Miao Yanliang: from Spanish silver to SWIFT, the forces that make currencies rule

CICC chief strategist & former SAFE chief economist argues economic scale, financial depth, institutions, technology, and network effects—with war as catalyst, not cause—shape currency leadership.

We have shared, at length, Miao Yanliang’s insight into U.S. dollar hegemony and whether the renminbi, the Chinese currency, will affect it. In the following essay, Miao looked back at history, examining the change and continuity of the international monetary order.

Miao served for 10 years at the China State Administration of Foreign Exchange (SAFE), part of the People’s Bank of China, including as its Chief Economist since May 2018. He joined SAFE in 2013 as Senior Advisor to the Administrator and then Head of Research.

His current job is Chief Strategist and Executive Head of the Research Department at China International Capital Corporation Limited (CICC), a leading Chinese investment bank.

Before SAFE, he was an economist with the IMF for five years. He holds a PhD, an M.A., and an M.P.A. from Princeton University.

The following is based on a manuscript Miao shared with us, similar to a WeChat blogpost by CICC on November 28, 2025.

缪延亮:国际货币秩序的“变”与“不变”——从“中心-外围”结构看国际货币体系的推动力

Miao Yanliang: The “Change” and “Continuity” of the International Monetary Order—Examining the Driving Forces of the System through a “Core–Periphery” Structure

In reviewing the historical evolution of the international monetary system, I have identified three stylised facts.

First, money displays an inherent order and, for most historical periods, a “core–periphery” structure. Under the Bretton Woods system, the U.S. dollar occupied the core position; under the classical gold standard, the British pound sterling did; and earlier still, the Dutch guilder played a comparable role. When Bretton Woods collapsed in 1973, the dollar was widely expected to lose its core status, yet it quickly stabilised and retained its core position.

Second, such monetary orders tend to be relatively durable. Sterling’s predominance emerged in the nineteenth century and remained substantial through the period around the First World War. The dollar’s rise to leading international-currency status occurred in the interwar years and has sustained it for nearly a century to date.

Third, such orders are not immutable. Central-currency status has shifted over time. Over roughly the past five centuries, the system has moved from the Spanish silver dollar to the Dutch guilder, then to sterling, and ultimately to the U.S. dollar.

These observations raise a further question: what forces drive the rise and replacement of a core currency, and through what mechanisms might the renminbi move toward core-currency status? A review of historical experience suggests four—or, more precisely, four and a half—main drivers.

The first is the economic foundation. When an economy can supply large volumes of high-value-added goods and services, global trade with that economy generates endogenous demand for its currency.

Second is the financial market. Money ultimately rests on trust. Domestically, monetary credibility is underpinned primarily by state sovereignty and coercive authority; internationally, however, it must be earned through market-based competition. Economic size does not automatically translate into trust. Only financial markets with sufficient depth, breadth, and liquidity can enable a currency to function effectively as a unit of account, a means of settlement, and a store of value, thereby winning broad-based confidence in the international community.

The third is institutional factors. The credibility of institutions, including the protection of property rights and the conduct of macroeconomic policy, provides the foundation for a currency to build long-term trust.

The fourth is technological forces. Historically, each major transformation in money—from shells and precious metals to paper currency—has been the result of institutions and technology working jointly. Technology has changed not only the form of money but also the architecture of payment and settlement systems.

There is also a view that military power constitutes a fifth driving force. My judgment is that military power can, to some extent, protect existing credibility, but it cannot create credibility ex nihilo. It is therefore better regarded as “half a force”.

Taken together, rising economic power does not automatically translate into rising monetary power. For a currency to move from the periphery of the system to its core, it must not only seize historical windows created by the relative decline of an incumbent core currency; more importantly, it must enhance its own credibility through sustained market-building and institutional reform. This perspective is also instructive for understanding the renminbi’s path to internationalisation.

Chapter 1 The Historical Evolution of the International Monetary System

This section reviews the trajectory from early silver hegemony to the Jamaica system, and identifies the driving forces behind each episode of order formation and disintegration. The aim is to provide an analytical basis for understanding the internal logic of the “core–periphery” structure in the international monetary order.

I. The Proto-Form of the International Monetary System

In the sixteenth century, Spain rapidly established a vast colonial empire through overseas expansion during the Age of Discovery. Yet what fundamentally altered the empire’s trajectory was the 1545 discovery of the silver deposits at Potosí, often described as a “treasury of the world.” Silver was extracted at scale through coercive labour systems imposed on Indigenous populations. Output increased markedly after mercury-amalgamation techniques were introduced for refining, and silver became the principal economic pillar supporting Spain’s imperial expansion and prosperity.

By some estimates, in the sixteenth century, the Americas accounted for approximately 85 per cent of global silver production, most of which flowed into Europe through trade routes controlled by Spain. In this context, Spanish silver coinage, especially the eight-real coin (real de a ocho), emerged as a dominant trade coin, aided by relatively stable fineness and standardised specifications.

However, the prosperity brought by silver did not translate into broad-based gains in productive capacity. Instead, it displayed features that later literature would describe as a “resource curse.” The surge of precious-metal inflows contributed to severe inflation in Spain; prices in sixteenth-century Spain rose by roughly 400 per cent, far exceeding the rate observed elsewhere in Europe. The relative abundance of bullion also weakened incentives to develop domestic industry and agriculture, contributing to longer-run structural weaknesses. Although Spain possessed some of Europe’s finest wool resources, it failed to cultivate a competitive textile industry, exporting raw wool to the Low Countries and importing finished cloth at higher prices.

Ironically, despite continued bullion inflows, the Spanish Crown repeatedly faced acute fiscal strain. A substantial portion of revenues was absorbed by military expenditure and debt servicing rather than productive investment. In 1557, 1575, and 1596, the Crown suspended debt payments—episodes commonly described as sovereign “bankruptcies”—which severely damaged its creditworthiness and contributed to the gradual unravelling of the order that had been sustained by silver-based hegemony.

By the seventeenth century, the Dutch bank florin rose to prominence as a leading unit of account. Benefiting from dynamic trade networks and a vibrant commercial culture, the Dutch Republic entered its “Golden Age” (1588–1672). In 1609, the Bank of Amsterdam (the Wisselbank) was established and innovatively created bank money.

This institutional innovation had multiple advantages. First, the Bank unified the unit of account and required silver coins of varying fineness from different jurisdictions to be credited according to their actual metal content. It replaced the cumbersome circulation of physical silver with ledger-based credit, transforming money from a metallic object into a series of entries in an accounting system. At the same time, it committed to maintaining full-value redemption of its bank money, making the value basis behind it clearly verifiable. More importantly, it consolidated previously dispersed private clearing networks into a standardised and verifiable settlement mechanism, improving the efficiency and reliability of cross-border transactions. As a result, the Amsterdam bank florin served, over much of the seventeenth and eighteenth centuries, as a leading European clearing medium and reserve asset, and is widely regarded as an important institutional precursor to the Dutch guilder.

Concurrently, the Dutch East India Company’s 1602 joint-stock innovation, together with the establishment of the Amsterdam Stock Exchange, helped integrate securities markets into the financing of transnational commerce. This contributed to a level of financial-market depth that purely metallic circulation could not by itself provide. The guilder, accordingly, was widely used in regional trade and settlement and increasingly supported more complex financial transactions, becoming, alongside the Spanish silver, one of the dominant currencies in global commercial life.

The shift in the core of the international monetary system from the Spanish silver dollar to the Dutch guilder marked a transition in international monetary competition: from a focus on metallic content toward competition in technology, financial-market development, and institutional design. Economies that could organise settlement more effectively, reduce transaction costs, and provide stable and credible financial infrastructure were more likely to see their currencies move toward the centre of the international monetary system.

II. The Classical Gold Standard (1816–1914)

Between the sixteenth and seventeenth centuries, the Spanish real de a ocho and the Dutch bank florin became the most widely used media for cross-border settlement, supporting early forms of international clearing. Yet there was still no unified and stable set of institutional rules at the international level. It was only with the consolidation of the gold standard in the nineteenth century that the international monetary system entered its first institutionalised order.

The emergence of the gold standard was driven by the pursuit of exchange-rate stability and transactional efficiency. From the late eighteenth century through the mid-nineteenth century, Britain rose rapidly amid the Industrial Revolution. International trade and capital flows expanded dramatically, while railways, steamships, and the telegraph increasingly integrated global markets. At the same time, national monetary arrangements were fragmented: silver standards, bimetallic regimes, and various forms of local paper currency coexisted. Exchange rates were volatile, settlement was costly, and merchants and bankers bore substantial exchange losses and credit risks. Under such conditions, fixed exchange rates became a shared objective. They reduced uncertainty in cross-border transactions, mitigated exchange-rate risk, and allowed the flows of goods and capital to operate within a unified pricing framework.

It was against this backdrop that the classical gold standard took shape. The system’s origins lay in Britain. Interestingly, a key step toward gold’s dominance began with an unintended development. In 1717, Sir Isaac Newton, better known as a physicist but then serving as Master of the Royal Mint, fixed the official price of gold per ounce in an effort to standardise Britain’s coinage system. Because the resulting valuation set gold “too cheaply” relative to silver, it unintentionally made gold cheaper than silver and gradually drove silver coins out of circulation. [Strictly speaking, Newton’s concrete move was to recommend fixing the guinea at 21 shillings; the “per ounce” figure is an implied mint price derived from that legal rating. —Yuxuan’s note]

In 1816, Britain enacted the Coinage Act, which legally established gold as the standard metal, specified the gold content underpinning the monetary unit, and relegated silver to subsidiary status. In addition, advances in minting technology provided a practical foundation for the regime’s implementation. That same year, the Bank of England adopted steam-powered presses and expanded its capacity for high-volume, standardised coin production, which helped strengthen the credibility and reliability of the coinage system.

By the mid-nineteenth century, as London became the world’s financial centre, sterling’s stable gold parity helped attract global capital. Sterling was not merely a means of payment but also a symbol of creditworthiness. To secure access to sterling finance and integrate into global trade networks, other countries increasingly emulated Britain’s institutional arrangements. Until around 1880, major capitalist economies, including the United States, Germany, and the Netherlands, converged on the gold standard, giving rise to an international gold standard system centred on sterling and anchored in gold.

Between 1914 and 1944, the gold-standard order broke down, and the international monetary system experienced a prolonged period of instability that spanned the two world wars. The 1929 U.S. stock market crash triggered the Great Depression, and as international trade contracted and international capital chains collapsed, countries’ monetary arrangements fell in succession. In September 1931, as gold reserves drained from the Bank of England beyond control, Britain was forced to abandon the gold standard. In 1933, the Roosevelt administration devalued the dollar and prohibited private gold holdings. France and its partners in the so-called “gold bloc” (including Belgium and Switzerland) attempted to maintain gold parity for longer, but by 1936, the bloc had collapsed, and remaining members abandoned the standard.

As the monetary system plunged into disorder, countries competed through currency devaluations, exchange controls, and trade barriers, unleashing a wave of beggar-thy-neighbour policies. This fragmentation of the monetary order further intensified trade protectionism and geopolitical antagonism, and laid the groundwork for the outbreak of the Second World War.

III. The Bretton Woods System (1944–1971)

The rise and fall of the gold standard revealed the trade-offs in choosing an exchange-rate regime. Fixed exchange rates can deliver stability, but they often shift the burden of external adjustment onto domestic prices and employment. Yet a regime of fully flexible exchange rates, if left entirely to market forces, can produce large swings and invite competitive devaluations, risking a return to the disorder that followed the collapse of the gold standard.

After the Second World War, the international community widely concluded that a “fixed but adjustable” order was needed (Eichengreen, 1993). The new framework should have adjustable pegs to facilitate international trade, while using capital controls to preserve room for domestic policy objectives.

In 1944, the Allied powers met at Bretton Woods, New Hampshire. Owing to its unrivalled economic strength, deep financial markets, and high institutional credibility, the United States occupied the core position in the new order. The system established a dollar-centred regime: the U.S. dollar was pegged to gold at $35 per ounce, and other currencies were pegged to the dollar. The conference also created the International Monetary Fund (IMF) and the World Bank, intended to support exchange-rate stability, manage balance-of-payments strains, and finance postwar reconstruction, thereby providing the institutional foundations of the new monetary order.

In the early postwar years, Europe and Japan were still emerging from devastation, with constrained productive capacity and persistent external deficits. International liquidity, therefore, depended heavily on U.S. outflows—through aid (notably the Marshall Plan), military spending abroad, and outward investment. Over time, however, the system’s internal tensions accumulated as the global balance of economic power shifted. By the 1950s and 1960s, Europe and Japan had largely completed reconstruction and rapidly strengthened their manufacturing competitiveness. As the U.S. share of world GDP declined from nearly one-half in the 1940s to roughly a quarter by the early 1970s, the United States current-account surplus could no longer offset capital-account deficits. The counterpart was a growing stock of foreign-held dollar claims, which had come to exceed U.S. monetary gold holdings.

In addition, from 1965 onward, expansionary fiscal pressures—including Great Society programmes during President Lyndon B. Johnson’s administration and the costs of the Vietnam War—further weakened confidence in the dollar (Obstfeld, 2025). On 15 August 1971, the United States suspended the dollar’s convertibility into gold. By 1973, the major industrial economies had largely moved to floating exchange rates, marking the effective collapse of the Bretton Woods system.

IV. The Jamaica System (1976–Present)

Following the breakdown of Bretton Woods, the par-value system and the institutional constraints associated with fixed exchange rates effectively came to an end. The Jamaica Agreement, ratified by the IMF in 1976, legalised this new reality by recognising the legitimacy of floating exchange rates and granting members greater autonomy in choosing their exchange-rate regimes.

Because the United States retained a dominant position in the world economy and global finance, and because of the inertia of network effects, the U.S. dollar remained at the core of the system, resulting in a de facto dollar standard. This post-1970s order is often referred to as the “Jamaica system”. Yet, in the absence of binding, system-wide rules on exchange-rate arrangements or a robust mechanism for international balance-of-payments coordination, the Jamaica system is not a coherent institutional framework. Its operation relies more heavily on market forces and national decision-making, and is therefore frequently described as a “non-system” or “a system of no system”(Ocampo, 2017; Eichengreen, 2019).

The years from 1971 to 1990 were a phase of chaos. As fixed parities collapsed and countries were no longer bound by dollar pegs, many governments sought to relieve domestic imbalances and support exports through currency depreciation. Major industrial economies moved away from pegs toward floating arrangements. Key currencies, including the U.S. dollar, sterling, the Italian lira, and the French franc, experienced sharp swings in both directions, sending the international monetary system into prolonged turbulence. Policy divergence became more pronounced, and cross-border capital mobility intensified. Meaningful exchange-rate coordination among the major advanced economies resumed only after the 1985 Plaza Accord.

Between 1990 and 2015, some countries participated in arrangements resembling a Bretton Woods cycle. Several scholars labelled this configuration “Bretton Woods 2.0”, which can be treated as a “fragment” order within the broader Jamaica-era monetary environment. The dollar remained the core currency, but the countries playing peripheral and semi-core roles shifted. In the original Bretton Woods system, Western Europe and Japan, through decades of capital accumulation and industrial upgrading, moved from peripheral countries into the “semi-core” of the international monetary system (Eichengreen, 2004).

Meanwhile, emerging Asian economies and energy-exporting countries became the new periphery of the monetary system. They maintained long-term, de facto dollar pegs or crawling pegs to support export competitiveness, accumulated large U.S.-dollar foreign-exchange reserves through export-led growth, and recycled those reserves into U.S. Treasuries (Dooley, Folkerts-Landau, and Garber, 2003, 2004).

In August 2015, China further advanced exchange-rate reform, shifting away from a de facto dollar peg toward a managed floating regime based on market supply and demand with reference to a basket of currencies. This change increased the exchange-rate flexibility of peripheral countries and signalled the end of Bretton Woods 2.0.

As global growth dynamics moved from a predominantly U.S.-centred pattern toward a more dual-engine structure featuring both the United States and China, tensions between economic and trade multipolarity and monetary unipolarity intensified. The internal balance of the dollar-centred system has consequently come under greater strain. On one hand, China’s economic weight rose markedly, supported by an increasingly comprehensive manufacturing base and growing capabilities in frontier technologies. In 2014, on purchasing-power-parity (PPP) measures, China’s GDP surpassed that of the United States for the first time. In emerging technological domains such as artificial intelligence, the two economies increasingly operate in parallel competition. On the other hand, the relative advantage of the U.S. economy has narrowed, while fiscal deficits and public debt burdens have increased. It has also increasingly abused its financial hegemony, prompting countries around the world to begin seeking alternatives to the U.S. dollar.

Chapter 2: Why Does Money Exhibit an Inherent Order?

A review of the historical evolution of the international monetary system suggests that, for most periods, it has displayed a stable “core–periphery” structure. Even after the breakdown of the gold standard and the collapse of the Bretton Woods system, brief episodes of disorder were followed by the re-emergence of a new centre and the restoration of order. What underlying mechanism makes money appear “inherently ordered”?

I. The Nature of Money

To understand how monetary order forms, it is necessary to begin with the nature of money itself. Money can be understood as a trust-based social contract (Ingham, 2004). Its value rests on the issuer’s obligation to the holder. People accept money not because it has intrinsic value, but because of a social belief that it will continue to be accepted by others and can be used to settle debts and discharge obligations. In this sense, money is a “higher-order belief”: individuals accept a currency not only because they believe it is valuable, but because they believe others will continue to accept it, thereby producing a stable collective consensus.

Mainstream accounts assign the state a decisive role in sustaining this trust framework (Keynes, 1936; Borio, 2019). On the one hand, the state relies on the coercive force of law to require society to use the currency it issues—namely, its status as legal tender. On the other hand, the state must also safeguard the currency’s capacity to discharge obligations by maintaining sustained fiscal solvency and relatively robust institutional credibility.

In The General Theory of Employment, Interest and Money, Keynes (1936) uses the concept of the “own-rate of interest” to distinguish money from other assets. He defines the total return from holding an asset over a period as its yield (q) minus its carrying cost (c) plus its liquidity premium (l), so that the own-rate is q − c + l. In this framework, money’s yield is close to zero, and its carrying cost is negligible, but its liquidity premium is substantial because of its general acceptability. As Keynes puts it, it may be “the greatest of the own-rates of interest.” At the same time, as the nominal unit of account, money’s value does not automatically adjust with future changes in relative prices. This further strengthens the stability of its own-rate of interest and anchors money in the most secure position within the overall interest-rate structure.

The decisive role of the state in this trust architecture endows sovereign money with coercive backing and credibility support, which is also core to understanding how sovereign currencies differ, in essence, from crypto-assets such as stablecoins. In its Annual Economic Report 2025 discussion of stablecoins and the future monetary system, the Bank for International Settlements (BIS) frames a sound monetary system as requiring three core attributes: singleness, elasticity, and integrity. When these conditions are met, money is better able to perform its three basic functions as a medium of exchange, a unit of account, and a store of value.

These functions generate powerful network effects that make money a natural monopoly and provide the economic foundation for the emergence of order. The more widely a currency is used, the greater its liquidity and the more convenient transactions become, which in turn attracts more users and creates a self-reinforcing positive-feedback loop. This gives money an inherent natural-monopoly tendency, drawing monetary use toward centralisation. By doing so, it resolves the “double coincidence of wants” problem and substantially lowers coordination costs.

In sum, within a domestic context, the combination of political coercion and economic natural-monopoly effects tends to ensure monetary concentration and unity.

II. Characterising Monetary Order: From the Pyramid to the “Core–Periphery” Model

At the international level, however, there is no global government with universally recognised authority. There is neither an effective capacity for coercive enforcement nor a stable institutional guarantee. Against this backdrop, free competition plays a more important role in the international monetary system. As early as The Denationalisation of Money (1976), Friedrich Hayek advanced the idea of currency competition, arguing that, within a single country, currencies should be allowed to compete freely, with market selection favouring those that best preserve purchasing power and maintain stable credibility.

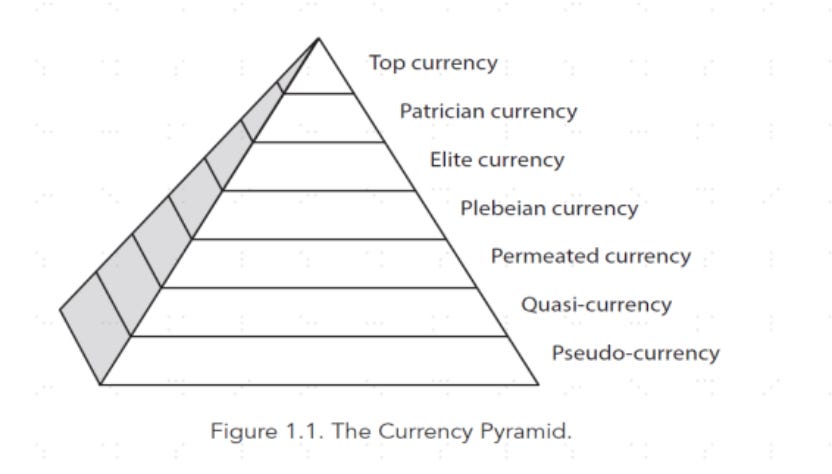

Scholars have characterised the international monetary order from different analytical angles. One is the “currency pyramid” approach, associated with Susan Strange (1971) and Benjamin Cohen (2015), which depicts the world’s currencies as forming a steep hierarchy. Another is the “core–periphery” approach, associated with Dooley, Folkerts-Landau, and Garber (2003, 2004), which highlights the asymmetric power relationship between a small number of core currencies and the large majority of peripheral currencies.

(1) The “Currency Pyramid” Framework

Benjamin Cohen (2015) classifies currencies into seven tiers according to their degree of global use, acceptance, and trust. At the top are top currencies, which comprehensively dominate international trade, reserves, and financial settlement, such as sterling in the nineteenth century and the U.S. dollar in the twentieth century. Below them are patrician currencies, which perform major functions at the regional level, such as the euro and the Japanese yen. Elite currencies have more limited international roles but are issued by states with high credibility, such as sterling (in its contemporary role), the Swiss franc, the Australian dollar, and the Canadian dollar. Plebeian currencies are used only for some trade invoicing and settlement, and have limited reserve and investment functions; examples include the Nordic currencies, the Korean won, the Singapore dollar, and the currencies of some Middle Eastern oil-exporting states. Permeated currencies, because of unstable value, serve only to a limited extent as media of exchange and units of account, and are more commonly observed in parts of Latin America and Southeast Asia. Quasi-currencies are largely displaced by foreign currencies, such as the Zimbabwe dollar, in episodes of extreme inflation. At the lowest tier are pseudo-currencies, which have virtually lost monetary-policy independence and exist primarily in symbolic form—for example, the Panamanian balboa, with the U.S. dollar functioning as the effective circulating currency domestically.

The pyramid illustrates a hierarchy among currencies in the international domain. From the apex to the base, the international functions that currencies can perform diminish step by step: top-tier currencies perform almost the full set of international monetary functions, whereas the lower the tier, the fewer functions a currency can reliably perform. In the lowest tiers in particular, some currencies cannot fully perform even basic monetary functions within their own domestic economies.

(II) The “Core–Periphery” Framework

Some scholars describe the international monetary system through a “core–periphery” lens. The concept was first advanced in the study of international politics (Prebisch, 1950) to highlight inequality in the international division of labour. In this view, core economies command technology and capital and possess pricing power, whereas peripheral economies mainly export primary commodities, face persistently unfavourable terms of trade, and receive an income share far below that of the core.

This structural perspective was later applied to the international monetary system. Under such an application, core countries issue international reserve currencies and therefore enjoy greater policy autonomy, and can benefit from resource transfers associated with seigniorage and liquidity premia; peripheral countries, by contrast, effectively “pay” seigniorage and are more often placed in a reactive position regarding policy space (Bordo & Flandreau, 2001).

For example, Bretton Woods produced a layered structure of “dollar–gold–other currencies”. During postwar reconstruction, Europe and Japan accumulated large amounts of dollars through exports. To maintain fixed exchange rates under Bretton Woods, these dollars largely had to be recycled back to the United States—either through purchases of U.S. Treasury securities or via official reserve holdings. Put differently, the core country was able to exchange next-to-no-cost monetary liabilities for real resources from the periphery.

The French economist Jacques Rueff illustrated this logic with a vivid metaphor. A tailor (Europe and Japan) makes suits for a customer (the United States). After being paid, the tailor returns the same money to the customer as a loan, and the customer uses the loan to buy more suits. The cycle repeats: promissory notes pile up and suits multiply, yet the customer never has to pay in “hard” money, relying instead on credit to obtain a continuous flow of goods. Rueff’s question was: if the tailor ever demanded that the promissory notes be converted into cash, would the customer still be able to pay?

Under the Jamaican system, the power asymmetry between core and peripheral economies has become even more pronounced. On the one hand, the cycle of “money exchanged for resources” continues. The dollar’s status as the primary reserve currency sustains global investors’ preference for U.S. Treasury securities and other dollar assets, enabling the United States to borrow large amounts at low cost and to avoid adjustments even when international payments are imbalanced.

In this phase, the peripheral countries can be divided into two broad groups. One consists of export-oriented East Asian economies and energy-exporting countries. By running trade surpluses, they accumulate dollars and purchase large quantities of U.S. Treasury securities—so that the United States can exchange paper liabilities for real resources (the group emphasised in “Bretton Woods 2.0”). The other consists of peripheral economies in Europe and Latin America, where investors purchase large amounts of U.S. financial assets such as equities and bonds, allowing the United States to attract real capital that can be used for domestic investment or outward expansion (Zhang Ming and Qin Donghai, 2005).

On the other hand, capital-account opening has intensified the asymmetry inherent in the core–periphery structure. Under Bretton Woods, most countries maintained strict controls on capital movements, so the cross-border spillovers of U.S. monetary policy were relatively limited. In the context of contemporary financial globalisation, however, many countries have substantially relaxed or even removed capital controls. The Federal Reserve sets monetary policy primarily in line with domestic conditions, but its decisions generate significant cross-border spillovers, triggering large-scale capital inflows and outflows. This not only weakens the monetary-policy autonomy of peripheral economies, but has also repeatedly contributed to episodes of financial turmoil and even crisis in these countries.

Chapter 3 The Driving Forces of International Monetary Order

Within a “core–periphery” international monetary order, only a very small number of currencies occupy the core at any given time. In my view, the status of a core currency is not shaped by a single factor. Rather, it is the result of multiple forces working together, including economic strength, financial depth, institutional credibility, and technological change. This status is also reinforced by the natural-monopoly tendency created by network externalities, as well as by the institutional barriers erected by core states. It is the joint effect of state power and monopoly mechanisms that makes international currency competition persistently concentrated and stable.

I. Determinants of Monetary Order

(1) Economic strength provides a solid demand foundation for a core currency

Cross-border currency use is not exogenously imposed; it is endogenous to real trade in goods and services. Chinn and Frankel (2007) emphasise that, among the long-run determinants of international currency status, the most important is the size and share of global trade of the country in which the currency is indigenously used. Only when a country achieves structural dominance in economic scale, production capacity, and trade networks can its currency generate stable and broad international demand, thereby providing a solid demand foundation for currency internationalisation.

The larger an economy is, and the more complete its supply chains are, the stronger the willingness and convenience for trade partners to invoice and settle in its currency. Historically, the international rise of sterling in the nineteenth century and the U.S. dollar in the twentieth century both rested on a strong economic base and extensive trade networks.

(2) Financial markets as the functional anchor of a core currency

Economic scale provides the foundation for trade settlement, but the maturity of financial markets determines whether a currency can move beyond trade invoicing and settlement and take on higher-order functions such as a store of value and an investment vehicle. Only capital markets with sufficient depth, breadth, and liquidity can support these roles (Obstfeld, 2017; Eichengreen, 2019). Active and open financial markets allow foreign investors to participate on an ongoing basis in financial transactions denominated in the home currency, thereby creating a large and stable base of asset holders. The development of derivatives markets and offshore markets further enhances the currency’s liquidity within the global financial system.

The historical rise of the U.S. dollar underscores the importance of financial markets. Although the United States had surpassed the United Kingdom in economic size by the late nineteenth century, international capital continued to rely on London due to the underdevelopment of U.S. financial markets. After the Second World War, the expansion of the U.S. Treasury market, greater financial openness, and improved asset liquidity established the dollar’s dominant position under the Bretton Woods system. In the 1960s, the rise of the Eurodollar market further strengthened the dollar’s international liquidity, enabling it to retain global core status after Bretton Woods collapsed through extensive offshore financial networks.

(3) Institutional frameworks are the trust foundation of a core currency

The rise of a core currency is, in essence, a process in which a country’s institutional credibility is extended from the domestic sphere to the international arena. Domestically, institutional arrangements clearly matter, but the state can also use coercion to sustain the baseline credibility of its currency. As a result, even under moderate inflation or short-lived financial volatility, residents typically do not abandon the national currency.

In international competition, however, only when a country’s institutional arrangements are sufficiently stable, transparent, and rule-bound can its currency plausibly move toward the centre of the global system. Historical experience repeatedly suggests that currency internationalisation relies on credible institutional constraints, and that decline is often associated with institutional breakdown. Early modern Spain and France experienced severe fiscal stress and repeated sovereign defaults, which weakened their monetary standing in international commerce. Likewise, the 1971 “Nixon Shock”—the unilateral suspension of the dollar’s convertibility into gold—illustrates how the loosening of an institutional commitment can erode global confidence.

By contrast, Britain’s trajectory highlights how institutionalised credibility can underpin monetary ascendancy. After the Glorious Revolution, Parliament’s enhanced control and oversight of public finance constrained discretionary royal spending, laying a foundation of trust that enabled sterling to become a world currency.

(4) Technological transformation as a reshaper of monetary form and economic structure

Technology shapes the form of money not only by changing how payments, clearing, and value storage are carried out, but also by raising productivity and reconfiguring patterns of trade and finance. In doing so, it can shift the global centre of wealth and provide a solid real-economy foundation for the rise and replacement of core currencies.

Almost every major transformation in monetary form has stemmed from the combination of institutional innovation and enabling technological conditions. In the seventeenth century, the Dutch Republic established the world’s first system of “bank money” through the Bank of Amsterdam’s deposit-ledger regime, replacing the physical circulation of precious metals with book-entry deposit clearing. This substantially improved transactional security and efficiency and helped elevate the Dutch guilder to a leading international currency of the period. Centuries later, financial infrastructures such as SWIFT and CHIPS, through standardised messaging and electronic clearing, further increased the efficiency of cross-border payments and reinforced the U.S. dollar’s settlement and circulation advantages within global financial networks.

Historically, the countries that issue central currencies have often stood at the apex of both institutions and technology. In the nineteenth century, Britain leveraged the First Industrial Revolution to establish industrial and commercial leadership: steam power, railways, and ocean shipping significantly raised productivity and expanded global trade capacity. At the same time, post–Glorious Revolution reforms strengthened fiscal constraints and parliamentary oversight, providing a more credible institutional foundation for sterling. The combination of technological progress and institutional innovation enabled sterling to become the first truly “global currency” (Eichengreen, 1996; 2011).

In the twentieth century, the United States drew on the technologies of the Second Industrial Revolution—electricity, chemicals, and automobiles—to reshape global production and, through the creation of the Federal Reserve and the Bretton Woods, completed the transition in monetary leadership from sterling to the dollar (Eichengreen, 2011).

For these reasons, technological revolutions may not directly “manufacture” monetary hegemony. But by reshaping production, trade, and finance—and by interacting with institutional design—they can become a key driving force behind the formation of core currencies.

Today, a new wave of technological change centred on artificial intelligence may be incubating a structural turning point comparable to the Industrial Revolution. As a new general-purpose technology (GPT), AI is not merely a technical breakthrough; it is a technological paradigm capable of diffusing across sectors and systematically reshaping production processes and the allocation of factors of production.

On the technology side, AI development follows the “scaling law” (Kaplan et al., 2020). As investment in parameter count, training data, and compute increases, model performance does not improve in a purely linear way; rather, once certain scale thresholds are crossed, performance can appear to jump discontinuously, with models exhibiting new reasoning and generalisation capabilities—so-called “emergence” (Wei et al., 2022; OpenAI, 2023).

On the economic side, these technological regularities translate into scale effects and network externalities (Agrawal, Gans & Goldfarb, 2019; Cockburn, Henderson & Stern, 2018). As AI becomes embedded across production, finance, logistics, and consumption, the agglomeration of data and computing power generates positive-feedback effects, raising total factor productivity and reinforcing the concentration of economic activity, capital flows, and knowledge production (BIS, 2023).

Therefore, AI not only reshapes global value chains and cross-border capital flows; it may also confer new structural advantages within institutional and monetary systems on countries that control core computing capacity and algorithmic standards. In this sense, AI may represent a transformation comparable in depth to the Industrial Revolution—not only rewriting methods of production, but also reshaping macroeconomic structures and financial systems, and providing key momentum for the emergence of a new centre in the international monetary order.

(5) Must a dominant currency be backed by military power? The “Mars vs. Mercury” debate

Must a leading currency necessarily be issued by a military great power? Kindleberger’s (1973) hegemonic stability theory emphasises that a hegemon’s preponderant military capabilities are central to sustaining international economic and political stability. In May 2025, European Central Bank President Christine Lagarde also made a rare remark in Berlin, arguing that any enhanced global role for the euro would need to coincide with greater military strength that could credibly back Europe’s partnerships. Such remarks were noteworthy because central bank leaders rarely address defence issues in monetary-policy settings.

There is little doubt that monetary credibility is rooted in state sovereignty, and that the maintenance of sovereign credibility is intertwined with the security and stability that military capabilities underwrite. Military strength, therefore, plausibly provides important support for the formation and maintenance of a core currency. The key question, however, is how strong that support is: does military power exert a direct causal effect on international currency status?

This question reflects a longstanding debate in the literature. As Eichengreen, Mehl, and Chiţu (2019) vividly put it, it is often framed as a contrast between “Mars” and “Mercury”.

The “Mars” metaphor draws on Mars, the Roman god of war, which evokes force and conquest. On this view, the status of an international reserve currency rests on the backing of military and security arrangements (Kindleberger, 1973; Krasner, 1976). A hegemonic state reinforces confidence in its currency by supplying global public goods—such as security provision and the protection of key trade routes and corridors—thereby sustaining external stability in the geopolitical order. From this perspective, the formation and maintenance of the dollar system have been underpinned by the United States’ worldwide military presence and its security commitments.

By contrast, the “Mercury” metaphor draws the Roman god of commerce and communication, symbolising rationality and communication. The “Mercury” view holds that the core competitiveness of an international currency derives from the endogenous stability of the issuer’s economic and financial system (Eichengreen, 2011; Cohen, 2015; Helleiner, 2023). Institutionalised credibility, the depth of capital markets, and transparent rule-of-law arrangements provide a more durable basis for trust than military power. In this sense, open financial systems and predictable policy rules can generate “institutionalised security”, reducing reliance on military guarantees as the source of monetary credibility.

In my view, the relationship between military power and international currency status is closer to co-movement than to causation. Military capability is typically a derivative of economic, financial, and institutional strengths, rather than their original source. Economic prosperity generates fiscal resources and innovation capacity that make sustained military power possible, but military expansion, by itself, does not automatically translate into international monetary credibility. The Soviet Union, for example, possessed formidable military strength during the Cold War, yet it did not build an international currency network capable of rivalling the U.S. dollar.

On the surface, shifts in core-currency leadership have often coincided with major wars or geopolitical upheavals. Yet military victory is better understood as a catalyst that releases pre-existing structural forces. By disrupting an established order and breaking its “lock-in”, war can open a window through which a country whose economic, financial, and institutional advantages have already become decisive can translate those advantages into monetary ascendency. In this sense, war does not “create” a new central currency; it accelerates the crystallisation of underlying economic and financial strength. The Anglo–Dutch Wars weakened Dutch fiscal and naval capacity, widening Britain’s opportunity to rise on the back of industrialisation and the gold-standard regime. The two World Wars, in turn, weakened Britain’s fiscal position and industrial base, enabling the United States—backed by a comprehensive industrial system, net creditor status, and strong capacity to provide financial support—to effect the postwar shift in monetary leadership from sterling to the dollar through the Bretton Woods system (Eichengreen, 1996; 2011; Kennedy, 1987).

War, therefore, is best understood as a trigger in the evolution of monetary systems, not a fundamental driver. Its main role is to “open a time window” for change, rather than to substitute for the underlying economic, financial, and institutional forces. When shifts in relative power are unfolding but remain locked in by an existing order, war can rapidly break the equilibrium, force states back to the bargaining table, and accelerate the redesign of institutional arrangements (Eichengreen, 2019). But battlefield victory alone—without the support of economic depth, financial innovation, and institutional trust—rarely enables a country’s currency to move to the centre of the international monetary order.

Returning to Lagarde’s remarks, rebuilding Europe’s military capacity could bolster the euro’s international standing. However, the euro’s decline reflects deeper structural constraints, including fragmented fiscal arrangements, segmented capital markets, and an insufficient supply of safe assets. More importantly, the euro’s fundamental problem is Europe’s structural growth stagnation. Europe has not only missed much of the digital-revolution wave; it is also at a disadvantage in emerging industries such as artificial intelligence. This deeper loss of economic dynamism erodes the euro’s long-term value and credibility at the root.

In sum, the forces that propel a currency toward core status do not operate in isolation; they can form mutually reinforcing feedback loops. A strong economic base supports deeper financial markets, and financial depth in turn improves the efficiency of allocation. Institutional advantages attract and retain capital and talent, reinforcing financial development and technological innovation. Technological progress can lower transaction costs, increasing a currency’s attractiveness and expanding the scale of economic and financial activities. Meanwhile, military strength underpins sovereign credibility and provides a stable external environment conducive to economic development, while economic growth supplies fiscal capacity for defence. Through this co-evolution, core-currency status is sustained and consolidated.

II. The Formation of Monopolistic Competition

Economic, financial, institutional, technological, and military factors are all important, but they do not fully explain two stylised facts: why the number of currencies at the apex of the global “pyramid” is extremely small, and why, in a “core–periphery” order, the genuinely core currencies have always been limited to only a few.

In principle, countries have a natural incentive to use their own currencies in international trade and financial transactions. One might therefore expect the international use of currencies to correspond broadly to relative economic and financial size, producing a pluralistic and competitively open landscape with currencies of different scales. In practice, however, both the pyramid structure and the core–periphery system exhibit a distinctly concentrated, often unipolar or few-pole-dominated, monopolistic pattern. This suggests that, beyond the factors discussed above, additional market mechanisms help shape the order of the international monetary system.

One way to frame this is through the lens of market-structure theory in economics. Depending on the number of participants, product differentiation, barriers to entry, and the degree of market power, market structures are typically classified as perfect competition, monopolistic competition, oligopoly, and monopoly.

Monopolistic outcomes—including oligopoly and near-monopoly—often arise from different forces. For example, the value of a product or platform increases with the number of users. Once a firm or a standard gains a first-mover advantage, it can attract additional users and further entrench its lead, generating a natural monopoly; familiar examples include telephone networks, payment networks, and operating systems. In other cases, governments or industry bodies create exclusivity through licensing regimes or standard-setting, producing administrative monopolies—for example, in tobacco, gambling, or telecommunications licensing.

The near-monopolistic structure of the international monetary system reflects the joint operation of these mechanisms. The first is network externalities. As more economic actors adopt the same currency for trade invoicing, financing, and reserves, that currency’s liquidity and perceived safety tend to increase, which further strengthens incentives to keep using it. As a result, even transactions that do not directly involve the issuing country may gravitate toward the core currency. This self-reinforcing positive feedback gives international currency competition a “winner-takes-most” character. The U.S. dollar consolidated its core position precisely through this channel: U.S. Treasury securities became the world’s most liquid safe asset, and the dollar became a leading vehicle for offshore financing and cross-border settlement.

The second mechanism is the institutional entry barriers that create a form of administrative monopoly. Once a currency achieves a dominant position, its issuer can further lock in that position by shaping global clearing and settlement arrangements, influencing regulatory standards, supplying safe assets, and exercising leverage over critical financial infrastructures. After the Second World War, the dollar was institutionalised as the key reserve currency under Bretton Woods. Over time, the Federal Reserve’s dollar swap arrangements evolved into an important global liquidity backstop. Key nodes in cross-border finance—including the SWIFT messaging network, major clearing banks, and cross-border custody and settlement systems—also developed in ways that were deeply dollar-centred in practice. The result is that nearly all institutional infrastructure for international transactions, financing, regulation, and clearing has come to operate around the dollar as its default reference point.

In sum, the highly monopolistic structure of the international monetary system reflects not only cross-national disparities in economic, financial, and institutional capacity, but also the interaction between natural-monopoly dynamics driven by network externalities and the institutional barriers constructed by core states. It is the combined effect of state power and market mechanisms that produces a persistent and stable monopolistic configuration in international monetary competition.

References

Agrawal, Ajay, Joshua Gans, and Avi Goldfarb. 2019. Prediction Machines: The Simple Economics of Artificial Intelligence. Harvard Business Review Press.

Bank for International Settlements (BIS). 2023. Annual Economic Report 2023. Basel: BIS.

Bank for International Settlements (BIS). 2025. Annual Economic Report 2025, Chapter III: “The next-generation monetary and financial system.” Basel: BIS.

Borio, Claudio. 2019. “On money, debt, trust and central banking.” BIS Working Papers No. 763. Bank for International Settlements.

Bordo, Michael D., and Marc Flandreau. 2001. “Core, Periphery, Exchange Rate Regimes, and Globalization.” In Globalization in Historical Perspective, edited by Michael D. Bordo, Alan M. Taylor, and Jeffrey G. Williamson. University of Chicago Press.

Chinn, Menzie D., and Jeffrey A. Frankel. 2007. “Will the Euro Eventually Surpass the Dollar as Leading International Reserve Currency?” In G7 Current Account Imbalances: Sustainability and Adjustment, edited by Richard H. Clarida. University of Chicago Press.

Cockburn, Iain M., Rebecca Henderson, and Scott Stern. 2018. “The Impact of Artificial Intelligence on Innovation.” NBER Working Paper No. 24449.

Cohen, Benjamin J. 2015. Currency Power: Understanding Monetary Rivalry. Princeton University Press.

Dooley, Michael P., David Folkerts-Landau, and Peter Garber. 2003. “An Essay on the Revived Bretton Woods System.” NBER Working Paper No. 9971.

Dooley, Michael P., David Folkerts-Landau, and Peter Garber. 2004. “The Revived Bretton Woods System.” International Journal of Finance & Economics 9(4): 307–313.

Eichengreen, Barry. 1993. Golden Fetters: The Gold Standard and the Great Depression, 1919–1939. Oxford University Press.

Eichengreen, Barry. 1996. Globalizing Capital: A History of the International Monetary System. Princeton University Press.

Eichengreen, Barry. 2004. “Global Imbalances and the Lessons of Bretton Woods.” NBER Working Paper No. 10497.

Eichengreen, Barry. 2011. Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System. Oxford University Press.

Eichengreen, Barry. 2019. Globalizing Capital: A History of the International Monetary System. 3rd ed. Princeton University Press.

Eichengreen, Barry, Arnaud Mehl, and Livia Chiţu. 2017. How Global Currencies Work: Past, Present, and Future. Princeton University Press.

Hayek, Friedrich A. 1976. The Denationalisation of Money. Institute of Economic Affairs.

Helleiner, Eric. 2023. The Contested World Economy: The Deep and Global Roots of International Political Economy. Cambridge University Press.

Ingham, Geoffrey. 2004. The Nature of Money. Polity Press.

Kaplan, Jared, et al. 2020. “Scaling Laws for Neural Language Models.” arXiv:2001.08361.

Kennedy, Paul. 1987. The Rise and Fall of the Great Powers: Economic Change and Military Conflict from 1500 to 2000. Random House.

Keynes, John Maynard. 1936. The General Theory of Employment, Interest and Money. Macmillan.

Kindleberger, Charles P. 1973. The World in Depression, 1929–1939. University of California Press.

Krasner, Stephen D. 1976. “State Power and the Structure of International Trade.” World Politics 28(3): 317–347.

Obstfeld, Maurice, and Alan M. Taylor. 2017. “International Monetary Relations: Taking Finance Seriously.” Journal of Economic Perspectives 31(3): 3–28. DOI: 10.1257/jep.31.3.3.

Obstfeld, Maurice. 2025. “The international monetary and financial system: a fork in the road.” Andrew Crockett Memorial Lecture, Basel, 29 June. Bank for International Settlements.

OpenAI. 2023. “GPT-4 Technical Report.” arXiv:2303.08774.

Prebisch, Raúl. 1950. The Economic Development of Latin America and Its Principal Problems. United Nations.

Rueff, Jacques. 1963. The Monetary Sin of the West. (English translation widely circulated; publication details vary by edition.)

Strange, Susan. 1971. “The Politics of International Currencies.” World Politics 23(2): 215–231.

Wei, Jason, et al. 2022. “Emergent Abilities of Large Language Models.” arXiv:2206.07682.

Zhang, Ming (张明), and Qin Donghai (覃东海). 2005. “国际货币体系演进的资源流动分析.” 世界经济与政治, no. 12.

Ocampo, José Antonio. 2017. Resetting the International Monetary (Non)System. Oxford University Press.

Miao Yanliang: myth-busting the dollar hegemony, stablecoins, & multipolar monetary system

Miao Yanliang joined China International Capital Corporation Limited (CICC) ,a leading investment bank, in March 2023 as Chief Strategist and Executive Head of the Research Department. Before that, he served for 10 years at the China State Administration of Foreign Exchange (SAFE), part of the People’s Bank of China, including as its Chief Economist sin…

Miao Yanliang explains China's large monetary injection yet blocked transmission

Miao Yanliang joined China International Capital Corporation Limited (CICC) ,a leading investment bank, in March 2023 as Chief Strategist and Executive Head of the Research Department. Before that, he served for 10 years at the China State Administration of Foreign Exchange (SAFE), part of the People’s Bank of China, including as its Chief Economist sin…

| A guest post by

|