China's local govt debt in 2020 was 50% higher than WB, IMF estimates: David Daokui Li

Local govt debt soared after 2015, surpassing the combined revenues of local govts and profits of local SOEs, necessitating a central govt bailout, said the prominent economist at Tsinghua.

Local government debt in China amounted to 90 trillion yuan (12.49 trillion U.S. dollars) in 2020, 50% higher than the World Bank and IMF estimates, according to a recent study by Professor David Daokui Li and Zhang He of the Academic Center for Chinese Economic Practice and Thinking (ACCEPT), Tsinghua University. The study also revealed that:

The rapid accumulation of infrastructure debt is the main reason for the rapid rise in the leverage ratio of local governments and the entire real economy.

China's local government debt demonstrates a nested structure, where local governments establish entities to secure loans, and these entities, in turn, leverage those borrowed funds to acquire further financing for their subsidiaries.

Without central government intervention, local debt is unsustainable.

Prof. David Daokui Li is the Mansfield Freeman Chair Professor of the Department of Finance of the School of Economics and Management of Tsinghua University. He is also the director of ACCEPT.

The following article is the first part of the translation of Prof. Li's lecture at the 8th session of the "Government and Market Economics Series," an event organized by ACCEPT at Tsinghua University on Oct. 25. The full video of Li's lecture is available at Xueshuo, a professional knowledge dissemination platform incubated by Tsinghua. (Watching requires registration.) A transcript of his lecture appears to be first published by the New Economist WeChat blog.

Local government debt in China: dimensions, causes and impacts

Today, I will discuss the dimensions, causes, and impacts of local government debt in China, a key area of research our institute has dedicatedly analyzed over the last three to four years, with close monitoring extending back four to five years. The goal of our project is to study the scale and dimensions of China’s local government debt: How large is it? How is it structured? Is it sustainable? What are the fundamental reasons for its huge size? What impact does it have on local economic development? Of course, we also deduced how to address and resolve this issue.

Let's first briefly introduce our findings. To understand the scale, structure, and sustainability of China's local government debt, we developed an innovative measurement method.

Drawing from real-world examples, our study delves into the financial composition of infrastructure projects, with a particular focus on the diverse funding methods utilized by local authorities in these projects. We identified a key concept: "a nested structure." What does this mean? Typically, local governments register a parent company, such as a local government financing vehicle (LGFV). This parent entity secures financing with, say, 30-40% comprising borrowed capital and 60-70% being its own funds. This parent company then invests in a subsidiary, which in turn borrows more and invests in a sub-subsidiary, and so on.

Based on this pyramid structure, we studied how much local governments repay and how much new debt they acquire each year. Employing retrospective analysis and integration techniques, we gradually deduced the total debt magnitude. This research was conducted in collaboration with a former Ph.D. student from our institute who currently works at CITIC Group.

Our meticulous analysis revealed that in 2020—though these figures are somewhat dated, relying on historical data—China's local government debt approached 90 trillion yuan (12.49 trillion U.S. dollars), equating to 88% of the GDP at that time. This estimation significantly surpasses those commonly cited by most scholars. For instance, the International Monetary Fund or the World Bank typically estimate it around 60 trillion yuan (8.33 trillion U.S. dollars), roughly 50% of the GDP.

Our higher calculation stems from incorporating the nested financial structure and encompassing all debts of state-owned investment vehicles under local governments. We believe that the debts of these state-owned investment vehicles are, in essence, debts of the local governments themselves, and should not be viewed separately.

We also found that the rapid accumulation of infrastructure debt is the main reason for the rapid rise in the leverage ratio of local governments and the entire real economy.

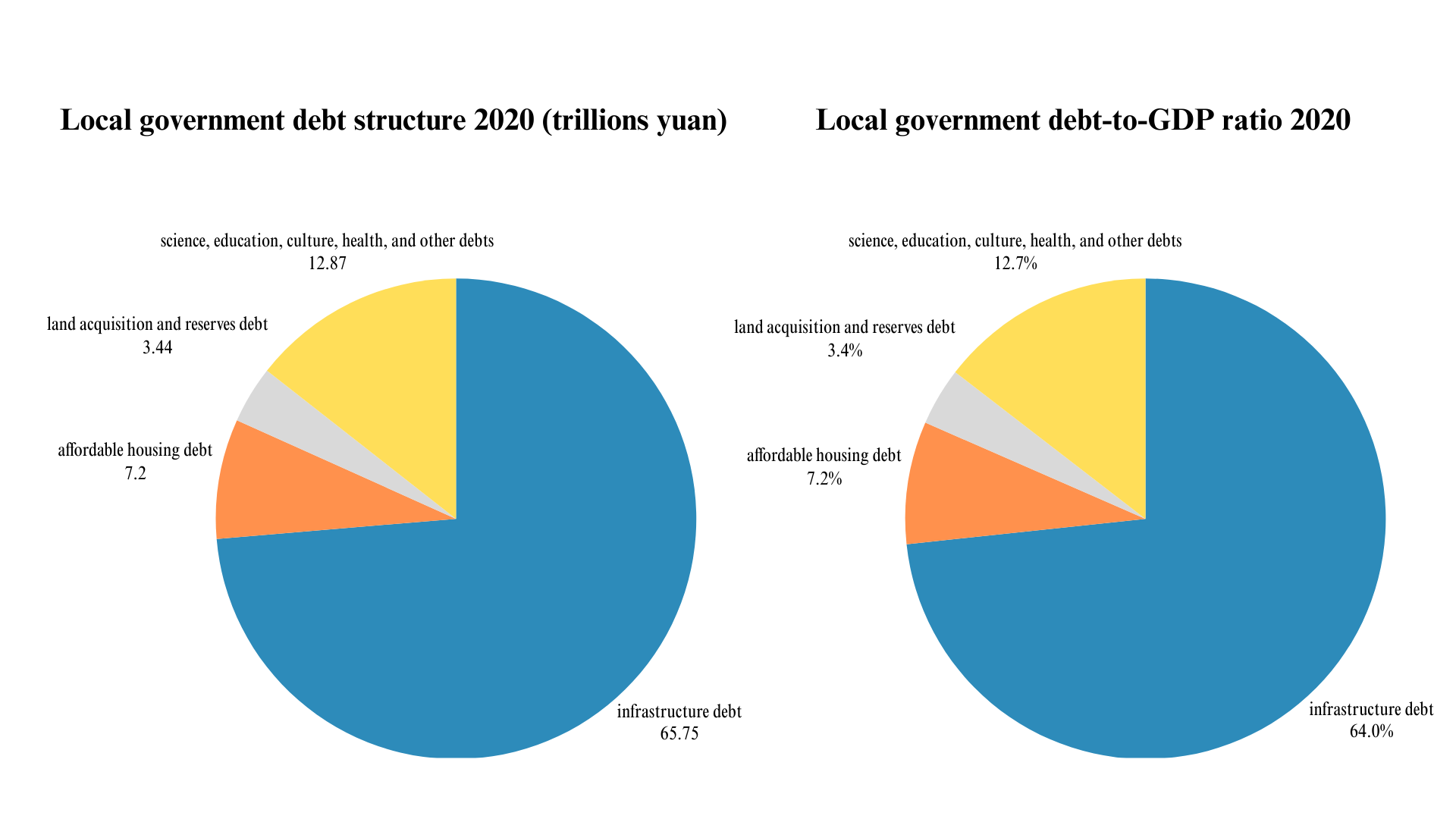

Take a look at the pie chart on the left, which displays debt calculated by amount. The infrastructure debt, the blue segment, is about 65.76 trillion yuan (9.13 trillion U.S. dollars), constituting 64% of the GDP. So it's no surprise that infrastructure debt is the main source of debt. I think for all of you researchers, this conclusion should be straightforward.

Another finding is that local state-owned enterprises (SOEs) serve as the main channel for local governments to incur debt. Local governments receive only limited budgets by approval of local people's congresses. We discovered that as of 2020, the scale of debt incurred by local SOEs for infrastructure construction stood at 50 trillion yuan (6.94 trillion U.S. dollars). Considering that the total infrastructure debt is 64 trillion yuan (8.88 trillion U.S. dollars), 50 trillion yuan was a substantial portion. The remaining 5 trillion yuan (0.69 trillion U.S. dollars) was allocated to affordable housing, which is also significant. Nevertheless, it is essential never to forget that local SOEs are the primary debtors in local government debts.

We also made an important discovery: without central government intervention, local debt is unsustainable. To assess this unsustainability, we evaluated the debt repayment capacity of local governments, factoring out essential government expenditures such as employee salaries. Our findings indicate that, after deducing these necessary fiscal expenditures, local governments have very limited capacity to repay their debts.

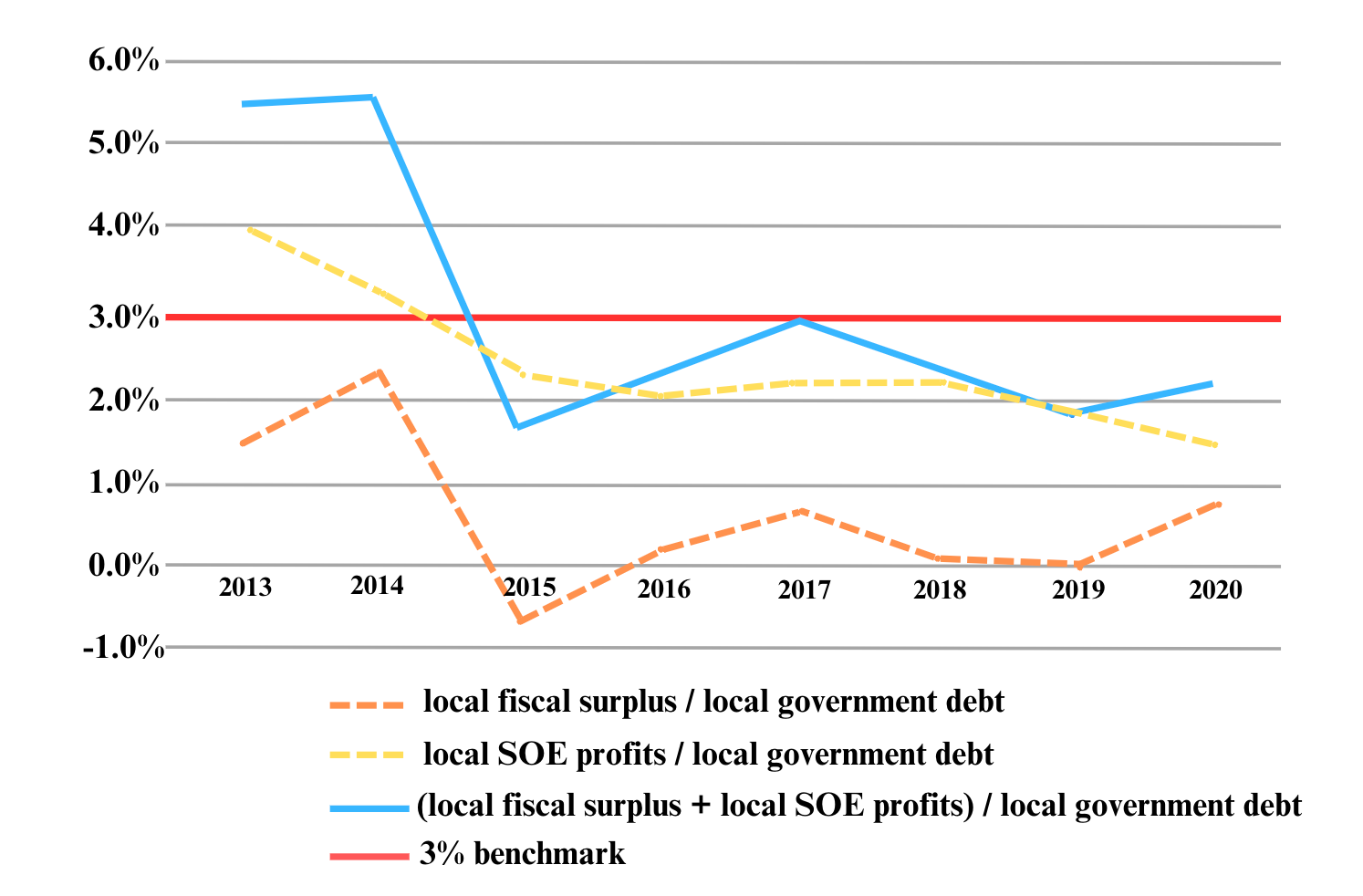

Some may think, since local SOEs are the main channel for incurring debt, why not repay these debts with the profits of SOEs? So we conducted some further analysis, as depicted in the chart below.

The lowest dotted line, the orange one, represents the local fiscal surplus divided by local government debt. Since 2016, it has consistently been below 1%, and at times even dipped into negative territory, signaling consistent fiscal deficits. The light yellow dotted line above represents the total profit of local SOEs divided by local debt. Recently, this ratio has dropped to just over 1%.

So, the sum of the fiscal surplus plus the profits of local SOEs, namely the financial resources available to local governments for debt repayment, amounts to only 2.18% of their total debt. How can this be sustainable, when the general bond issuance interest rates are at least 4-5% or even higher? It's clear that local governments are compelled to incur new debts to repay existing ones, which is unsustainable.

Our second research question is: Why do local governments borrow so much money? What are the fundamental and systemic reasons? We believe the most fundamental reason is is the prioritization of GDP growth by local governments, with a particular emphasis on short-term GDP gains.

Building on this theory, we developed a basic two-period game model to analyze governmental borrowing behaviors across two distinct phases. When GDP trumps all and short-termism prevails, the government is willing to incur excessive debt in the first period without adequately weighing its repayment capacity in the subsequent period, nor its ability to secure further borrowing. This is a simple theoretical model.

Our third question is: does high local government debt affect local development? For this, we amassed an extensive dataset, including economic development data for each province and calculated the scale of local debt for each province. Through various empirical analyses, we discovered that places with high local debt, or more precisely, places with high local debt in the proceeding years, experienced slower economic growth in the following years. Their investment in manufacturing and infrastructure also grew more slowly, and their total factor productivity growth rate declined, leading to an overall slowdown in economic growth.

In summary, if a government incurs high debt in the initial stages, various economic indicators will decline in the later stages. In other words, based on our findings, we conclude that local governments have excessively borrowed.

Our paper mainly presents three novel points of interest:

First, we have developed a new method for estimating local government debt, focusing on unraveling the nesting issues of debts held by local SOEs.

Second, we provide a theoretical explanation for why local governments accumulate so much debt.

Third, we use our data to discuss the consequences of excessive borrowing by local governments.

This study is based on the theoretical framework of government and market economics, which considers the government as a key player in the market economy, and hence it's essential to pay attention to government actions.

Next, I will introduce our research findings in detail. At the end of this lecture, I will also discuss some policy recommendations for resolving local government debt from our research institute and welcome your valuable opinions and questions.

Post-publication editing note:

Part II: David Daokui Li's meticulous breakdown of "nested" dimensions of local govt & its debt

In a post on Friday, Dec. 22, we shared that Professor David Daokui Li of Tsinghua University recently unveiled a study - together with Zhang He at the Academic Center for Chinese Economic Practice and Thinking (ACCEPT) - that found China’s local government debt in 2020 was around 90 trillion yuan, 50% higher than

Part III of David Daokui Li: local government debt in China driven by central's GDP requirement and prevalent short-term focus

Hi, this is Jia Yuxuan from Beijing, coming to the third and final part of Prof. David Daokui Li's lecture on the scale and dimensions of China's local government debt. In the first part of the study by Prof. Li and Zhang He, it was reveiled that China’s local government debt in 2020 was around 90 trillion yuan, 50% higher than

The East is Read’s extensive coverage of Chinese scholars’ discussion of China’s local government debt also includes:

Zhang Ming says local govt handicapped by short-term, high-interest debt, & unaffordable responsibilities

Local government debts in China—their causes and solutions—have been a subject of internal debate for months, and has frequently been featured on The East is Read. In a recently published piece, Ting Lu, Chief Economist of Nomura Securities China, identified revitalization of the real estate sector as a key measure to kickstart debt resolution in China.

Ting Lu: urbanization+real estate is key to debt resolution

This article features the speech of Mr. Ting Lu, Chief Economist of Nomura Securities China, from his recent discussion in the New Economist Think Tank Debt Debate (Part Two). The original Chinese version is available on the WeChat blog of New Economist Think Tank.

Xu Gao: China's historical, unitary framework implies central govt responsibility for local govt debt

The unitary political framework, a millennia-old legacy in China, obligates the central government to intervene in local government debt, which is a key component of the country's growth model, said Xu Gao, the Chief Economist of Bank of China International (China).

Beyond LGFVs: three types of hidden debt unaccounted for in China's official stats

The debts accumulated by Local Government Financing Vehicles (LGFVs), often referred to as China's hidden debts due to their association with government liability, are widely known among observers of China's economy. However, in a recent speech and Q&A

Luo Zhiheng on government debts, fiscal expenditure, and major risks

Luo Zhiheng 罗志恒 is the Chief Economist and President of the Research Institute at Yuekai Securities and one of China’s leading scholars on macroeconomics and fiscal policies. He sat at Li Qiang, Chinese Premier’s roundtable on Jul. 6. Although what he said was not disclosed, the following

| A guest post by

|

I wonder why the WB and IMF estimate was much lower. That’s not really explained in the article.

A very interesting article, I'm pleased to see this sort of study can be undertaken and published.

Besides debt which is relatively easy to find and measure, being related to currency of exchange, I'm always currious about deeper and more dangerous liabilities, those that can't be easily discovered and measured. For example polluted/toxic soils, these are naturally not transparent and often go unmeasured/undermeasured in the West, and I wonder how they are grappled with under a socialist system where in theory they are more likely a public liability than a private one.