Xu Gao: why SOE stocks should be distributed among all citizens

Chief Economist of Bank of China International says it is the key to consumption-based growth

Xu Gao is the Chief Economist of Bank of China International (China) Co., Ltd., an adjunct professor of National School of Development in Peking University, and a member of the China Chief Economist Forum. Xu has also published two best selling textbooks in China -- "Lectures on Macroeconomics from a Chinese Perspective" and "Lectures on Financial Economics".

The following is an extract from Xu’s article, "The shift to consumption-based growth needs a 'Universal Shareholding Scheme for SOE Stocks'", Xu recommends creating multiple state-owned investment funds, transferring state enterprise equity into them, and distributing the fund shares evenly among all citizens. It is a notion, according to Xu, that was construed over a decade ago, since when he became more and more convinced of its feasibility.

I wrote in my June 28 article, "We Need to Correct Misconceptions about China's Debt", that:

"The fact that Chinese companies yield little dividends to residents is an indication of dysfunction in China's market mechanisms for regulating consumption and investment...and as the wealth effect of China's corporate sector on the household sector is practically negligible, when investment returns decline, incomes for the corporate sector (especially SOEs and private firms tightly controlled by major shareholders) do not automatically flow to residents. This means China's problems of excess savings and excess investment cannot be automatically corrected by the market. This is the crux of why China has long suffered from insufficient consumption and excess savings, and an important difference from Western countries."

The disconnect between China's household sector and corporate sector stems from various factors, but the huge presence of SOEs is an undoubtedly a predominant one. Although China's massive state capital belongs to all citizens, very little of the returns on state capital are transferred to households.

Data disclosed by the State Asset Management Department of the Ministry of Finance shows that in 2021, the total amount of state assets in financial and non-financial enterprises was 308.3 trillion yuan [42.89 trillion U.S. dollars] and 352.4 trillion yuan [49.03 trillion U.S. dollars] respectively. If we deduct the liabilities, the figures would be 86.9 trillion yuan [12.09 trillion U.S. dollars] and 25.3 trillion yuan [3.52 trillion U.S. dollars] respectively. Together, the total amount of state assets (net capital) belonging to SOEs in China in 2021 was 112.2 trillion yuan [15.61 trillion U.S. dollars] . In addition, China also had 42.9 trillion yuan [5.97 trillion U.S. dollars] of net assets under administrative control, not to mention state-owned natural resources (such as land).

According to data disclosed by the Budget Department of the Ministry of Finance, in 2021, China's fiscal revenue obtained 517.043 billion yuan [71.93 billion U.S. dollars] from SOE profits, dividends, asset sales and other items. Nearly half of that amount was eventually returned to SOEs by means of capital injections and subsidies, etc. Only 247.284 billion yuan [34.40 billion U.S. dollars] was transferred from the state enterprise capital operation budget into the national treasury.

It goes without saying that SOEs play an important role in China's economy, paying salaries and taxes like all companies do. But as enterprises owned by all citizens, SOEs should provide returns to the public beyond salaries and taxes, i.e., through capital returns. However, calculations using the above Ministry of Finance data show that in terms of net returns obtained by fiscal revenue, China's SOEs provided a capital return rate of only 0.22% on their 2021 state assets of 11.22 trillion yuan [1.56 trillion U.S. dollars] . In addition, although SOEs also directly distribute dividends to resident shareholders, the amounts are fairly limited.

As such, whether through direct dividend distribution to residents or indirect transfer through fiscal revenue, there have been few capital returns generated by China's massive state capital. This results in a very weak wealth effect connection between China's households and SOEs.

Of course, the disconnect between China's household and corporate sectors does not all stem from SOEs. Capital returns transferred to the general public from private firms with highly concentrated ownership are also very limited. The low income transfers from the corporate sector to the household sector is in truth a reflection of households' lack of restraint on corporations, which renders the market mechanism ineffective for regulating consumption and investment in China. This also explains China's high savings and investment rates, despite the country's excessive investment which clearly depressed capital returns.

The ratio of GDP to capital stock can demonstrate, indirectly, trends in economy-wide capital returns (theoretically, the two figures should be positively correlated). After the global financial crisis in 2008, China's GDP-stock capital ratio has sharply declined and is now at the lowest level since reform and opening-up. This suggests a marked decrease in China's capital returns, which should have made savings and investment much less attractive than pre-crisis. If market mechanisms for regulating consumption and savings were working, we should have seen more income allocated to consumption rather than savings, causing the savings rate to decline. And yet it's quite the contrary - after the financial crisis in 2008, China's savings rate did not decline due to the fall in investment returns; Rather, it remained stable and high above pre-crisis levels. The persistently high savings rate is further evidence of insufficient consumption in China.

Should we presume that the ultimate goal of economic growth is to improve people's welfare, then it is obvious how the national income shall be used to improve people's welfare - namely, by letting the people make the decisions. It is especially the case when it comes to how income should be allocated between consumption and investment (or consumption and savings) so as to ensure that the ratio between consumption and investment is at the most appropriate level - that is, the level that maximizes people's welfare. However, in China, there is an obvious disconnect between the household sector and the enterprise sector.

This disconnect is manifested on the macro level in that national income has not adequately flowed to the household sector, leading to the household income accounting for a relatively low percentage of GDP. The result is insufficient household consumption, as a considerable portion of the national income is not under the household's discretion.

On the micro level, this disconnect is reflected in that corporate investment decisions are less constrained by household preferences, thus leading to over-investment. Therefore, judging by whether economic development is most conducive to improving people's welfare, there is indeed a problem of insufficient consumption in China.

To facilitate consumption-based growth and increase the proportion of consumption in the economy, we sure need to increase the proportion of household income. But that is not enough. More importantly, we need to build a market-based mechanism to dynamically adjust consumption and investment (consumption and savings) according to household preferences and returns on investment, without which we shall have no clues as to the appropriate share of household income and consumption in the economy.

Without knowing the appropriate ratios, macro policies to increase household income will all be in vain. In an economy where companies are privately owned, residents own stocks and constrain businesses as shareholders and get dividends from the corporate sector. This is the natural form of the market mechanism that regulates consumption and investment. However, privatization is not a viable option for China. The socialist system is certainly an important consideration, but the painful lessons of privatization in the Soviet Union and Eastern Europe are also worth learning.

During the privatization of state-owned enterprises in the Soviet Union and Eastern Europe, although all citizens were, in theory, owners of the enterprises, they were not able to effectively supervise and constrain the enterprises in actual operations and privatization processes. They were "absentee owners". Insiders, therefore, were able to take advantage of the information gap to plunder state assets that should have belonged to all citizens. This "insider control" problem was prevalent in the privatization process of the Soviet Union and Eastern Europe, which ultimately brought about a revel of oligarchs who fed on state-owned assets. For this reason alone, it is imperative that China find ways other than privatization to facilitate consumption-based growth.

"Universal Shareholding Scheme for SOE Stocks" to facilitate consumption-based growth

I suggest facilitating consumption-based growth substantially through a "Universal Shareholding Scheme for SOE Stocks". The goal of the scheme is to build a wealth effect linkage between SOEs and households without overthrowing the state ownership. On the one hand, it will make state assets visible, tangible and useful to ordinary people, so that they can truly feel the wealth effect brought by state assets. To put it more bluntly, it is to make ordinary people have more money to spend because of the existence of state assets. On the other hand, it will form a market-based mechanism that dynamically adjusts the allocation of resources between SOEs and households based on people's current preferences and returns on corporate investments.

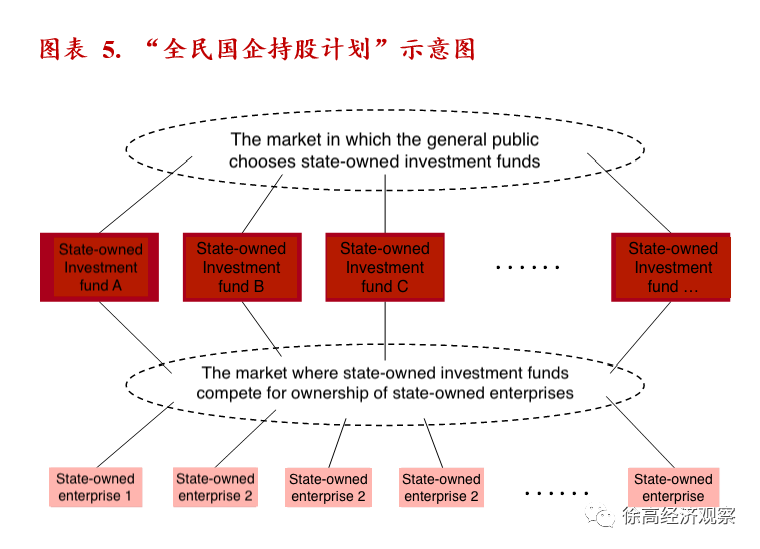

The key to the "Universal Shareholding Scheme for SOE Stocks" is to establish multiple state-owned investment funds. First transfer SOE equity evenly into these funds; then distribute the fund shares evenly to all the people across the country, so that all ordinary people become shareholders. After the initial distribution, the state funds can freely buy and sell state enterprise equity in the state enterprise equity market to obtain the highest possible investment returns. People cannot sell their fund shares at least for a considerably long period of time, so as to prevent speculation on the basis of, for instance, information asymmetry, and thus missing out on the shielding effect of state assets. But every year, people can withdraw dividends from the funds for spending. People can also convert their shares between different state investment funds - from shares in one fund into shares of another fund at any time based on the net value.

[The following graph demonstrates the author's conception of the "two-market" system in the shareholding scheme]

In this "Universal Shareholding Scheme for SOE Stocks", the key lies in constructing two competitive markets. The first market involves state-owned investment funds competing for shares among the general public. The funds must strive to gain public recognition through superior investment performance to expand their scale. Underperforming funds will gradually shed their shares and eventually be eliminated from the market. State-owned investment funds naturally aim to come out victorious in the competition, and as a result, they operate the funds based on the preferences of the general public. When the public desires higher dividends, the funds will distribute more dividends, and when the public needs fewer dividends, the funds will distribute fewer dividends. Through this market, the time preferences of the public can influence the investment behavior of state-owned investment funds.

The second market is the competition among state-owned investment funds for ownership of state-owned enterprises, which is known as the state-owned enterprise ownership market. This market is exclusively open to state-owned investment funds, ensuring that SOEs, although their shares can be owned by individual shareholders, remain state-owned. Within this market, state-owned funds can convey the preferences of the general public to state-owned enterprises, influencing their behavior accordingly. Consequently, when the public senses lower investment returns and desires higher dividends, state-owned investment funds are incentivized to increase dividends. As the owners of state-owned enterprises, state-owned funds then pass on this pressure for increased dividends to the enterprises, prompting them to distribute more dividends.

Through this design, a market mechanism is established to bridge the gap between two major sectors - residents and state-owned enterprises - without altering the latter's ownership. On one hand, this ensures that state-owned assets genuinely create wealth effects for residents, stimulating increased income and consumption. On the other hand, it creates a dynamic resource allocation mechanism between residents and state-owned enterprises, facilitating market-driven adjustments to consumption and investment. Furthermore, the issue of "internal control" can be effectively addressed in this scheme. Competitive state-owned investment funds, acting as a capable and incentivized collective owner, impose strong constraints on corporate insiders. Moreover, state-owned investment funds have greater transparency compared to other enterprises across various industries, thereby reducing the risk of internal manipulation.

Conclusion

The Gross Domestic Product (GDP) of a country is its total income and at the same time its total purchasing power. Therefore, in terms of overall quantity, a nation always possesses the purchasing power to buy all of its output. However, the distribution of purchasing power within a country may not necessarily align with expenditure intentions. There may arise situations where some economic entities have the desire to make purchases but lack the financial means, while others have the financial means but lack the willingness to spend. Hence, the root cause of insufficient domestic demand lies in an income distribution issue, where the mismatch between income and expenditure intentions results in a shortage of overall demand.

The stark disconnect between the two major sectors - residents and enterprises - in our country has led to issues in income distribution. Evaluating economic development based on whether it optimally enhances residents' welfare, we find that both income and consumption among our country's residents are inadequate. Behind this apparent problem lies the weak link between the wealth effects of the two sectors and the absence of a market mechanism for dynamic resource allocation between residents and enterprises. To address the fundamental issue of insufficient consumption and the resulting inadequate domestic demand, the key solution lies in creating a connection between the two major sectors - residents and enterprises. This can be achieved by constructing a market-driven mechanism that prioritizes maximizing residents' welfare when regulating consumption and investment.

Based on this rationale, the introduction of the “Universal Shareholding Scheme for SOE Stocks” is a logical and coherent measure. Through state-owned investment funds, the household sector gains indirect ownership of shares in state-owned enterprises, enabling them to experience the positive wealth effects resulting from the growth of these enterprises. The process involves residents actively choosing state-owned investment funds and engaging in competition for state-owned enterprise equity. This alignment of residents' time preferences with the investment returns of enterprises helps strike a balance, leading to an equitable distribution of income between residents and state-owned enterprises, ultimately promoting the well-being of residents. As a result, the problem of insufficient consumption can be effectively resolved.

The "Universal Shareholding Scheme for SOE Stocks" was first proposed in my 2012 article "Building a Competitive Market for SOE Ownership to facilitate the shift to consumption-based growth". Back then, the constraints on China's macroeconomic policies were not as tight as they are now. While there were criticisms of the model of stimulating growth through investment, views were not as negative as they are today. However, with macro policies now unwilling to stimulate growth like in the past, China urgently needs the "Universal Shareholding Scheme for SOE Stocks" to adjust income distribution within the framework of China's socialist system, fundamentally resolve the issues of insufficient consumption and domestic demand, and rebuild the sustainability of China's endogenous growth.

China's economy currently has three options - best, medium, and worst. The best option is to optimize China's income distribution structure through the "Universal Shareholding Scheme for SOE Stocks" to truly promote consumption-based growth. This will lead China towards a more sustainable growth model that benefits people's welfare even more. The medium option is, without significant changes in income distribution (thus the resident income and consumption remain insufficient), for the government to use financial leverage to create demand in order to stabilize growth. This is not the best path, but it is the constrained optimum under restrictions on income distribution. The worst option is no financial leverage (due to debt concerns), and no adjustments in income distribution. To some, this may seem to allow the market to self-correct and enable the Chinese economy to start over, because after all, "a short-term pain is better than a long-term one". But the good intention will not become reality, as economic slowdown does not automatically translate into improvement in income distribution. In that case, the prolonged deflation, large-scale bankruptcies, and massive unemployment that China experienced from 1998 to 2002 could be repeated.

To maintain the glorious achievements of reform and opening up over the past forty years, China urgently needs the "Universal Shareholding Scheme for SOE Stocks" to truly promote consumption-based growth. And before the shift to a consumption-driven economy makes substantial progress, it is also necessary to correct misperceptions about China's debt situation and for the government to use financial leverage to stabilize growth.

Luo Zhiheng on government debts, fiscal expenditure, and major risks

Luo Zhiheng 罗志恒 is the Chief Economist and President of the Research Institute at Yuekai Securities and one of China’s leading scholars on macroeconomics and fiscal policies. He sat at Li Qiang, Chinese Premier’s roundtable on Jul. 6. Although what he said was not disclosed, the following

These economists spoke to China's Premier on Thursday. What's their view on the economy recently?

During the symposium, experts including Liu Shangxi, Luo Zhiheng, Tian Xuan, Huang Xianhai, Yuan Haixia, Qin Hailin, Lu Ming, and Zhao Wei spoke. The official readout didn’t elaborate on what they said at the meeting, but below are some of what they said recently about the Chinese economy before the meeting.

| A guest post by

|

This economist must have been trained in the US “Chicago school”. I would caution that there are unavoidable political implications, as it will make China’s citizens stakeholders in a capitalist system overnight. It’s a policy pursued by many Western governments (Thatcher government in the UK, Howard government in Australia) and likely contributed to the right ward shift in politics in these countries.

I understand many economists (more inclined to the left) even in the West don’t support this kind of mass privatisation of SOEs. Indeed, privatising Telstra in Australia led to significant regulatory headaches, and the privatised Commonwealth Bank has been closing down branches all over Australia.

We should understand that many of China’s SOE have significant social (non-profitable) functions (like running rail services at or below cost) and other “universal service” obligations. Once these SOEs are privatised, they will come under strong pressure (from shareholders) to shit down unprofitable services and lay off staff, contributing to job insecurity.

Really, if the issue is weak domestic consumption in China, just get the PBoC to issue every citizen with a digital wallet, and make periodic grants or low-interest loans that are targeted at low-income residents or residents in the area of China that are struggling with poverty alleviation. The wealthy in China (like this economist?) do not need free shares to stimulate domestic consumption. It’s far more efficient to target those who are genuinely income constrained, if your goal is to stimulate domestic consumption. You get a bigger “bang” for each yuan spent if it is targeted.

I am not arguing that the PBoC granting digital funds is the best solution to the problem of weak domestic consumption. Just saying it is far better (and more targeted) than simply distributing shares to citizens.