China’s Changing Role in Multilateral Development Banks

Bert Hofman and P. S. Srinivas in CCG's new book discuss how China reshapes global financial governance to the interests of itself and developing countries.

At the CCG book launch of Enhancing Global Governance in a Fragmented World—Prospects, Issues and the Role of China, published by Springer Nature, on August 22, P.S. Srinivas described his joint contribution with Bert Hofman to the book in a prerecorded speech. He said, "We chose to focus our contribution on China's changing role in multilateral development banks, a contribution that we hope covers the issues of multilateralism, global economic and financial governance, China's evolving role in them, and the prospects for the future from an economic perspective…China has succeeded in helping define governance of these institutions in a way that it feels is more reflective of its own views and the needs of developing countries."

Bert Hofman is Adjunct Professor at the East Asian Institute (EAI) at National University of Singapore (NUS). He was Director of EAI and Professor of Practice at the Lee Kuan Yew School of Public Policy from June 2019 to December 2023. Before joining NUS in 2019, he worked with the World Bank for 27 years, 22 of which were in Asia, and 12 of which were in China. He was World Bank Country Director for China 2014–2019, Country Economist 2004–2008, and Chief Economist for the World Bank in the East Asia and Pacific region 2011–2014. Follow Bert's Newsletter.

Dr. P. S. Srinivas joined the East Asian Institute (EAI) at the National University of Singapore (NUS) in April 2021 and is currently Visiting Research Professor working on Chinese financial markets and China’s evolving role in the global financial architecture. Prior to EAI, he worked with the New Development Bank in Shanghai (2016–2021) as Director General of the Front Office of the President. He has also worked at the World Bank in Washington DC (1996–2016); the Asian Development Bank in Manila, Philippines (1993–1996); and ICICI in Mumbai, India (1987–88).

Their contributed chapter to the book is presented as follows. Both the Chapter and the whole book, edited by Henry Huiyao Wang and Mabel Lu Miao, are open for free download on Springer's website.

China’s Changing Role in Multilateral Development Banks

Bert Hofman and P. S. Srinivas

Abstract

China has a complex relationship with MDBs as it is simultaneously one of their largest shareholders, one of their largest donors, one of their largest borrowers, and one of their largest recipients of contracts. Through the Belt and Road Initiative (BRI) and other lending, China has also become the world’s largest bilateral lender to developing countries. It is also a major driver behind the AIIB and NDB, both of which have the potential to make a significant impact on the international financial system and provide lessons for established MDBs in their own operations and governance.

Keywords

Development finance · Multilateral Development Banks (MDBs) · Asian Infrastructure Development Bank (AIIB) · New Development Bank (NDB) · BRICS · Internationalization of the RMB

Since China joined the World Bank (WB) in 1980,1 its role in multilateral development banks (MDBs) has changed considerably. China now has a complex and multifaceted relationship with such institutions. It is, at the same time, one of the largest shareholders, one of the largest donors, one of the largest borrowers, and one of the largest recipients of contracts in projects financed by several of these institutions.

In addition to its growing role in established MDBs, China has led the setting up of two new MDBs, the Asian Infrastructure Investment Bank (AIIB) and the New Development Bank (NDB). One of the driving forces behind the creation of these institutions has been China’s frustration with the slow pace of change in the existing MDBs, particularly as it relates to China’s shareholding. In addition, these new MDBs can be viewed as experiments, where new approaches to global development finance are being tried out and, depending on the results, could have implications for more established institutions.

MDBs are being increasingly called upon to scale up assistance to developing countries to help them address emerging challenges such as climate change, post-COVID-19 response, and food security in addition to long-standing demands of infrastructure and sustainable development. China’s expanding role in these institutions puts it in a better position to influence their activities.

China’s role in global development finance through its own bilateral creditor relationships with developing countries has been the focus of several studies.2 Through the Belt and Road Initiative (BRI) and other lending, China has now become the world’s largest bilateral lender to developing countries. China’s role in MDBs, however, has only recently begun to attract attention.3 This paper reviews existing work in this area and contributes to the literature by examining in greater detail China’s role in one of the new institutions that it has had a major role in creating, the NDB.

The Evolution of China’s Multiple Roles in MDBs

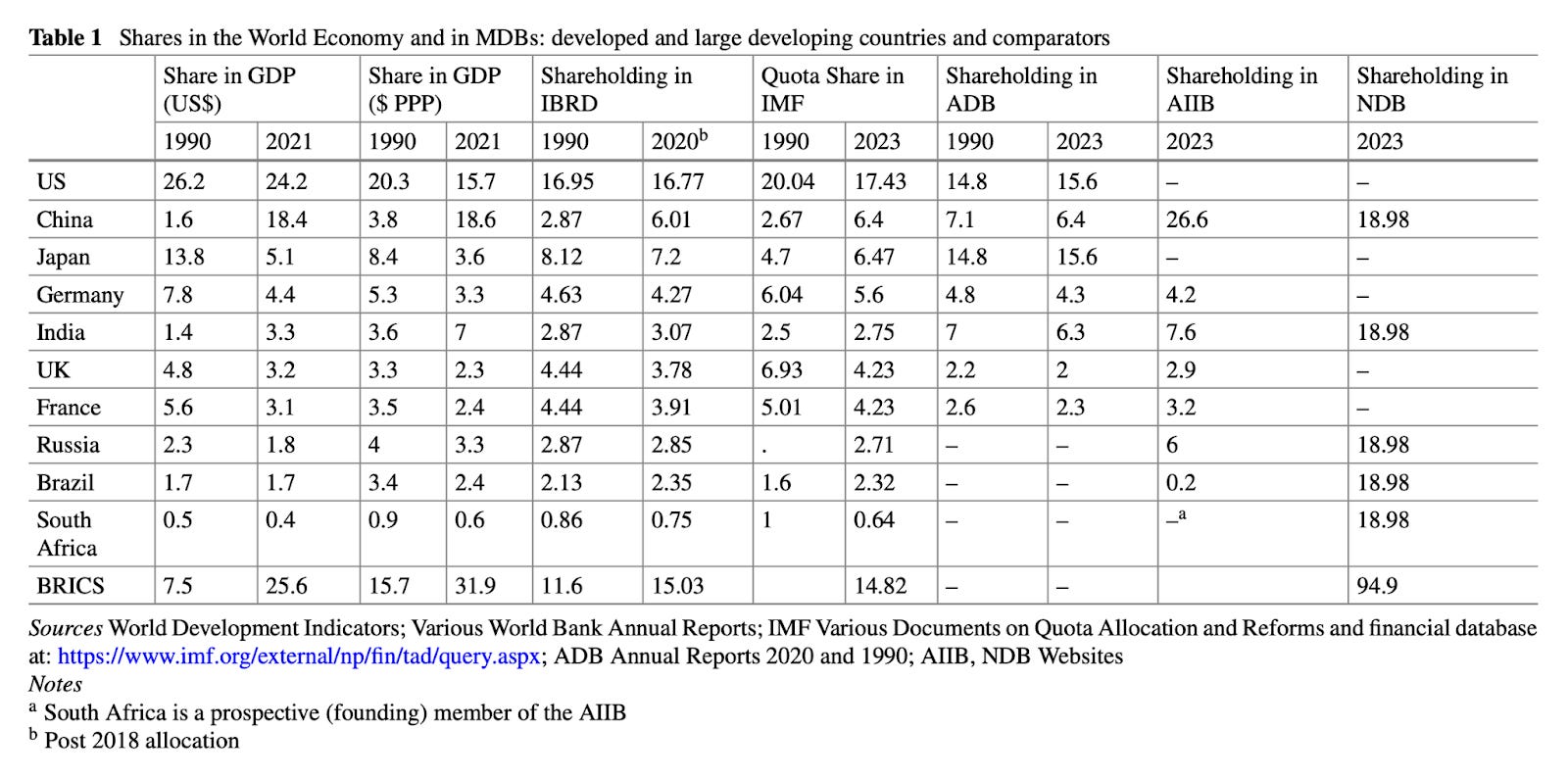

China’s role as a shareholder in MDBs has grown considerably since it joined the system in 1980 (Table 1). Morris et al. (2021)4 map China’s participation in multilateral financial institutions and find that China is a member of 17 global and regional multilateral financial institutions in addition to the International Monetary Fund (IMF). Across the MDB system, China now stands second in terms of voting power (just below 8 percent), considerably behind the United States (US, about 14%), ahead of Japan (around 7%), and well ahead of other G-7 countries. China’s role in the IMF has also grown substantially. In terms of the IMF’s quota or share capital, in 2010 China had the sixth largest quota share. It now has the third largest share ($43.4 billion in 2021) behind the US and Japan. However, comparing China’s share in the capital of the MDBs to its share of global Gross Domestic Product (GDP), it is still considerably under-represented (Table 1).

China’s role as a donor and financing partner to MDBs has also grown substantially.5 China now acts as a major donor to MDB concessional funding windows managed by MDBs. It is the 5th largest donor to the Asian Development Fund (ADF) managed by the Asian Development Bank (ADB), the 6th largest in the International Development Association (IDA) managed by the WB, and the 12th largest donor of the African Development Fund (AfDF) managed by the African Development Bank (AfDB). It has also contributed to special-purpose funds or trust funds managed by several MDBs, including the $2 billion Africa Growing Together Trust Fund managed by the AfDB. China has entered into Memoranda of Understanding (MoUs) and co-financing agreements with institutions such as the International Finance Corporation (IFC) and the AfDB, wherein Chinese institutions co-invest their own funds, alongside those of the MDBs, in projects identified by the MDBs.

China has also long been a major borrower from MDBs such as the WB and the ADB. For much of its time as a member, it was one of the top five borrowers from these institutions, although more recently its borrowings have declined. China also borrows from the NDB and AIIB. In recent years, pressures on China to borrow less and to prepare for “graduation” have been increasing. China’s increasing per capita income has played an important role in the decisions by the WB and ADB to reduce the lending to China. As part of its 2018 capital increase, WB shareholders requested enforcement of a long-standing graduation policy for countries above the so-called graduation discussion threshold of income.6 Graduation from the WB is not an automatic consequence of reaching a particular income level, but rather is supposed to be based on a determination of whether the country has reached a level of institutional development and capital-market access that enables it to sustain its own development process without recourse to WB funding. The ADB has similar criteria for graduation.7 Also as part of the 2018 capital increase, WB management committed to focusing lending to China on global public goods and on aspects of socio-economic management in which China has demonstrated remaining weaknesses. Consequently, lending rapidly declined from a record $2.5 billion in FY2017 to less than $1 billion annually at present.

Chinese enterprises have been major players in procuring contracts for implementation of projects financed by MDBs—both within and outside China. During 2010–2020, firms from China won the most contracts by value of those awarded for projects financed by the World Bank in all years except one.8 Around 20 percent by value of all contracts awarded by the World Bank were won by Chinese firms. Nearly half of all contracts awarded by the World Bank to Chinese firms were for work outside China. India and Brazil, whose firms also win large amounts of World Bank contracts by value, on the other hand, win most of their contracts for work done domestically. Italy and Spain round out the top five countries whose firms win large amounts of World Bank awarded contracts. Chinese firms are also at or near the top of the rankings in terms of contracts obtained from several other MDBs.

The Drivers of China’s Evolving Role in MDBs

In line with its rapidly growing economic clout, China has been seeking a greater voice in the international financial architecture. That architecture was largely formed after World War II and comprised of institutions such as the IMF and WB, which means that Western developed countries control the majority of voting shares in global financial institutions and have a greater voice in terms of the way the institutions are run.

In the aftermath of the global financial crisis, which means that at the London G20 summit in 2009, member countries had agreed to reforms in governance of international financial institutions to provide greater voice to developing countries, in response to China’s (and other large developing countries’) calls for a more representative international financial architecture reflecting the significantly larger role of developing countries.9 However, changes were slow to be implemented in practice. Shareholding being a zero-sum game, a greater role for China (and other large developing countries) meant a smaller role for existing large (and mostly developed country) shareholders. And these latter shareholders have been reluctant to significantly reduce their shareholding. Therefore, while China’s share in these institutions has increased over time, it still does not reflect its overall weight in the global economy, where it is already the largest economy on a Purchasing Power Parity (PPP) basis and the second largest in nominal terms (Table 1).

China’s share in the International Bank for Reconstruction and Development (IBRD, the WB’s non-concessional lending arm) also falls well short of the “formula-based” notional allocation of 12%. At the Lima, Peru Annual Meetings in 2015, it was decided to base shareholdings on a formula that takes share in the world economy and past cumulative contributions to IDA as weights to determine what a country’s share should be. For China, this works out to 12% based on 2020 data, but its actual shareholding is 6%.10

China has responded to its limited success in gaining a greater shareholding in established MDBs in a variety of ways. One was by increasing its contributions to IDA, the WB’s soft loan window, which is financed through a trust fund that requires regular replenishment. China’s contribution went up from $200 million in IDA 16 (2008) to $1.3 billion in IDA 20 (2021), or 5.6% of total.11 This contribution not only provides China with voting rights in IDA itself, but also contributes to future shareholding in the IBRD, which takes IDA contributions into account.

China also created a series of funds, managed by MDBs, through which it could finance projects in developing countries.12 This approach lacked one of the main benefits of contributing to an MDB, which is that of leveraging China’s resources through market borrowings using the high credit ratings of MDBs. It did, however, provide a way for China to gain some influence on the governance of existing MDBs.13 China also became a member of or a financier to several smaller MDBs in Africa, Central Asia, and Latin America. Its financial commitments to these institutions are small, but they augment China’s overall engagement in the development process of countries in these regions.14

China’s other strategy has been to lead the establishment of two new MDBs: the Asian Infrastructure Investment Bank (AIIB) and the New Development Bank (NDB), where it has been able to help define institutional governance in a way that it feels is more reflective of its views of the needs of developing countries. The establishment of these two MDBs also demonstrates China’s commitment to a multilateral approach to global development.

The formation of the AIIB was announced by President Xi Jinping in 2013. With 106 member countries as of April 2023, including five of seven G-7 member countries, the AIIB is now the second largest MDB in the world, after the World Bank Group, in terms of membership. China is the largest shareholder with 26.6% of the shareholding.15 The AIIB exhibits several similarities to existing MDBs such as the WB, with a mix of developed and developing member countries, although with China in the lead instead of the US and Japan as in the case of the WB and the ADB, respectively. Like several established MDBs, it also has the highest AAA credit rating. Some of AIIB’s policies, such as its environmental and social authority delegated to the President as compared to established MDBs, and a greater share of private sector projects.16

The New Development Bank

The establishment of the NDB was one of the outcomes of the political and economic dissatisfaction arising out of the growing disparity between the BRICS countries’ (Brazil, Russia, India, China, and South Africa)17 share of the world economy and their representation in the institutions underpinning the global financial architecture. The heads of state of Brazil, Russia, India and China had begun meeting annually in the aftermath of the global financial crisis, to discuss issues of common interest, with the first meeting in Ekaterinburg, Russia in 2009. From the very beginning, leaders of these countries expressed their dissatisfaction with the prevailing global financial architecture and called for reforms to institutions such as the IMF and the WB and called for a world economic order that better reflected the changed global economy.18 They called for a greater voice, reflected in increased share of voting rights in existing institutions, more transparent processes for selection of the heads of these institutions and increased reflection of the development needs of these countries in the operations of existing institutions.

Despite the 2009 G20 agreement, adjustments in shareholding and governance reforms remained insufficient in the eyes of BRICS leaders. Calls for reform of the global financial architecture remained a consistent feature of several subsequent BRICS summits. At the fourth BRICS Summit in New Delhi in 2012, the idea of the New Development Bank (NDB) was first formally articulated.19 On 7 July 2015, justpolicies, are broadly similar to those of established MDBs. However, it also has differences such as a non-resident Board of Directors (BoD), substantially more project approval prior to the seventh BRICS Summit, the NDB was established with Brazil, Russia, China and South Africa as Founding Members.20

BRICS comprise 42% of the global population and have, as a block, been among the fastest growing developing countries in recent decades. The BRICS’ share of world Gross Domestic Product (GDP) measured in Purchasing Power Parity (PPP) terms rose from about 18% in 2000 to about 32% by 2021, a share more than double that of countries of the European Union (EU, 15%). However, the combined voting share of these countries in the WB, for example, stood at just 15% in 2020.

In addition to the issue of representation, the urgent economic development needs of BRICS countries played a major role in the drive to establish the NDB. Existing MDBs, especially the WB, had considerably reduced the share of their lending to infrastructure development in favor of social sector development and budget support, despite continuing high demand for infrastructure finance from BRICS and other developing countries.

At the time of NDB’s establishment, China was simultaneously in the process of establishing the AIIB. The models of AIIB and the NDB are, however, fundamentally different. The AIIB’s governance structure is broadly similar to the prevailing Western institutions, with China being the largest shareholder. In the NDB, China is an equal partner with the other BRICS countries, with each having equal voting shares in the institution. At its founding, each member had a 20% share of the NDB’s capital and even with new members joining, the five founders will always hold no less than 55% of the institution’s voting rights.21 The NDB structure of shareholding gives an equal voice to all five founders in the institution, despite substantial differences in their economic size.22 The structure also limits the total shareholding of non-borrowing members to a maximum of 20 percent of total capital and that of any single non-founding member to a maximum of 7 percent. The NDB has an authorized capital of $100 billion and a subscribed capital of $50 billion, of which $10 billion is paid-in and $40 billion is callable.

In the NDB, China is part of an experiment of a new model of governance of global financial institutions. The NDB’s Articles of Agreement ensure that no single founding member has veto rights as they require most decisions to be made by simple majority of the founding members. Another important difference is that the Presidency of the NDB is rotated among the five founding members in the BRICS order.23 This model is in response to the dissatisfaction of BRICS (and other developing) countries with the appointment process of the chief executives of existing global financial institutions. These roles are by tradition reserved for a US citizen (the WB), a European citizen (the IMF), and a Japanese citizen (the ADB).

China has supported a totally different approach to membership expansion in the NDB as compared to the approach taken by AIIB.24 While the latter emphasized new membership at speed and already has 106 members, the former has taken a much slower approach. While the NDB’s membership is open to all members of the United Nations, it was only in 2021 that it welcomed its first non-founding members. As of April 2023, three new members (Bangladesh, the United Arab Emirates, and Egypt) had joined the NDB and Uruguay has been identified as a “prospective” member.25 The NDB expects its membership to grow consistently and in a gradual way in the future and that “…its approach to membership expansion will strive for greater diversity of member countries—both in terms of geography and stage of development. Continued membership expansion will enable the NDB to promote infrastructure and sustainable development in a larger number of countries, creating an impact beyond its existing members. New members will also strengthen the [NDB’s] capital base, support portfolio diversification, enhance its capacity to mobilise resources, enrich its development experience and bolster the NDB’s role as a platform for wider collaboration among [emerging markets and developing countries].”26

China and the other BRICS countries have supported this process stating that they “….look forward to further membership expansion in a gradual and balanced manner in terms of geographic representation and comprising of both developed and developing countries, to enhance the NDB’s international influence as well as the representation and voice of EMDCs in global governance.”27 The addition of the three new members has reduced the shareholding of the five founding members to 18.98% each.

China has also supported several innovations in the operational model of the NDB, which are different from those of established MDBs. These changes are targeted at addressing some of the criticisms of existing institutions, such as the WB, particularly their bureaucratic and slow operational approaches in which project approvals can sometimes take years. The NDB claims that speed of approval is a key element of its operational model with its stated target of approving loans within six months, while not compromising on quality.28 The NDB also uses country systems to manage the environmental and social aspects of, as well as procurement procedures related to, the projects it finances, thereby removing the need for its borrowers to deal with an external institution’s systems. Arguably, because the NDB has, thus far, dealt mostly with a limited clientele of just five middle-income country borrowers, this is more achievable for the NDB than for global institutions such as the WB that deal with many more countries at widely different stages of development. It remains to be seen how the NDB’s approach evolves as its membership expands to include countries less developed than the BRICS.

The NDB also contributes to China’s ambitions to internationalize its currency, the Renminbi (RMB). Since the early 2000s, China has had ambitions to internationalize the RMB and has gradually made a series of policy efforts to achieve this goal.29 The NDB had raised RMB 28 billion (about $4 billion) from Chinese capital markets as of December 31, 2022, in addition to $7.8 billion from global capital markets.

The NDB has also provided local currency loans to its borrowers and made provision of such loans an important element of its operational strategy.30 This has been a long-standing demand of many borrowers from MDBs, and one that MDBs such as the WB are technically able to do, but also one that has made little progress. Local currency loans reduce the foreign exchange risk that borrowers face if their currencies decline in value relative to that of currencies such as the US Dollar or Euro, which are typically the currencies that most other MDBs provide their loans in. As of December 31, 2021, the latest published figures, 23% of NDB’s total lending portfolio of $30 billion was in local currencies.31 The NDB has thus far provided local currency financing to China, India, and South Africa at competitive interest rates, though, like other MDBs, offering rates better than the sovereign in local currency is also a challenge for the NDB.

The NDB has ensured that the pricing of its loans remains competitive with that of more established MDBs. Given that the NDB is currently rated AA+ while most other established MDBs are rated AAA, the cost at which the NDB raises funds in the markets is higher. Essentially, this implies that the NDB needs to manage itself more efficiently to keep its operating costs low to make up for the cost differential.32 A lean management and staff structure is, therefore, also a key feature of the NDB’s operational model. Such a setup also implies that the NDB is less ambitious than some other MDBs in terms of economic analysis and provision of global public goods, which other MDBs often support. Unlike other MDBs, the NDB has also chosen to avoid pushing for and supporting structural reform in its member countries, and thereby focuses less on analytical work supporting such reforms. Even for some BRICS countries, one of the motivations for borrowing from other MDBs is their support for structural reforms.

With its location in Shanghai and having been established nearly at the same time as the China-led AIIB, the NDB could have become yet another China-led institution.

Despite orders of magnitude of differences in economic size among the five founders, with China dominating by a large margin, the lack of veto authority for any country has not yet proved to be a significant hurdle.33 China has calibrated its role to ensure that, at least thus far, all founding shareholders have an equal voice in the institution. The founders have worked together to enable the NDB to test out new approaches and new ways of doing business that could be useful for other, more established, MDBs to consider.

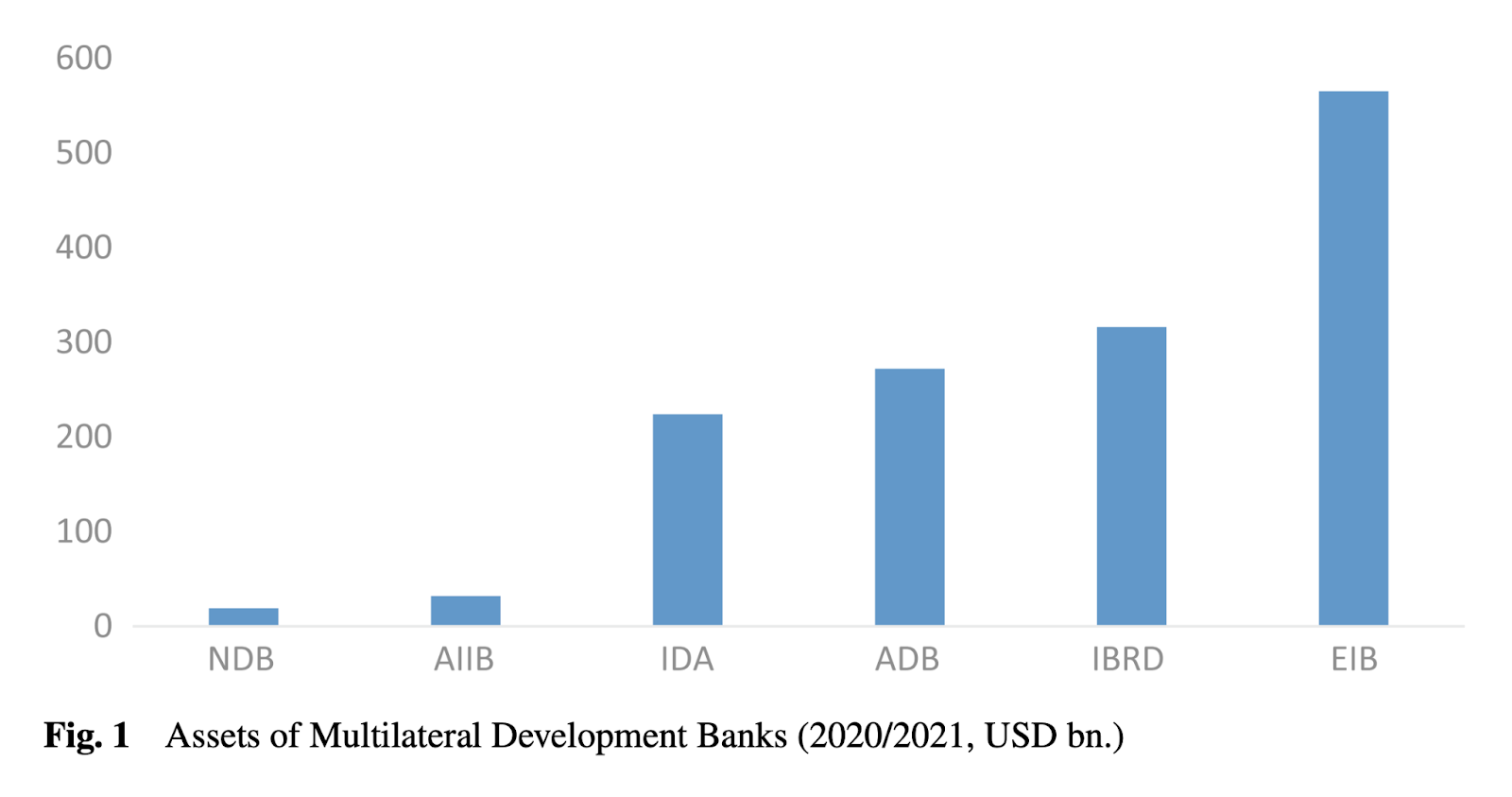

China will also have a large role play in helping the NDB address its most critical challenge of scaling up. Scale will have to be achieved rapidly, even as the institution continues to build upon the foundation that has been laid, ramps up its human resources, and further strengthens its internal systems. It needs to become a large enough player among the community of MDBs (Fig. 1) to make a material difference to the global financial architecture. There have been significant changes in the political and economic situations in BRICS countries and in the global economy since the establishment of the NDB. The continuing political and economic tensions between the US and China, the Russian invasion of Ukraine, political tensions between China and India due to border conflicts, the continuing weak economic performance of Brazil and South Africa are all likely to impact the NDB’s ability to scale up, directly or indirectly. Being based in Shanghai, China’s ability to help the NDB navigate these issues will be critical to its future evolution.

Conclusions

China’s evolving role in established MDBs demonstrates its belief in the importance of these institutions in global development. Even as it expresses frustration at the slow progress of changes in governance and operational models at these institutions, it continues constructive engagements within them. It continues to attach importance to its borrowing and, equally importantly, learning from these institutions, particularly the WB, both for its own economic development and for its broader engagements with other developing countries. China has also shown that it is willing to make long-term investments in established MDBs through its more recent roles as a major financier, partner, and donor. It would be reasonable to expect that China’s voice and role in the governance of these institutions, and through them in the global financial architecture, will continue to grow in line with its continued economic growth.

China has also shown that it is willing to experiment with new models of MDB governance and operations through its roles in the AIIB and NDB. These two institutions, established almost simultaneously in China with a major Chinese presence, have very different models of governance and operations. In the AIIB, an institution that closely resembles established MDBs in several aspects including global membership, China is the dominant shareholder. In the NDB, China has taken a role on par with the other BRICS countries, even though its economy is five times larger than that of the next biggest member, India. It is borrowing from both institutions. It is also supporting new operational approaches in both institutions. The results of the working of these institutions could have lessons for established institutions.

The NDB is an innovative experiment in global financial governance. If the institution navigates well the current challenges it faces, scales up significantly, and can demonstrate that its projects have been successfully implemented and are achieving their intended objectives, it clearly has the potential to make a significant impact on the international financial system. China’s gradually increasing voice in established MDBs could then help in pressuring these institutions to take lessons from NDB into account in their own operations and governance.

Technically, the People’s Republic assumed the seat for China. The People’s Republic of China had been one of the founding members of the World Bank in 1944.

Brautigam, Deborah (2009). The dragon’s gift: the real story of China in Africa. Oxford University Press.

Brautigam, Deborah (2011). “Aid with Chinese characteristics”: Chinese foreign aid and development finance to meet the OECD-DAC aid regime, Journal of International Development 23(5), pp: 752–764.

Calabrese, Linda and Y. Chen (2020). Broadening the Belt and Road: China’s new fund for multilateral cooperation. https://odi.org/en/insights/broadening-the-belt-and-road-chinas-new-fund-formultilateral-cooperation/, accessed on April 15, 2023.

Chen, Gregory T. and K. P. Gallagher (2019). “Coordinated credit spaces: the globalization of Chinese development finance,” Development and Change, 50(1), pp. 245–274.

Horn, Sebastian, C. Trebesch, and C. M. Reinhart (2019). China’s Overseas Lending. Kiel Working papers No. 2132, Kiel Institute for the World Economy.

Horn, Sebastian, B. C. Parks, C. M. Reinhart, and C. Trebesch (2023). China as an International Lender of Last Resort. AIDATA Working Paper 124, March 2023.

Gasemyr, Hans J. (2018). China and Multilateral Development Banks: Positions, Motivations, Ambitions. NUPI Report, The Norwegian Institute of International Affairs.

Morris, Scott, R. Rockafellow, and S. Rose (2021). Mapping China’s Multilateralism: A Data Survey of China’s Participation in Multilateral Development Institutions and Funds. CGD Policy Paper 241, November 2021. Center for Global Development.

Humphrey, Chris and Y. Chen (2021). China in multilateral development banks: Evolving strategies of a new power. September 2021, ODI Report.

Ibid.

Ibid.

OECD, Transition Finance Toolkit, https://www.oecd.org/dac/transition-finance-toolkit/IBRDgraduation-2021.pdf, accessed 13-4-2023.

Asian Development Bank, Classification and Graduation of Developing Member Countries. https://www.adb.org/sites/default/files/institutional-document/31483/om-a1.pdf, accessed 13- 4-2023.

Ibid.

https://www.imf.org/external/np/sec/pr/2009/pdf/g20_040209.pdf, accessed 15 April 2023.

See: World Bank, 2020, 2020 shareholdings review: report to governors at the annual meetings. https://www.devcommittee.org/sites/dc/files/download/Documents/2020-09/Final%20D C2020-0009%20Shareholding.pdf, accessed 20-4-2023.

IDA, Contributor Countries, https://ida.worldbank.org/en/about/contributor-countries, accessed 13-4-2023

Ibid.

Ibid.

Ibid.

http://www.aiib.org/en/about-aiib/governance/members-of-bank/index.html, accessed on April 13, 2023.

Mike Callaghan & P. Hubbard (2016) The Asian Infrastructure Investment Bank: Multilateralism on the Silk Road, China Economic Journal, 9:2, 116–139, DOI: https://doi.org/10.1080/17538963. 2016.1162970.

Asian Infrastructure Investment Bank (2015). “Asian Infrastructure Investment Bank: Articles of Agreement,” Beijing. https://www.aiib.org/en/about-aiib/basic-documents/articles-of-agr eement/index.html, accessed on April 18, 2023.

Alex He (2016). China in the International Financial System: A Study of the NDB and the AIIB, CIGI Paper No. 106, accessed on April 18, 2023.

Chris Humphrey (2020). “From Drawing Board to Reality: The First Four Years of Operations at the Asian Infrastructure Investment Bank and the New Development Bank,” Working Paper, Boston University Global Development Center.

Goldman Sachs (2001) coined the term BRICs to refer Brazil, Russia, India and China. https://www.goldmansachs.com/insights/archive/archive-pdfs/build-better-brics.pdf, accessed 22 April 2022. South Africa joined the grouping in 2010 and the acronym changed to BRICS.

Joint Statement of the BRIC Countries’ Leaders. http://www.kremlin.ru/eng/text/docs/2009/06/ 217963.shtml, accessed April 15, 2023.

https://mea.gov.in/bilateral-documents.htm?dtl%2F19158%2FFourth+BRICS+Summit++ Delhi+Declaration, accessed April 15, 2023.

http://www.brics.utoronto.ca/docs/150709-ufa-declaration_en.html, accessed April 15, 2023.

http://www.ndb.int/wp-content/uploads/2022/11/Agreement-on-the-New-Development-Bank. pdf, accessed on April 14, 2023, Article 6 (b).

For e.g.: In current US dollars in 2020, China’s GDP was US$14.7 trillion while that of South Africa was US$330 billion, although both have the same share in the NDB.

The founding President was an Indian national. Brazil nominated the second President. Russia, China, and South Africa will follow, after which the President will rotate in the BRICS order. Each country’s Presidency is for a five-year term.

http://www.ndb.int/wp-content/uploads/2022/11/Terms-Condition-and-Procedures1.pdf, accessed on April 18, 2023.

https://www.ndb.int/wp-content/uploads/2023/04/Investor-Presentation-April_20230406.pdf, accessed on April 18, 2023.

Ibid.

Ibid.

https://www.ndb.int/wp-content/uploads/2023/04/Investor-Presentation-April_20230406.pdf, accessed on April 18, 2023.

Among others, see P. S. Srinivas and R. Cheng (2021). “Renminbi Internationalisation (I): A Historical Review and China’s Policy Measures,” EAI Background Brief No. 1597, July 2021.

P. S. Srinivas and R. Cheng (2021). “Renminbi Internationalisation (II): Progress and Prospects,” EAI Background Brief No. 1598, July 2021.

https://www.ndb.int/wp-content/uploads/2022/07/NDB_StrategyDocument_Eversion-1.pdf.

https://www.ndb.int/wp-content/uploads/2022/10/NDB_AR_2021_complete.pdf, accessed on April 12, 2023.

There are relatively fewer degrees of freedom available to the NDB on other aspects that could potentially be used to manage this issue such as duration of lending, reserve policies, and liquidity buffers. These are largely the same for the NDB as those of established AAA rated MDBs, given client demands, and rating methodologies.