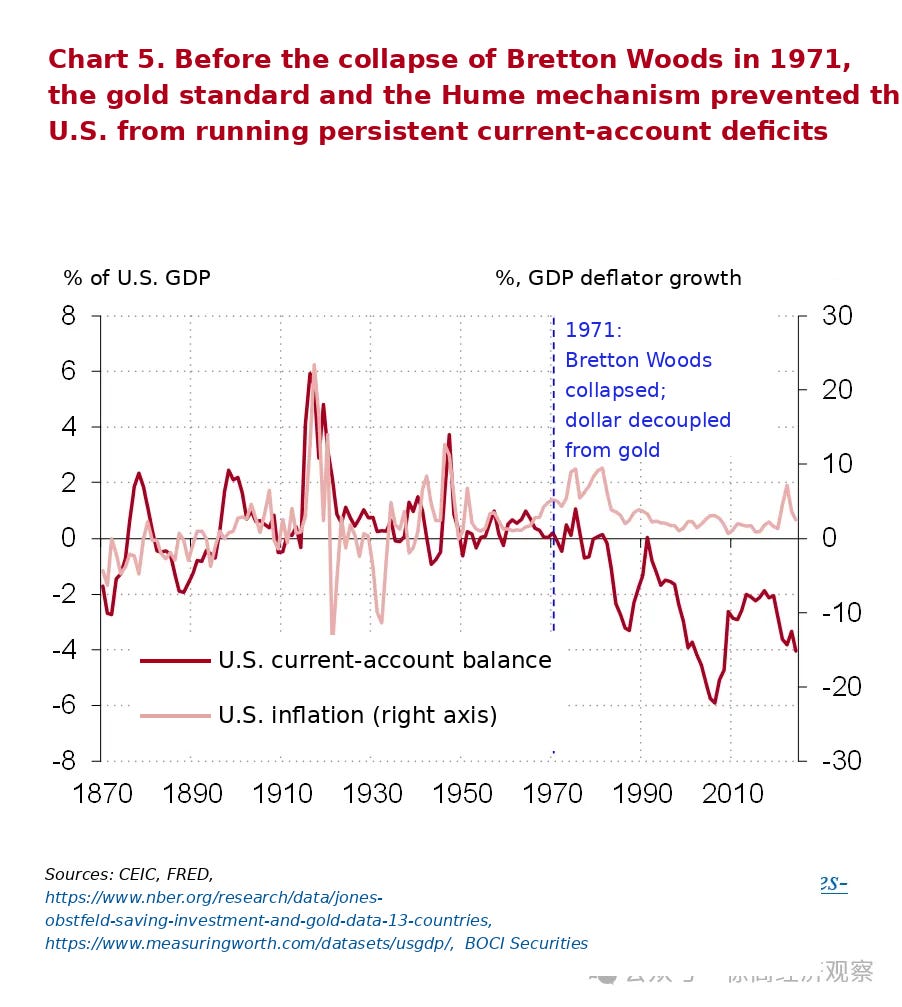

Traces of the Hume mechanism can be seen clearly in historical U.S. data. In the century before the Bretton Woods system collapsed in 1971 and the dollar was decoupled from gold, the U.S. current-account surplus—a broad measure of the trade surplus—was clearly positively correlated with U.S. inflation. This suggests that gold moved across borders in response to surpluses and deficits, thereby affecting domestic price levels. Only after the dollar was decoupled from gold did the correlation between the U.S. current-account surplus and domestic inflation disappear.5 (See Chart 5)

The Hume mechanism, as an automatic mechanism for correcting economic imbalances, should be assessed dialectically. On the positive side, it automatically corrected international trade imbalances. Under the gold standard, countries tended in the long run to maintain both external balance, meaning they did not continuously accumulate trade surpluses or deficits, and internal balance between supply and demand, meaning there was no persistent excess or shortfall in domestic demand. As discussed later, it was precisely the absence of such an automatic adjustment mechanism that allowed the globalisation that emerged in the 1980s to produce persistent global trade imbalances.

On the negative side, however, the internal and external balance achieved through the Hume mechanism depended on structural adjustment in the real economy. Such adjustment was usually slow and painful. This was especially true for trade-deficit countries, which had to correct domestic imbalances through deflation. That often meant macroeconomic recession, or even outright economic crisis.

In sum, the “golden handcuffs” imposed by the gold standard had both advantages and disadvantages. By linking money to gold, countries could avoid excessive money issuance and maintain public confidence in money relatively easily. The cost, however, was the loss of flexibility in monetary policy. Under the gold standard, monetary policy served the objective of maintaining the link between money and gold, rather than stabilising the real economy as it does today. Central banks could adjust interest rates, but such adjustments were aimed primarily at preserving the gold parity. As a result, monetary policy could not act as a buffer for the real economy; the real economy had to absorb shocks through its own adjustment. At times, those shocks even came directly from money that is link to gold. Freeing money from the “golden handcuffs” to turn monetary policy into a stabiliser for the real economy was the main reason money was decoupled from gold. It was also the fundamental force behind the move away from the gold standard and into today’s fiat-money system, the Jamaica system.

3. The Progress From “Anchored” to “Unanchored” Money

The history of the international monetary system over the past two centuries is a history of money’s gradual detachment from physical anchors. The system evolved from bimetallism, in which both gold and silver served as standard money, to the gold standard, then to the gold exchange standard represented by Bretton Woods, and finally to today’s fiat-money system, the Jamaica system.

The collapse of Bretton Woods in 1971 marked the full arrival of the fiat-money era: money was completely decoupled from physical objects and no longer had any physical anchor supporting its value. Before then, some countries had suspended or abandoned such anchors because of war, reparations, or other pressures, as Germany did during the Weimar Republic. But these were temporary exceptions, not the international norm. Only after 1971 did unanchored fiat money become the dominant form of the monetary system. In this sense, the international monetary system over the past two centuries has moved from currencies whose value was backed by physical anchors to money whose value rests on confidence alone.

When considering where the international monetary system may go next, one should not focus only on the shortcomings of the Jamaica system, but also recognise its advantages over earlier systems. The evolution of the international monetary system over the past two centuries was not accidental. The Jamaica system eventually replaced earlier systems because it offered advantages they lacked. Any future international monetary system can replace the existing one only if it preserves the strengths of the Jamaica system while remedying its weaknesses.

The transition from “anchored” to “unanchored” money was a major advance, reflecting humanity’s enhanced capacity to manage the economy. It brought several important forms of progress.

First, human societies learned how to maintain public confidence in money even when money was no longer anchored to a physical object. Everyone knows that fiat money is not a claim on any physical asset, and that no one promises to convert it into one at a fixed rate. Yet people generally still believe that fiat money can preserve its purchasing power over the long term and can be used to purchase goods and services at reasonable prices. This confidence rests on a deeper understanding of how expectations are formed and revised, and on the policy capacity to manage them. By appropriately guiding public expectations, governments can sustain confidence in money.

In this sense, modern monetary policy is the art of managing expectations. What it ultimately regulates is expectations, and its primary objective is to maintain public confidence in money. It is because of this deeper understanding of economic operations that human societies have been able to maintain monetary stability under unanchored money over the past half-century. This itself marks an advance in human capabilities.

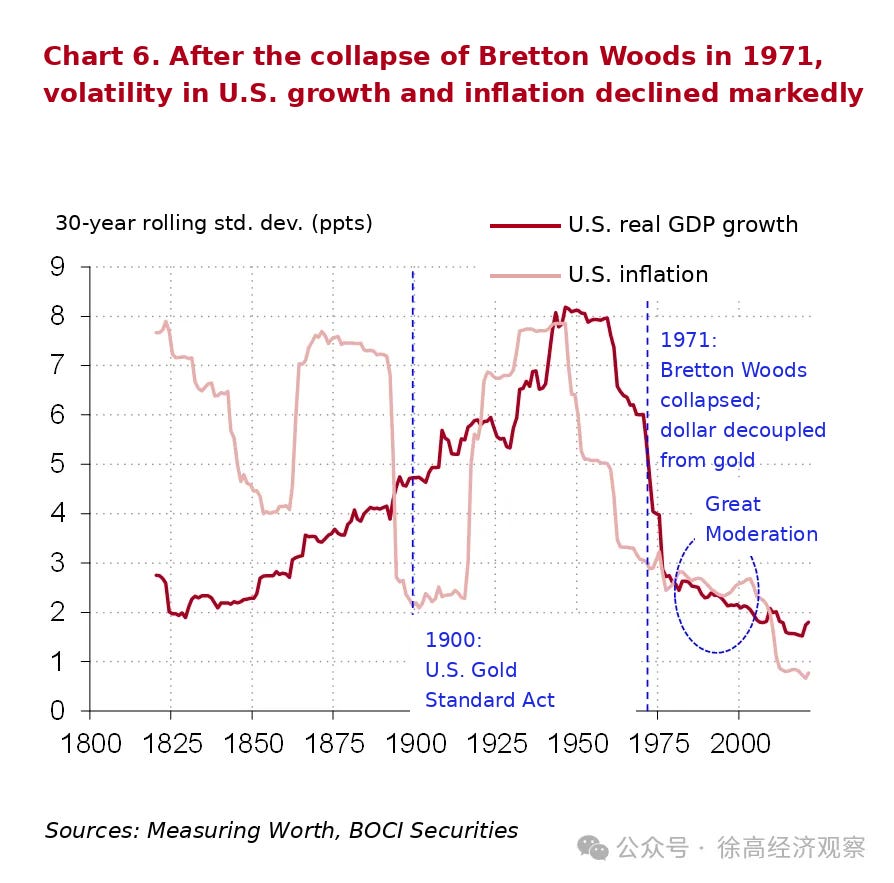

Second, once money was freed from the physical anchor, monetary policy could be adjusted more freely and flexibly, without physical constraints. This turned monetary policy into a buffer for the real economy and thereby reduced economic volatility. When money is no longer linked to gold, monetary policy no longer needs to make the maintenance of that link its primary objective. Instead, it can treat the stable operation of the real economy as an important goal. Today, countries generally take price stability and the promotion of growth, or employment, as the two main objectives of monetary policy. Through flexible adjustment, monetary policy can cushion the real economy against various shocks and reduce volatility. Judging from the 30-year rolling standard deviation of U.S. economic growth and inflation, both real economic volatility and inflation volatility declined significantly after 1971. In the twenty-first century, both have fallen to their lowest levels in nearly two centuries.

Flexible monetary policy, freed from the constraints of the “golden handcuffs”, gave rise to the Great Moderation. From the 1980s to the outbreak of the subprime crisis in 2008, the global economy became significantly more stable. Economists refer to this period as the Great Moderation, often attributing it to the Federal Reserve Chair Alan Greenspan’s “magic” formula. In fact, the deeper force behind it was monetary policy’s release from the “golden handcuffs” and the flexibility this created. That flexibility did not disappear after the subprime crisis. If anything, the introduction of unconventional monetary policy after 2008 further expanded the range of tools available to central banks. This explains why volatility in U.S. economic growth and inflation continued to decline after the crisis. In that sense, the Great Moderation continued even after 2008.

Third, once monetary policy was freed from the constraints of a physical anchor, it became better able to respond to economic crises. This is one way in which monetary policy reduces volatility in the real economy, but it deserves separate discussion. When a crisis breaks out, economic actors in both the financial system and the real economy hoard money to cope with heightened uncertainty. This causes demand for money, or liquidity, to surge. Under the gold standard, the money supply was constrained by a country’s gold holdings, making it difficult for governments to increase liquidity sharply in times of crisis. If that demand for liquidity could not be met, panic was harder to contain, economic activity weakened because of insufficient money supply, prices fell, and the crisis deepened. After the Great Depression began in 1929, the constraints imposed by the gold standard on monetary policy in Western countries were an important reason why the crisis lasted so long and caused such severe damage. Only after Western countries left the gold standard one after another, with Britain abandoning it in 1931, were the conditions created for recovery.

Under a fiat-money system, the money supply can be adjusted flexibly in response to changing conditions, significantly strengthening governments’ ability to manage economic crises. When a crisis erupts, governments can sharply expand the money supply in the short term to meet the market’s demand for liquidity and calm panic. When the subprime crisis broke out in 2008, the U.S. financial system at one point nearly seized up. Yet with the Federal Reserve’s massive liquidity injections, it recovered far faster than the U.S. financial system did after the Great Depression. That the subprime crisis did not produce consequences as severe as the Great Depression owed much to a fiat-money system no longer constrained by a physical anchor.

Fourth, unanchored money has given countries flexible exchange-rate tools, allowing them to use currency movements to absorb external shocks. When currencies were linked to gold, exchange rates were fixed by gold parity, and national monetary policies were effectively tied together by the free cross-border movement of gold. As a result, real economies across countries were forced to adjust in tandem. Changes in one country’s real economy could quickly spill over to others, transmitting shocks abroad.

For example, under the gold standard, a country could fall into a deflationary recession because of technological progress elsewhere. A country experiencing technological progress would become more competitive internationally, expand exports, and run a trade surplus. Gold would then flow into that country, triggering the sequence of effects described earlier under the Hume mechanism. But the technologically advancing country was not the only one forced to adjust. Other countries with stagnant technology would face wider trade deficits, gold outflows, deflation, and declining domestic demand. Their adjustment could be slow and painful, and could even produce economic crises through deflation and liquidity contraction.

In a fiat-money system, countries facing such pressure can respond less painfully by allowing their own currencies to depreciate. When technological progress abroad weakens their competitiveness, they can expand the money supply and let their currencies fall, making their exports more price-competitive in world markets. This helps them preserve international market share and avoid domestic deflation. Currency depreciation, of course, reduces the international purchasing power of the domestic currency and still lowers residents’ welfare. But it allows countries to avoid the slower and more painful real-economy adjustment caused by deflation. As a result, economies facing external technological shocks can experience less volatility and impose smaller costs on their populations.

Fifth, unanchored money supported the “global imbalance” model of globalisation that has prevailed over the past four decades, making an external-demand-driven growth model possible. In international trade, flows of goods are matched by flows of money in the opposite direction: money moves from deficit countries to surplus countries. If money is linked to a physical anchor, such as gold or silver, the global money supply is constrained by the quantity of that anchor. In that case, money in deficit countries would decline, forcing their real economies to adjust and reduce their deficits. This is precisely the effect of the Hume mechanism discussed earlier. When money is anchored to physical objects, no country can sustain a trade deficit indefinitely. Without deficit countries, there can be no surplus countries. Global imbalances, therefore, cannot arise under a physically anchored monetary system. It was monetary de-anchoring that made global imbalances possible, thereby creating external-demand space for economies with insufficient domestic demand. Earlier, global imbalances were described as one of the Jamaica system’s weaknesses. But that weakness also has a beneficial side: it makes external-demand-led growth possible.

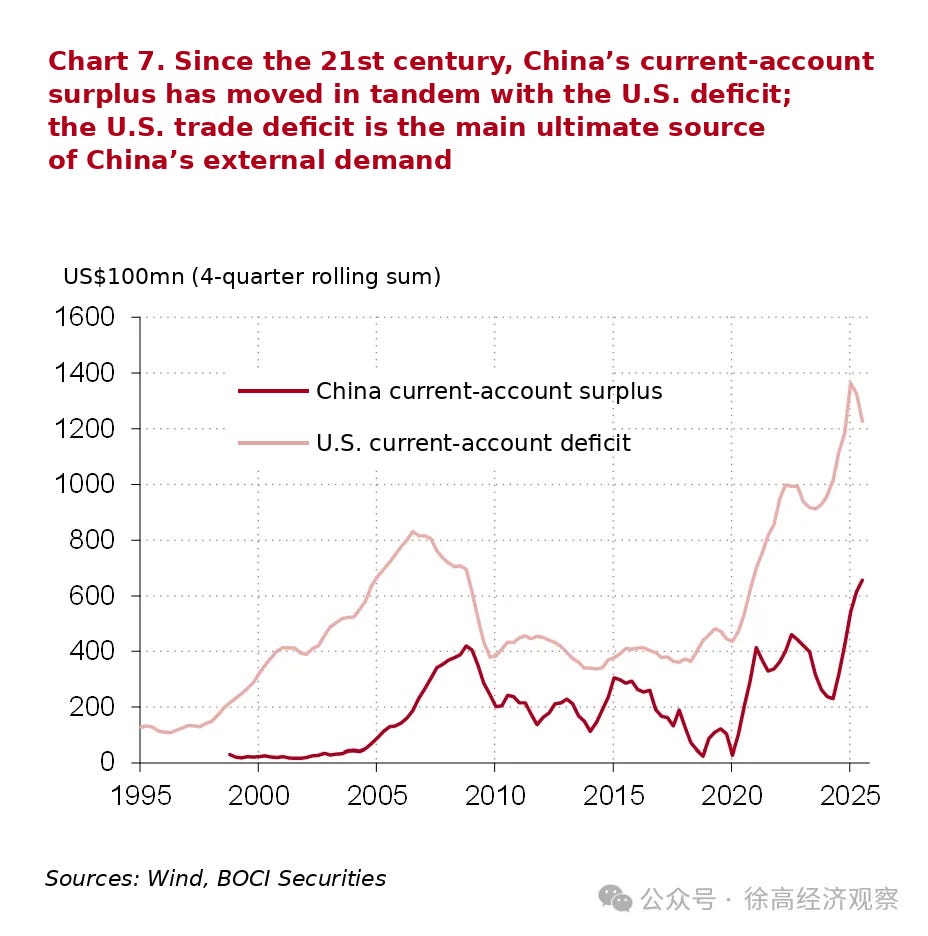

For a country such as China, where domestic demand is insufficient, the absence of global imbalances would be unfavourable. Without the trade deficits created by deficit countries, above all the United States, China could not run a trade surplus. In the long run, external demand, or the trade surplus, would then not contribute to China’s growth. China would be unable to use external circulation to offset weak domestic demand, and growth would come under greater pressure. In the five years after the Asian financial crisis of 1997, and again during the subprime crisis in 2008, China’s growth slowed markedly as external demand weakened. If money had been linked to a physical anchor, these two periods of weak external demand would have become long-term, making it much harder for China to maintain its economic stability. From this perspective, China is undoubtedly a beneficiary of global imbalances and of the Jamaica system that sustains them. Since the beginning of the twenty-first century, China’s current-account surplus has moved closely with the U.S. current-account deficit, and the persistence of the U.S. trade deficit has been the ultimate source of much of China’s external demand.6 China still benefits from the macroeconomic support provided by an external-demand-led growth model. (See Chart 7)

In sum, the move away from physically anchored money gave countries a flexible tool of macroeconomic management: monetary policy. On the positive side, money and exchange rates became buffers for the real economy, improving real economy stability. On the negative side, however, their ability to absorb pressure also weakened the incentive for real-economy adjustment, delayed that adjustment, and allowed structural imbalances to persist. The “global imbalances” of the past forty years can be understood as the result of repeated postponement of supply-demand adjustment in both surplus and deficit countries.

Any international monetary arrangement that seeks to change the status quo must preserve the Jamaica system’s main strength: monetary-policy flexibility. As the Chinese saying goes, “It is easy to move from frugality to luxury, but difficult to move from luxury back to frugality.” The same logic applies to the evolution of the international monetary system. Once people have become accustomed to the stability that flexible monetary policy brings to the real economy, any proposal to remove that flexibility and force the public once again to directly bear painful real-economy adjustments is unlikely to gain acceptance and is therefore bound to fail. Some may argue that structural adjustment in the real economy is necessary for long-term economic health. But flexible monetary policy can at least make such an adjustment faster and smoother, reducing the pain involved. Only arrangements that preserve monetary-policy flexibility while correcting the shortcomings of the Jamaica system can become the future of the international monetary order.

4. Future Scenarios That Can Be Ruled Out

After reviewing the history and current state of the international monetary system, it is now possible to consider its future. The following analysis begins by ruling out implausible scenarios before assessing the most likely path among those that remain.

4.1 A Single-Currency Area Can Be Ruled Out

The first scenario to rule out is the creation of a single-currency area composed of multiple countries, similar to the eurozone. If several countries replaced their sovereign currencies with a common currency, cross-border payments within the bloc would naturally be settled in that currency. If the model were extended globally, that currency would dominate the international monetary system. However, a currency area would strip countries of independent monetary policy, and the exchange rate would effectively be locked at 1:1. Economic differences among members could no longer be absorbed through independent monetary policies or flexible exchange rates, and would eventually pull the currency area apart. The eurozone offers a cautionary example.

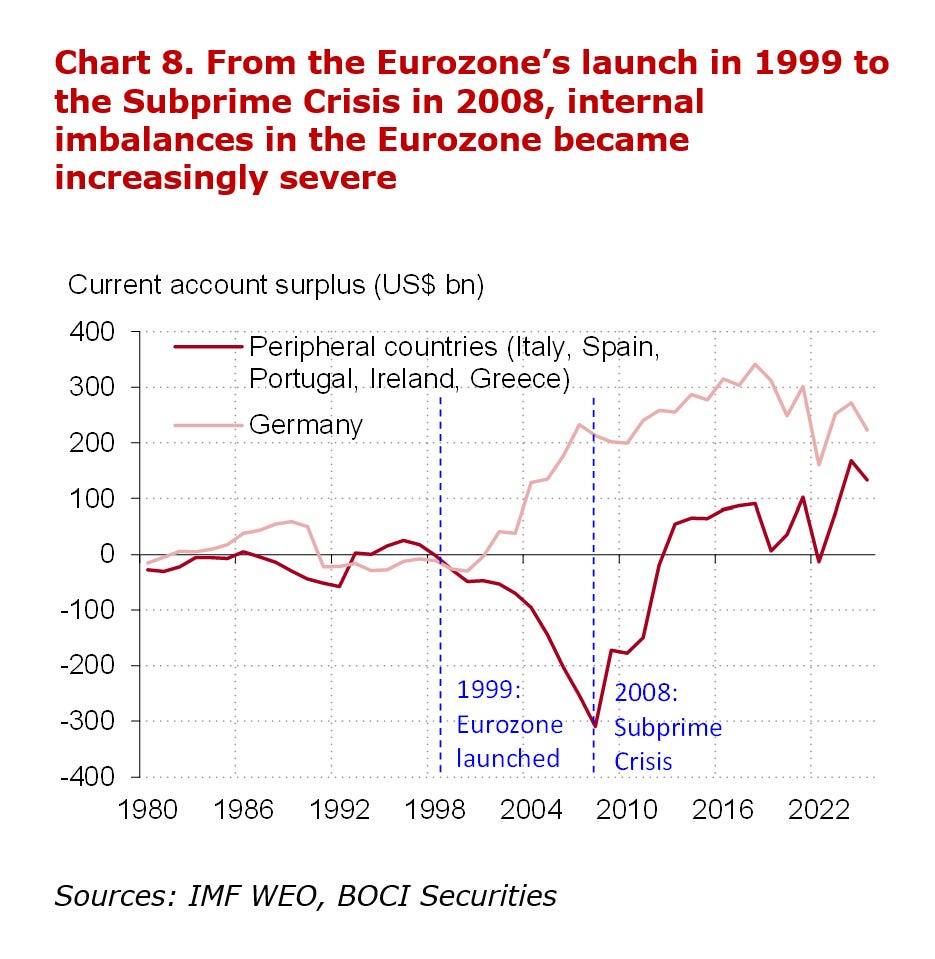

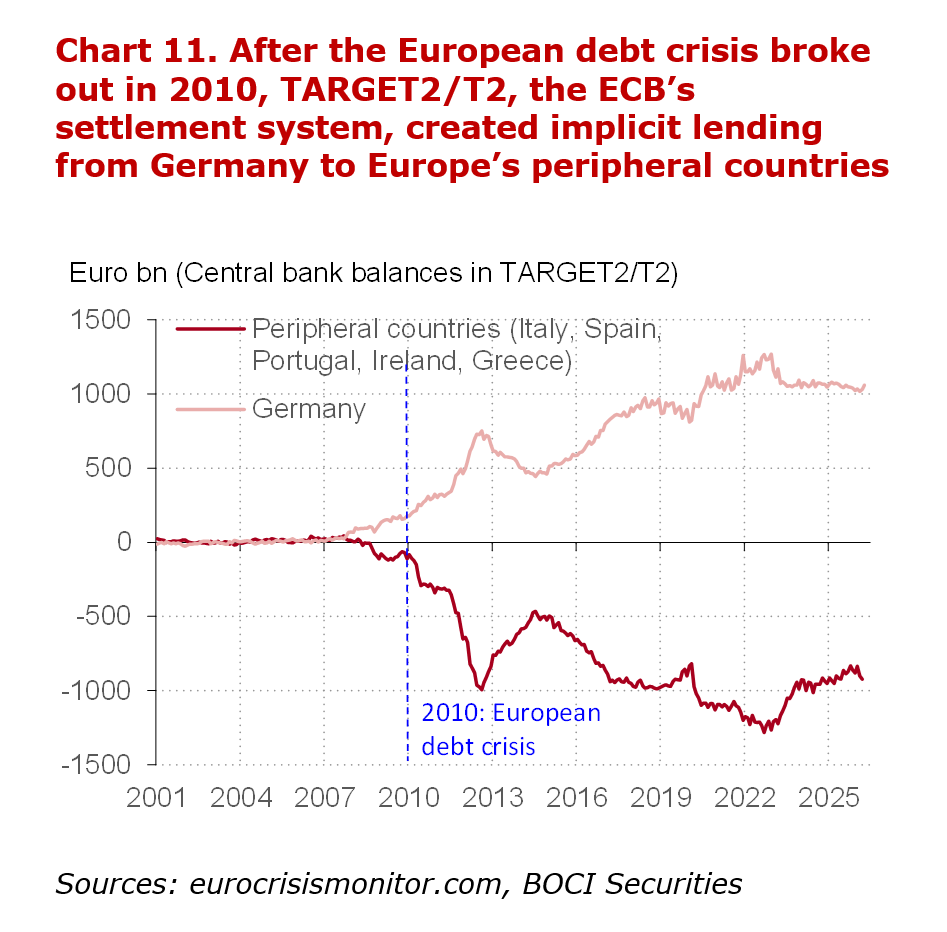

In its first decade after being launched in 1999, the eurozone developed clear internal imbalances. At the time of its creation, most member states had already signed the Schengen Agreement and joined the Schengen Area, removing border checks and allowing people to move freely within the area. The eurozone’s designers hoped that this free movement of people would reduce differences among member states and promote convergence of real economies. That expectation proved too optimistic. Labour mobility alone was far from enough to bridge the gaps among member states. Between the eurozone’s launch in 1999 and the outbreak of the subprime crisis in 2008, internal imbalances emerged and became increasingly severe. Member states split into two distinct groups: 1) current-account-deficit peripheral countries, including Italy, Spain, Portugal, Ireland, and Greece; 2) Germany, with a large current-account surplus. These widening divergences eventually triggered the European debt crisis in 2010, at one point putting the eurozone at serious risk of disintegration.7 (See Chart 8)

As a monetary union without a unified fiscal system, the eurozone still faces a risk of fragmentation. When labour mobility cannot produce economic convergence, fiscal transfers are needed to narrow disparities and hold the eurozone together. The Chinese mainland offers a useful comparison. China’s provincial-level regions together form a currency area using the renminbi. People can move freely across provinces, yet regional disparities remain significant. Yet because these regions belong to a single state, the central government carries out large-scale fiscal transfers each year from more developed areas to less-developed ones. These transfers prevent regional gaps from widening to the point where they could threaten the unity of the currency area.

However, the eurozone is not a unified state; its members have not formed a fiscal union, and cross-country fiscal transfers face enormous political resistance. Without fiscal transfers to narrow national disparities, and without monetary policy—especially exchange-rate policy—to absorb the resulting economic pressures, the eurozone remains vulnerable to fragmentation caused by excessive internal divergence. Although the eurozone has continued to pursue deeper integration, this problem has not been resolved. In this sense, the euro remains structurally fragile.

If even Western European countries, whose differences are relatively limited, have struggled to form a stable single-currency area, creating one on a broader scale would be even less plausible, regardless of what currency were used. The central problem is that when multiple countries share the same currency, they can no longer use monetary policy or exchange rates to absorb differences among national economies. Either their real economies must converge quickly, or cross-border fiscal transfers must be used to narrow the gaps. The former is difficult; the latter is hard to achieve without political union.

The international monetary system is therefore unlikely to move toward a currency-area model in which multiple countries use the same money. This means that sovereign currencies are unlikely to be replaced by a supranational payment instrument. The following analysis, therefore, does not consider the replacement of national currencies (as it is unlikely). Instead, it focuses on what might replace the dollar as the main international payment instrument and reserve asset. It is noteworthy though, that even if the dollar were no longer the dominant currency for international payments, it would remain the primary means of payment within the United States.

4.2 The “Physical Anchor” Will Not Return

The second future scenario to rule out is the emergence of a commodity-backed currency as the main instrument of international payment. In the future international monetary system, international money cannot return to any physical anchor, whether gold or a basket of commodities. Section 3 has already explained why money’s shift from “anchored” to “unanchored” represented progress. Here, the reasons for ruling out a return to a physical anchor can be summarised in two points.

First, linking money to a physical anchor is far from simple. It is not enough for the issuer merely to announce a conversion rate between the currency and the underlying asset. To make the link credible, the issuer must guarantee free convertibility at the stated rate. In other words, the currency must function as a claim on the underlying asset, backed by sufficient reserves and redeemable whenever the market demands. Given the scale of the international economy and the potentially enormous demand for redemption, such a commitment would be difficult for either a single country or a supranational institution to make.

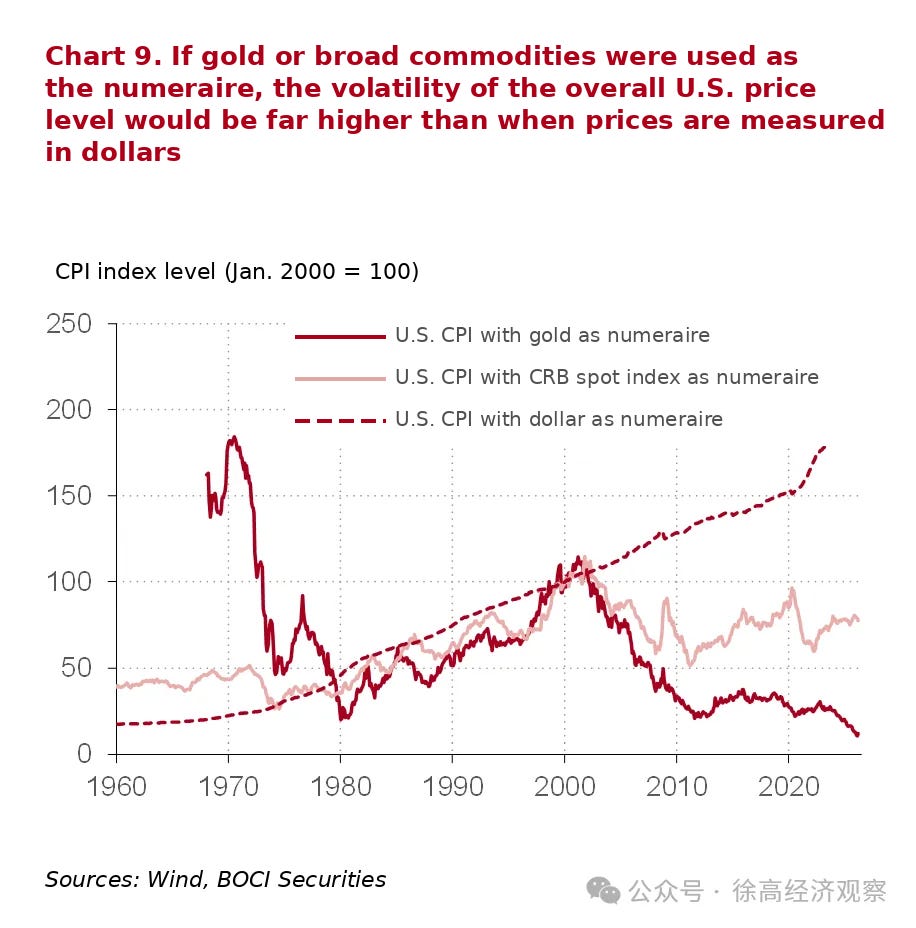

Second, an international currency tied to a physical anchor would lose flexibility. Far from moderating global economic fluctuations, it could itself become a source of shocks. The benefits of flexible monetary policy, and the costs of losing that flexibility, have already been discussed in Section 3. Here, it is enough to consider one consequence of restoring a physical anchor: large fluctuations in the overall price level. Over the past 50 years, both gold and broad commodity baskets have experienced substantial price volatility. By contrast, the basket of consumer goods most directly felt by ordinary people, as measured by the Consumer Price Index, has been relatively stable. This means that the relative price of gold and commodities against consumer goods has fluctuated sharply. If international money were linked to gold or commodities, the prices of national consumer-goods baskets measured in that currency would also fluctuate sharply. To stabilise domestic consumer prices, countries would then have to allow large swings in the exchange rates between their own currencies and the international currency. This would create persistent turbulence in the international monetary system and would therefore be unacceptable to countries.

Many people have misread John Maynard Keynes’s proposal for the bancor and therefore mistakenly believe that a commodity-linked supranational currency could be created. One common claim is that, in designing the post-war international monetary system, John Maynard Keynes proposed a supranational payment currency backed by 30 commodities and called it the bancor. That is not what appeared in his final proposal, the Keynes Plan. Although Keynes may have considered some form of commodity link while developing the plan, he ultimately chose not to include it. For an economist of Keynes’s calibre, it is reasonable to assume that he recognised the two constraints discussed above.

Nor was the bancor linked to gold. In the Keynes Plan, it had many of the features of an unanchored fiat currency. Countries could obtain bancor by paying in gold, but they could not redeem bancor for gold. Its issuance was therefore not constrained by the issuer’s gold reserves.

Since the international monetary system cannot return to a physical anchor, two possibilities are naturally ruled out.

First, the gold standard, or any variant of it, can not return. More than a century ago, Keynes had already recognised that the gold standard was out of step with the needs of the age, denouncing it as “a barbarous relic.” In A Tract on Monetary Reform, published in 1924, Keynes wrote: “In truth, the gold standard is already a barbarous relic…Advocates of the ancient standard do not observe how remote it now is from the spirit and the requirements of the age.” A gold standard that was already outdated more than a century ago has no real prospect of returning today.

Second, proposals for a supranational currency linked to commodities or other physical anchors will not succeed. Many people imagine a future international monetary system in which a supranational institution issues a supranational currency as an instrument of international payment. The first challenge for such a currency is establishing international trust in it. Linking it to a physical anchor may seem like an easy way to build that trust. But, as discussed above, making a supranational currency genuinely convertible into a physical asset is itself extremely difficult. The issuing institution would need enormous reserves, just as countries under the gold standard needed gold reserves. Even if that could be achieved, a supranational currency constrained by physical reserves and lacking flexibility would still be unable to meet the international community’s needs for payments and reserves. Therefore, even if a new supranational currency emerges in the future international monetary system, it cannot be linked to a physical anchor.8

4.3 Sovereignless Cryptocurrencies Cannot Become the Main International Means of Payment

In 2008, Satoshi Nakamoto published “Bitcoin: A Peer-to-Peer Electronic Cash System,” opening a period of rapid development in digital currencies. Nakamoto invented blockchain technology and used it to design a system that could conduct peer-to-peer electronic payments without verification by a trusted third party. This made it possible for payment systems to operate in a decentralised way, without a central node. Based on this idea, Bitcoin, an unprecedented digital cryptocurrency, was created. Bitcoin’s total market capitalisation now exceeds US$1 trillion. Since then, many other cryptocurrencies based on similar technologies have been developed. The rise of cryptocurrencies has also pushed central banks around the world to accelerate their own digital transformation, prompting several countries to launch central bank digital currencies (CBDCs). The People’s Bank of China launched the digital renminbi, or e-CNY, in 2022.

Digital currencies today fall mainly into three categories: sovereignless cryptocurrencies, stablecoins, and CBDCs. The first category, sovereignless cryptocurrencies, refers to digital currencies that do not rely on the credit backing of any sovereign state, are not linked to any national fiat currency or physical anchor, and are issued and circulated solely through decentralised networks and consensus algorithms. Bitcoin is the leading example and accounts for the largest share of this category. The second category, stablecoins, also uses technologies similar to those behind sovereignless cryptocurrencies. However, to address large price fluctuations, stablecoin issuers peg them to sovereign currencies.9 For every unit of stablecoin issued, the issuer holds an equivalent amount of national currency as reserves. Stablecoins can therefore be seen as an extension of sovereign currencies. The third category, CBDCs, differs from cryptocurrencies. They are digital currencies issued and managed by central banks, operating on centralised payment networks built around the central bank. CBDCs are the digital form of sovereign legal tender.

For three reasons, sovereignless cryptocurrencies cannot become the main instruments of international payment.

First, they are likely to face sustained resistance from sovereign states, which leaves them limited room for development. Currency issuance is a core sovereign power, and seigniorage is an important source of revenue for states. Governments are therefore unlikely to tolerate other organisations sharing in the power to issue money. In addition, sovereignless cryptocurrencies offer a considerable degree of anonymity, making them attractive tools for criminal activities such as money laundering. To protect monetary sovereignty and combat crime, sovereign states have strong incentives to ban or restrict their use.

China has already halted domestic cryptocurrency activities. In September 2021, the People’s Bank of China and nine other ministries and commissions jointly issued the Notice on Further Preventing and Disposing of Risks Related to Virtual Currency Trading and Speculation, which classified business activities related to sovereignless cryptocurrencies, referred to in the notice as virtual currencies, as illegal financial activities in China and strictly prohibited them. On February 6, 2026, the People’s Bank of China and seven other ministries and commissions again issued the Notice on Further Preventing and Disposing of Risks Related to Virtual Currencies and Related Activities, further clarifying that virtual currencies do not have the same legal status as sovereign legal tender, are not legally redeemable as currency, and should not, and cannot, circulate or be used as money in the market.

Second, sovereignless cryptocurrencies suffer from both rigidity and excessive flexibility. Any such currency that seeks to gain public trust must place limits on its own issuance. Bitcoin, for example, has a maximum supply of 21 million coins, fixed by algorithms. If a sovereignless cryptocurrency were truly used as an international means of payment, this quantitative rigidity would cause sharp swings in international commodity prices and disrupt international trade. In this respect, its weaknesses resemble those of money tied to a physical anchor.

At the same time, however, anyone with the relevant technical capacity can create a new sovereignless cryptocurrency. Since Bitcoin, other cryptocurrencies such as Ethereum and Binance Coin have emerged. These new entrants continuously divert liquidity and attention away from existing cryptocurrencies and expose them to repeated shocks. This weakens public confidence in any single sovereignless cryptocurrency.

Third, the decentralised technological model on which sovereignless cryptocurrencies rely faces serious technical constraints. Blockchain technology is subject to an “impossible trinity”: decentralisation, security, and scalability are difficult to achieve at the same time. In practice, a system can usually prioritise only two of the three, while sacrificing the third to some degree. Put simply, if decentralisation is required, transaction capacity, or scalability, is likely to be limited. Bitcoin, for example, currently processes fewer than 10 transactions per second worldwide. Visa, by contrast, processes more than 1,000 transactions per second. Bitcoin’s extremely low throughput clearly cannot support large-scale transaction demand.

Improving cryptocurrency performance would require the introduction of a central node, but that would undermine the very advantage of decentralisation. Technologies such as directed acyclic graphs are being explored as possible ways to address this impossible trinity, but progress remains limited. More importantly, it remains uncertain whether these alternative technological paths can win the same broad public trust that blockchain has acquired, and thereby support cryptocurrencies used at scale.

The analysis above rules out the possibility that sovereignless cryptocurrencies could become the main instruments of international payment. But this conclusion applies only to one form of digital currency. Stablecoins and CBDCs are digital extensions of sovereign currencies and should be understood as digital forms of sovereign money. Although they may use some cryptocurrency-related technologies, they are fundamentally different from sovereignless cryptocurrencies. The preceding analysis, therefore, does not apply to them.

5. Possible Futures for the International Monetary System

With the impossible scenarios ruled out, the analysis can now turn to the more plausible future paths of the international monetary system. Before doing so, three points need to be clarified.

First, the international monetary system changes slowly and over long periods. Although the current dollar-centred system has many problems, it is likely to persist for decades. The future discussed here is therefore not a future one or two years away, but the world around the middle of this century. Even so, long-term trends are already shaping present choices, so it is still worth looking that far ahead.

Second, the central question in assessing the future of the international monetary system is what could replace the dollar as the main international payment instrument and reserve asset. This is different from asking what could replace the sovereign currencies currently used by individual countries. The eurozone has already shown that, without political union, replacing multiple national currencies with a single currency is unlikely to produce good results. Sovereign currencies will therefore continue to exist for a long time. They will not disappear because the instruments used for international payments change.

Third, the claim that artificial intelligence will eliminate money is too utopian to serve as a serious basis for assessing the future of the international monetary system. AI is the most important technological innovation of the present era and is likely to raise human productivity substantially. But however much output expands, it will remain limited relative to unbounded human wants. AI-generated output still depends on resources and energy. AI can improve the efficiency with which humans use those resources, but it cannot abolish scarcity. As long as output remains scarce, markets will continue to function as mechanisms for allocating resources, and money will remain necessary as the means of payment in market transactions. AI will not eliminate money, although it may change the form money takes. That possibility should be taken into account when considering the future of the international monetary system.

With these points clarified, the next question is what might replace the dollar as the main payment instrument in the international monetary system.

5.1 Other Sovereign Currencies: Possible but Unlikely

It is not impossible that another sovereign currency could one day replace the dollar as the central currency of the international monetary system. But the probability is low. Some may argue that, since the dollar became the dominant international payment instrument on the back of American power, the currency of another country or bloc could replace it if that country or bloc were to surpass the United States in overall strength.10 This view underestimates the difficulty of challenging the dollar. As the anchor of the current system, the dollar enjoys a powerful incumbent advantage created by network externalities, setting a very high bar for any challenger.

Network externality means that the value users derive from a network rises with the number of other users connected to it: the more users there are, the more useful the network becomes for each participant. For more than half a century, the world has built a highly developed international payment system around the dollar. For example, if someone wanted to exchange Honduras’s currency, the lempira (HNL), directly into Nepal’s currency, the Nepalese rupee (NPR), it would probably be difficult to find a counterparty who happened to want to exchange Nepalese rupees for lempiras. But it would be far easier to exchange lempiras into dollars, and then dollars into Nepalese rupees. With the dollar as an intermediary, currencies around the world can be exchanged relatively easily. Because so many countries use the dollar in international trade and finance, it is convenient for everyone to keep using it.

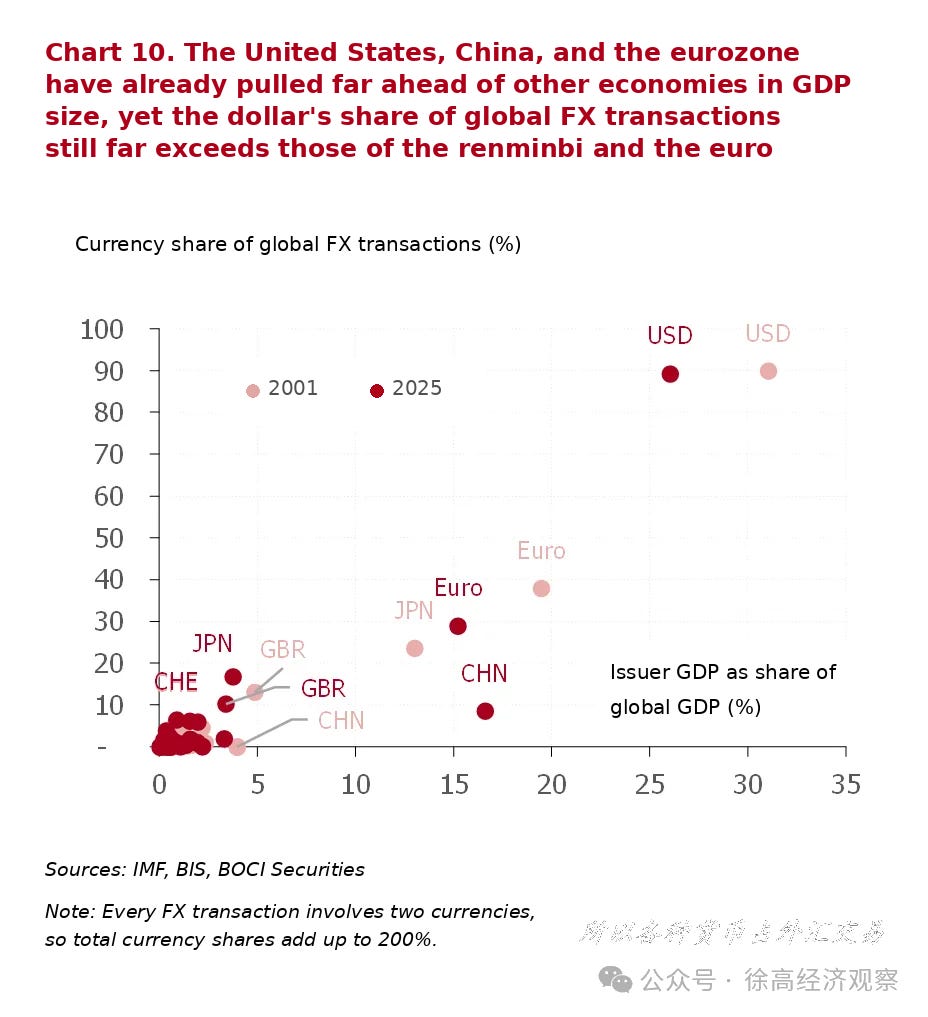

Because of these network externalities, another sovereign currency could replace the dollar only if its issuing country, or currency bloc, established an overwhelming advantage over the United States. That advantage would have to appear across many dimensions, including economic size, trade volume, the breadth, depth, and openness of financial markets, the stability of economic and financial conditions, and military power. Globally, the only currencies that might conceivably acquire such advantages in the future are the euro and the renminbi. Yet the eurozone, as a monetary union without a unified fiscal system, remains structurally fragile and is therefore poorly placed to challenge the dollar. China, meanwhile, still lags far behind the United States in financial markets and several other areas. According to statistics from the Bank for International Settlements (BIS), transactions involving the dollar accounted for as much as 89 per cent of all global foreign-exchange transactions in 2025, only one percentage point lower than in 2001. The shares of the euro and the renminbi remained far below that of the dollar. Replacing the dollar with another sovereign currency would therefore be extremely difficult. (See Chart 10)

5.2 A Supranational Currency Backed by Multiple Sovereign Currencies

The most plausible post-Jamaica path is a supranational currency linked to a basket of sovereign currencies, gradually replacing the dollar’s central role. Once the possibilities of a single-currency area, a physical anchor for money, and sovereignless cryptocurrencies are ruled out, and given the great difficulty of replacing the dollar with another sovereign currency, the most likely direction of change is a supranational currency supported by multiple sovereign currencies. There are two reasons.

First, the main international payment instrument after the dollar is unlikely to be another sovereign currency, cannot be a sovereignless currency, and certainly cannot be a natural physical object. It would therefore have to be a supranational currency issued by a supranational institution. This follows from the analysis above. Such an institution could not replace sovereign states; it could only be an international body jointly established by several sovereign states. A supranational currency constructed by multiple countries would also be better placed to overcome the incumbent advantage that network externalities confer on the dollar.

Second, at least in its early stages, such a supranational currency would need to be linked to multiple sovereign currencies to establish international trust. The central question for any new currency is how it can win confidence. Since money cannot be reattached to a physical anchor, trust cannot be built through commodity backing. Nor could the international institution issuing such a currency possess the coercive power of a sovereign state, so it could not rely on force to establish confidence. Its credibility would therefore have to rest on a link to sovereign currencies. Linking it to a single sovereign currency would serve little purpose: users might as well use that currency directly. It would therefore need to be linked to multiple sovereign currencies. In effect, such a supranational currency would have to function as a claim on a basket of sovereign currencies, giving users confidence that it could be exchanged at any time for that basket.

The Special Drawing Right (SDR), created by the International Monetary Fund (IMF) in 1969, is the embryonic form of such a supranational currency. The SDR itself is not a currency, but a book asset whose value is linked to a basket of sovereign currencies. At present, that basket includes five currencies: the dollar, the euro, the renminbi, the yen, and sterling. For the 2022–2027 period, their weights are 43.38 per cent, 29.31 per cent, 12.28 per cent, 7.59 per cent, and 7.44 per cent, respectively. Under the IMF’s Articles of Agreement, SDRs may be held only by IMF member countries and the IMF itself; individuals and private entities cannot hold them. This has limited their use. As of April 2026, total SDRs stood at SDR 660.8 billion, equivalent to about US$900 billion, leaving them relatively small in scale. If the scope of SDR use were broadened, issuance expanded, and private entities allowed to hold and use them for international payments, the SDR could evolve into a supranational currency and potentially become a major international payment instrument.

However, because the United States has veto power in the IMF, the SDR cannot challenge the dollar’s position in the international monetary system. Article XV, Section 2 of the IMF Articles of Agreement stipulates that an eighty-five per cent majority of the total voting power shall be required for a change in the principle of valuation or a fundamental change of the principle in effect. At present, the United States holds 16.49 per cent of the IMF’s voting power. This means that without U.S. consent, the IMF cannot change the rules governing the SDR. Given the United States’ incentive to preserve dollar dominance, it clearly cannot allow the SDR to become an international currency capable of challenging the dollar.

The R5, linked to the currencies of the BRICS countries, is a conception of a supranational international currency similar to the SDR, but one that could bypass U.S. constraints. Aleksei Mozhin, Russia’s Executive Director at the IMF, and Paulo Nogueira Batista Jr., former Brazilian Executive Director at the IMF, have both proposed that the BRICS countries could jointly issue a supranational currency. This currency would be linked to the sovereign currencies of the five BRICS countries: Brazil, Russia, India, China, and South Africa. Coincidentally, the English names of all five currencies begin with the letter R: Brazil’s real, Russia’s ruble, India’s rupee, China’s renminbi, and South Africa’s rand. A supranational currency linked to them could therefore be called the “R5”. The R5 would inherit the advantages of the SDR, while being less vulnerable to an outright U.S. veto, and could therefore become one possible future instrument of international payment.

5.3 The Main Problems a Supranational Currency Must Solve

For a supranational currency backed by a basket of sovereign currencies to challenge, or even replace, the dollar in the international monetary system, three major problems would have to be addressed.

First, how should the seigniorage from currency issuance be distributed? One solution would be to allocate seigniorage in proportion to the economic size of the countries participating in the currency’s issuance. Specifically, newly created supranational currency could be distributed according to the size of participating economies: larger countries would receive more, smaller countries less. This would distribute seigniorage among participating countries in a relatively fair way and avoid the inequity of the United States using the dollar to extract gains from the rest of the world.

Second, how should differences among the real economies of participating countries, and the trade imbalances arising from them, be handled? The answer is that trade imbalances are difficult to eliminate and would have to be tolerated. The experience of globalisation over the past half-century has shown that achieving long-term trade balance among all countries is unrealistic, both today and in the foreseeable future. Under the gold standard, long-term trade balance was achieved through the Hume mechanism, but only by forcing painful adjustment in countries’ real economies. As long as such adjustment can be avoided, people in different countries will be unwilling to bear its costs. This is especially true of surplus countries. When designing the post-Second World War international monetary system, Keynes once proposed taxing surplus countries to force them to reduce their surpluses. In modern society, such an idea would be unacceptable to surplus coungtries. The more realistic option, therefore, is to use a supranational currency to absorb the adjustment pressure created by trade imbalances, allowing global imbalances to persist, and surplus countries would continue to accumulate supranational currency.

Third, how should the supranational currency accumulated by the international community be invested? Trade-deficit countries would need to issue substantial amounts of government debt denominated in the supranational currency, creating a deep international market for such bonds to meet investor demand. Trade imbalances correspond to flows of savings from surplus countries to deficit countries. Once surplus countries accumulate supranational currency, they need to invest it abroad to earn returns. Deficit countries, meanwhile, not only receive supranational currency allocated by the issuing institution, but also need to borrow additional amounts from abroad to pay for imports.

The most workable solution would be for deficit-country governments to issue large quantities of government bonds denominated in the supranational currency, thereby meeting the investment demand of surplus countries. Deficit-country governments would not be the only possible issuers. Surplus-country governments and private-sector entities in various countries could also issue bonds in the supranational currency, increasing the supply of investable assets. But given the direction of savings flows under global imbalances, deficit countries, as importers of savings, should be the main providers of such assets. Compared with private-sector bonds, government bonds are clearly safer and should therefore form the core of the asset pool, at least in the early stage.

If these three issues can be resolved along these lines, a supranational currency could develop relatively smoothly.

5.4 The Path From the Present to the Future

Although it remains unclear what form a supranational currency capable of challenging the dollar might eventually take, current U.S. policy is already pushing the international monetary system in that direction.

First, the anti-globalisation policies adopted by the United States since 2025 have shaken international confidence in the dollar. After Trump began his second term as U.S. president in 2025, the United States introduced measures such as “reciprocal tariffs”. In the article “A Deep Understanding of the Logic and Impact of the U.S. Tariff War”, published on May 12, 2025, I argued that over the past 40 years of global imbalances, the global dollar cycle had channelled foreign savings back to the United States and supported the accumulation of U.S. debt. If the United States seeks to shrink its trade deficit through anti-globalisation policies, the high-consumption, high-debt growth model on which it has relied for the past four decades will become unsustainable. Unless the U.S. economy transforms in time by reducing domestic consumption and raising domestic savings, anti-globalisation policies will expose the United States to debt risks, causing dollar assets—once the world’s safe haven—to lose the trust of global capital. The dollar’s weakness since April 2025, together with the strength of gold over the same period, is consistent with this logic.

Second, the U.S. tendency to use the dollar as a sanctions tool—to weaponise the dollar—has also given the international community stronger incentives to reduce its reliance on the currency. Because the dollar occupies a central position in the international payment system, many global cross-border dollar transactions must be cleared through the U.S. banking system. This gives the United States enormous influence over international payment infrastructure, such as SWIFT. After the outbreak of the Russia-Ukraine war in 2022, the United States imposed unprecedented sanctions on Russia, excluded Russian institutions from SWIFT, and froze Russia’s foreign-exchange reserves. If the United States can use the dollar to sanction Russia, it can naturally do the same to other countries. This gives other countries an incentive to seek alternatives. The Russian and Brazilian scholars mentioned earlier, who advocated the R5, also treat the weaponisation of the dollar as one reason for creating such a supranational currency.

Many countries have already begun building international payment systems outside the dollar. After being cut off from SWIFT, Russia developed the Financial Messaging System of the Bank of Russia (SPFS) as an alternative channel for payments. China has built the Cross-border Interbank Payment System (CIPS) to support international payments based on the renminbi. In 2021, the People’s Bank of China, together with the BIS Innovation Hub Hong Kong Centre, the Bank of Thailand, the Central Bank of the UAE, and the Hong Kong Monetary Authority, launched the Project mBridge, which uses blockchain technology to connect multiple central banks and facilitate more convenient and efficient cross-border payments.

As payment systems built by different countries continue to develop, they will gradually give rise to a supranational currency supported by multiple sovereign currencies. First, because of network externalities, the larger a payment network becomes, the more efficient and convenient it is. International payment networks built by different countries, therefore, have a tendency to connect with one another and eventually form a larger network. Second, as the number of currencies in such a network increases, a central currency may naturally emerge to facilitate exchange among them, with different currencies converted through this central unit. Given the precedent of the dollar’s “exorbitant privilege” and the backlash it has generated, this new central currency is more likely to be supranational than an existing sovereign currency. As discussed earlier, such a supranational currency should be decoupled from physical anchors and linked instead to multiple sovereign currencies.

As this supranational currency and its corresponding international payment network develop, the dollar may eventually be absorbed into the new system. The United States faces a fundamental Triffin dilemma: U.S. hegemony gave rise to dollar hegemony, but dollar hegemony in turn erodes U.S. hegemony. This means that the dollar-centred international monetary system will eventually move toward its own negation. In that process, a supranational currency supported by multiple countries could ultimately replace the dollar at the centre of the international monetary system. At that point, the United States would have little choice but to support the new supranational currency and allow the dollar to become part of the basket of currencies to which it is linked.

Compared with this path, a better long-term option for the United States would be to promote SDR reform and allow the SDR to gradually become the supranational currency that replaces the dollar. Although this would better serve U.S. interests in the long run, it would also require the United States to weaken the dollar’s position by choice, and would probably be difficult for any U.S. government to accept.

The most likely path from the present to the future of the international monetary system is this: as international trust in the dollar weakens, a supranational currency jointly supported by multiple countries will come into wider use and eventually replace the dollar as the central currency of the international monetary system. Ultimately, the United States may be forced to accept the inclusion of the dollar in the basket of currencies to which that supranational currency is linked, completing the transformation of the international monetary system. If the BRICS countries can reach an agreement on establishing an R5 currency, it would have significant potential to become such a future supranational currency.

In discussing this path, however, the resilience of the Jamaica system should not be underestimated. As noted at the beginning of this section, the international monetary system evolves slowly, over decades rather than years. Before any future supranational currency emerges, the dollar-centred Jamaica system is likely to remain in place for a long time. The United States has indeed extracted seigniorage from the world through the dollar. In this sense, the dollar relies on the global economy as the base from which that seigniorage is drawn. But the global economy also relies on the dollar as a payment instrument, a reserve asset, and a pressure absorber that helps sustain global imbalances.

Many people see only the support that the “petrodollar” provides to the dollar, namely, the use of dollars by oil-exporting countries to settle oil trade. They overlook the fact that oil-exporting countries also need the dollar to absorb the pressure created by structural imbalances arising from insufficient domestic demand. For a fairly long period before the emergence of the supranational currency described above, the world economy will continue to need the dollar. That need gives the Jamaica system its resilience.

In the current international economy, the greater danger is not that the world will abandon the dollar, but that the world will lose a credible dollar. As argued above, the international community currently has no good alternative to the dollar as an international payment instrument. The world is therefore unlikely to abandon the dollar by choice. At the same time, however, U.S. anti-globalisation policies and unilateralist tendencies are eroding the credibility the dollar has built up over many decades. If the dollar loses that credibility, and if the international community no longer trusts the safety of dollar assets, international trade could suffer severe damage from the absence of a reliable international payment instrument; international financial markets could experience major turbulence as capital withdraws from dollar assets; and global imbalances could contract sharply as the dollar ceases to provide a buffer. A global shortage of payment instruments and safe assets caused by the loss of dollar credibility could trigger a severe global economic crisis. Such a crisis could, in turn, create the conditions for the emergence of a supranational currency to replace the dollar.

6. China’s Choices

Based on the preceding analysis, the following choices would best serve China’s long-term development during the transformation of the international monetary system.