Xiao Geng: financial sector risks and opportunities in China's pursuit of new quality productive forces

Chinese University of Hong Kong Professor says weak RMB & relatively tight fiscal and monetary policies are reducing profits, income, and wealth, contending that finance should serve real economy.

Xiao Geng is a Professor of Practice and Director of the Institute of Policy and Practice, Shenzhen Institute of Finance at the Chinese University of Hong Kong, Shenzhen, and Chairman of the Hong Kong Institution for International Finance. The following is his speech delivered at the IPP Forum of the Future themed "Overcoming the Middle-Technology Trap: Developing New Quality Productive Forces in China" on May 18, with the transcript released on July 24. The forum was convened by Zheng Yongnian, Professor at the Chinese University of Hong Kong, Shenzhen, and President of the Institute for International Affairs, Qianhai.

Xiao explained that despite China's consistent trade surplus and increased RMB purchasing power, the RMB has faced significant depreciation pressure largely due to geopolitical and policy risks, such as U.S. efforts to encourage businesses to withdraw from China.

The Chinese government has struggled to respond swiftly and effectively to these challenges, said Xiao. Unlike the U.S. Department of the Treasury, where "it often takes them just a weekend to resolve issues," said Xiao, Beijing drags its feet.

To address these issues, Xiao believes China must generate controllable financial risks to manage current challenges in the real economy. The current flawed RMB asset pricing mechanism results in inevitable investment losses, discouraging investment from both foreigners and ordinary Chinese. Also, developing the stock market is particularly important for risk management, as it offers an exit for venture capital investments, allowing reinvestment into new high-tech ventures. Echoing many and increasingly more Chinese economists, Xiao says China must expand fiscal spending financed by national debt.

Xiao has kindly proofread our translation.

金融如何促进新质生产力?

How Can Finance Promote New Quality Productive Forces?

New quality productive forces must address uncertainties arising from future geopolitical dynamics and technological revolutions from a national development perspective. This endeavor is challenging, as 99 out of 100 enterprises pursuing these new quality productive forces will likely fail. The central issue is managing the risks, and that's where finance plays a crucial role. However, a common misunderstanding about finance is the overemphasis on risk control by financial practitioners of their financial institutions, leading to substantial profits for banks and securities brokers while the profits and income of the real economy continue to decline; securities brokers earn huge profits, yet retail investors generally incur losses, and the stock market shows little signs of improvement in investment return.

This misunderstanding stems from a misinterpretation of the original purpose of financial risk management, which is to address real-world challenges. Among these challenges, the most critical are national security risks and the health of the real economy, which impacts people's livelihoods. When considering the concept of new quality productive forces and a financially robust nation, it is essential not to view these issues in isolation; instead, a systemic and strategic perspective should be adopted. The essence of a financially robust nation lies in finance serving the real economy which has national security, corporate profitability, and people’s income and wealth at its core.

As I mentioned earlier, a strong financial sector should address geopolitical challenges (such as wars) and the advancements in total factor productivity brought about by technological revolutions by creating controllable financial risks.

Historically, the United Kingdom introduced government bonds to meet wartime needs. By issuing bonds, the government could amass resources in the short term to finance wars, subsequently repaying the debt over twenty, thirty, or fifty years. This mechanism underscores the need for special long-term government bonds without incorporating them into the short-term budget deficit. In the context of competition with the United States, how can China effectively compete if its real economy is underperforming?

The development of the stock market also has historical roots. The Netherlands invented the stock market to support colonial expansion, which entailed immense risks, requiring shareholders to share risks—and profits. Today, while colonialism no longer exists, the stock market's role has shifted to attracting top talent and fostering cutting-edge technology to generate wealth. The U.S. stock market is particularly successful, especially in supporting the tech giants whose stock prices continue to rise, offering extremely high returns.

Currently, the goal of transforming China into a financially robust nation should not focus solely on the safe profits of banks, the robustness of securities companies, or the high income of their employees. Instead, it should be reframed to ensure that finance serves the real economy, including particularly the national security and the well-being of the people.

One issue China currently faces is: Despite the significant GDP growth in China over the past few years, with an average growth rate far exceeding that of the United States, housing and stock prices remain stagnant or falling, and profits and incomes are declining. Why is this happening?

This seems to be a shared responsibility, and various central departments and regions are reflecting on the sluggish real economy. Macroeconomic research highlights the importance of a country's fundamental pricing system for its monetary assets, which depends on the strength of its currency, though often invisible and intangible. Within this pricing system, price levels and exchange rates are crucial. Price levels directly affect the nominal rate of return on assets, while exchange rates determine external purchasing power.

The United States has long pursued a strong dollar policy. When faced with critical challenges, the U.S. Department of the Treasury takes swift measures as seen in their decisive actions during the global financial crisis. It often takes them just a weekend to resolve issues relating to systemic risks. In contrast, China has yet to fully master such measures for dealing with systemic risks, as evidenced by the long-unresolved Evergrande issue.

There has been a significant and persistent problem with China’s macroeconomic policy over the past few years: it has neglected competition with the United States. According to the Law of the People's Republic of China on the People's Bank of China (PBoC), the PBoC is responsible for maintaining the stability of the value of the currency. However, this responsibility assumes that the global reserve currency, the U.S. dollar, maintains low inflation and stable value, an undisputed implicit assumption when the PBoC Law was formulated.

In recent years, however, the United States has experienced high inflation rates and a rapidly declining purchasing power of the dollar in its domestic economy. It means the dollar as China's main international reserve currency is no longer stable and the implicit assumption of a stable dollar in the PBoC law no longer holds. PBoC’s mandate of maintaining low inflation and stable exchange rate with dollar is facing severe challenges, when dollar is no longer stable with high inflation.

In macroeconomics, the real interest rate is a key variable, defined as the nominal interest rate minus the inflation rate. A high real interest rate has a tightening effect on the real economy, and a very low or negative real interest rate strongly stimulates the real economy.

In recent years, China's real interest rates have been exceptionally high, far exceeding historical levels of the past 40 years and significantly surpassing those of the United States. Conversely, the real interest rate in the United States has been very low or even negative due to inflation in recent years, while China has experienced deflation.

High real interest rates in China over the past few years have acted as an invisible constraint on the country's real economy. Many enterprises, local governments, and other sectors lack an understanding of macroeconomics and are unaware that China is actually in an environment of strong macroeconomic tightening for non-financial sector. In such an environment, the rate of return on RMB assets has gradually declined, which could explain why housing prices and the stock prices have been falling in recent years from macro perspective, with asset returns generally getting lower and lower.

Furthermore, the misaligned exchange rate poses another significant problem for China’s economy. According to economic principle, the RMB should have been appreciating relative to the U.S. dollar over the past few years. Why? If you have RMB funds now and are currently planning to purchase real estate or automobiles in China, you will find them cheaper than before, indicating that the purchasing power of RMB is appreciating within China. Conversely, if you earn U.S. dollars, you will find that buying anything in the U.S. has become more expensive due to high inflation. According to the Purchasing Power Parity (PPP) theory in economics, the RMB should have appreciated relative to the dollar. However, in reality, the RMB has not appreciated and is instead facing depreciation pressure in the international foreign exchange market.

Also, for the past dozen years or so, China has consistently maintained a trade surplus, with exports exceeding imports, while the United States has experienced the opposite. According to principles of international finance or international economics, the currency of an exporting powerhouse should appreciate. Yet, in the international foreign exchange market, the RMB is depreciating.

This phenomenon cannot be explained by traditional economic theories but can be understood through the lenses of geopolitical and policy risks.

Geopolitical movements, particularly U.S. efforts to encourage foreign businesses to withdraw from China, directly create immediate depreciation pressure on the RMB. The initial round of RMB depreciation due to foreign capital withdrawal is just the beginning; the second round will be more consequential. Once foreign capital withdraws and the RMB depreciates in the forex market, public confidence will be shaken, prompting individuals to transfer their funds overseas. However, they may not realize that although U.S. interest rates appear higher, the purchasing power of the dollar in the US is continually decreasing.

Without foreign exchange controls, the massive outflow of money would pose a risk to China's financial system.

This chain reaction has led to significant misalignment in China's RMB asset pricing system. On one hand, deflation is caused by excessively high real interest rates, depressing the value of all RMB assets. On the other hand, capital outflow driven by geopolitical tension is triggering short-term RMB depreciation. Both discourages foreign investors from investing in China, as their RMB assets will lose value in a depressed market and when transferred out after a few years when RMB is expected to depreciate. Facing such macro risks, many foreign investors may avoid the Chinese market.

During the Asian financial crisis, then Chinese Premier Zhu Rongji announced that the RMB would not depreciate. This statement stabilized the entire Asian currency market and led to continuous foreign investment inflows into China over the following decades. Foreign investors continued to invest because they believed that the RMB would not depreciate, ensuring that the profits they earned in China would not lose value when transferred out later. Of course, the US-China relation was relatively stable during that period.

Therefore, it is essential to formulate macroeconomic policy from the perspective of national development strategy and geopolitical dynamics, including a stable and sustainable pricing mechanism for RMB assets. Only on this macro basis can the return on investment in the more specific sector, such as high technology and new quality productivity could be effectively supported.

If RMB asset pricing is flawed, investments in RMB asset will inevitably result in losses, and no one, including ordinary Chinese people, will be willing to invest. In such a scenario, encouraging the development of high-tech enterprises becomes very challenging. As mentioned before, among high-tech enterprises, perhaps only 1 out of 100 could succeed while the remaining 99 may fail. Then who should bear this high risk of loss? In the United States, investors worldwide as stakeholders help to share the high risk of high-tech company failures.

Just as Zheng Yongnian (Professor at the Chinese University of Hong Kong, Shenzhen, and President of the Institute for International Affairs, Qianhai) said, venture capital serves as the front-end to the stock market. Without an exit via the stock market, venture capital cannot exist, as its essence is to invest first, go public, cash out through listing, and reinvest in new high-tech enterprises.

Currently, China's high-tech enterprises are facing a fatal blow due to the prolonged slump in China's stock market. To promote new quality productive forces and technological innovation, it is essential to foster the development of the stock market. However, if the development of the stock market is undermined by the flawed pricing of all RMB assets, all efforts in micro and structural areas will be in vain.

The need for changing macroeconomic policies stems from the fact that China must fundamentally leverage financial tools and create controllable financial risks to address the challenges related to the development of the real economy, including the challenges for national security. I will explain this briefly.

Historically, the reduction in transaction costs, transportation costs and the rise of global trade facilitated the division of labour through the global supply chain, which truly drove the technological progress and productivity growth. This background does not require detailed elaboration.

Specialization in the supply chain propelled globalization, and China greatly benefited from it. However, the current issue is the U.S. implementing a "small yard, high fence" strategy and seeking economic decoupling from China. In response, China has started to promote innovation and advancing high-quality productive forces at the global frontier. Given the high risks and high returns involved, risk management becomes crucial.

This is where finance comes in. Its role is to manage risks, not just control them. By creating controllable financial risks over time, finance serves to exchange future risk management time for current surviving space.

In this regard, China has much work to do. Over the past 40 years, China has become a crucial node in global manufacturing. However, as the U.S. seeks to decouple from China, China must innovate independently in technologies that the U.S. is unwilling to provide. While this is challenging, it also presents numerous opportunities.

Take Huawei as an example. If the U.S. had not imposed sanctions, Huawei's HarmonyOS might never have succeeded. The sanctions helped Huawei secure a strong position in the domestic market, which is vast enough to support such a company. This highlights a strategic misstep by the U.S.

The traditional U.S. approach is to impose sanctions and market blockades to pressure rivals, but for China, this approach has spurred the creation and iteration of new markets within China, which may ultimately rival those of the U.S. The U.S. industry is not pleased with this outcome because sanctions result in their losing the Chinese market.

The pursue of new quality productive forces should adopt a strategic and systematic approach.

The competition in new quality productive forces is essentially a systemic competition between two major countries (China and the US). Therefore, China needs to draw on Qian Xuesen's theory of "Open Complex Giant Systems" as an analytic framework. In this giant system, relations of productive factors are key. According to Marxist theory, relations of production factors are as important as productivity, with the core of relations of production being the system of national governance.

The complex system of national governance is too intricate to elaborate on here. It involves an important matrix: the game between the central and macro agencies and the different micro economic segments, which gives rise to the rule system referred to as the property rights infrastructure (PRI). These rules define rights and obligations of market participants. In China, these "segments" are extremely complex, encompassing local governments, businesses, and households. Local governments function both as government institutions and market entities, significantly influenced by central government policies. This kind of influence from central to local is not commonly seen in the more stable local government system of the United States. In China, any changes in central government policies directly affect local governments, enterprises and individuals.

It is important to note that the working mechanisms of Chinese enterprises have already been deeply embedded with the DNA of the global market economy, as seen in the modern corporation system where the legal person has contractual relations with all the stakeholders of the corporation, including shareholders, employees, financers, etc. The efficiency of the team of the corporate stakeholders directly determines the enterprise's asset value and profitability. The corporate legal person's balance sheet reflects not only the assets value but also the liabilities to all stakeholders. Most importantly, the legal person through its contracts links the corporation to the entire market spaces, including local, national, and global markets. China’s reform and opening in the past few decades have helped not only to build a "unified national market" but also pushed progressively its integration into the global market. The family is the fundamental unit crucial for talent cultivation. If financial services fail to support families, talent development will be hindered, impeding the creation of new quality productive forces. Fortunately, the emphasis on education within Chinese families provides a solid foundation for innovation and the development of new quality productive forces.

A critical aspect of national governance is the development of PRI, for all market activities are governed by PRI. It is therefore essential to (1) clearly define property rights and (2) ensure the effective operation of exchange platforms and (3) develop effective dispute resolution mechanisms. These three measures are public services that require government involvement, as the market alone cannot provide these services effectively. China's reforms over the past 40 years have been informed by the PRI models of Hong Kong and Singapore.

Understanding this, it becomes clear that the quality of the market is essentially a reflection of the quality of the government in providing good PRI. When the government excels in these three services, the market naturally performs well. The high efficiency observed in Hong Kong and Singapore is a direct outcome of their effective PRI as the core of governance.

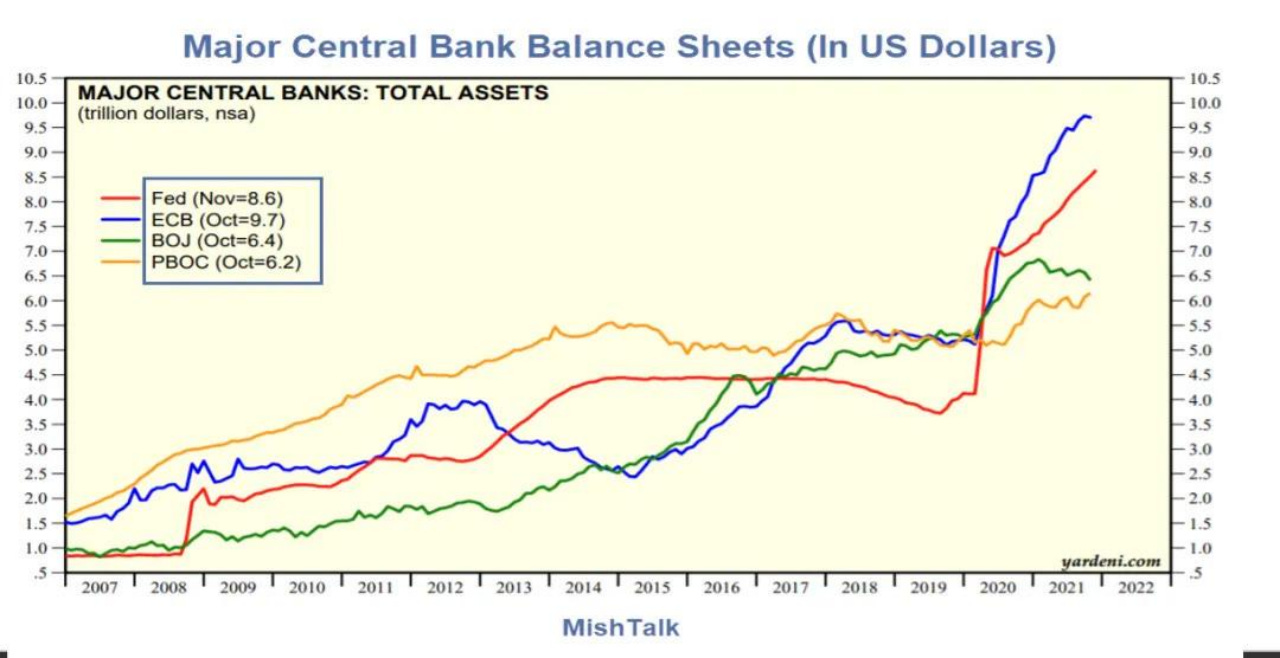

This lesser-known chart is crucial as it illustrates the balance sheets of the world's top four central banks, with the yellow line representing China. Before the pandemic in 2020, the PBoC's total balance sheet was larger than that of the Federal Reserve, the European Central Bank, and the Bank of Japan. This was due to China's substantial fiscal and monetary expansion before 2020 which had facilitated rapid increase in GDP, profits, income, and wealth. However, in 2020, during the pandemic, the global landscape of money supply underwent a fundamental change. The yellow line shows that since 2015, and even as far back as 2012, China has been tightening its monetary scale, a fact largely unnoticed by the country’s micro entities. This tightening is attributed to the effort to offset previously aggressive expansion.

The red line in the chart, representing the Federal Reserve, indicates a substantial increase in money printing in and after 2020. The European Central Bank and the Bank of Japan took similar actions. This reflects how the United States, Europe, and Japan view currency as a strategic tool to address the pandemic, geopolitical challenges, including the Russia-Ukraine war, the Middle East conflict, and the trade war with China. They have truly mastered the art of generating controllable financial risks to resolve current existential risks by supporting their real economy and national security. In contrast, China's response has been noticeably lagging in direction and scale, underscored by the dramatic contrast of this chart.

Since 2000, despite a more than 40% decrease in the purchasing power of the U.S. dollar, its market value outside the US continues to rise.

In the chart below, the blue line represents the rising U.S. interest rates. However, if we look at the red line, which is the real interest rate, it had been declining rapidly after 2020, and even has turned negative for most of 2020-2023, indicating periods of strong macroeconomic stimulation in the United States.

At the same time, China's real interest rates have remained relatively high. While the purchasing power of the RMB has increased within China, China's money supply has remained stagnant relative to its past and to its major peers, which is unfortunate.

The key issue is that while the Ministry of Finance has the ability to issue national debt to deal with current challenges in the real economy, it has failed to act at critical times with significant scales. Currently, ordinary people, businesses, and local governments are all short of funds because of the weak macro conditions, with only the Ministry of Finance has the ability to issue large enough debt and associated stimulative projects. The United States has printed excessively large amounts of dollars and distributed them to its residents to purchase essential goods. China should have the confidence that it could print the RMB similarly to turn around its macroeconomic conditions.

As previously mentioned, China should use future time to exchange for current surviving space, addressing current issues by creating controllable future financial risks. The potential of the PBoC and the Ministry of Finance to turn around China’s macroeconomy is significant because most of the RMB China printed so far was based on inflows of foreign investment, while the RMB printed with national debt issuance has been relatively limited.

The "Greater Bay Area International Economic Cooperation Super Zone" and the "Enterprise Cross-Border Dual Headquarters Operation Mechanism"

Finally, I would like to illustrate how institutional innovation can enhance new quality productive forces with a specific case. Recently, I proposed to Hong Kong government to establish an International Economic Cooperation Super Zone (hereinafter referred to as the "Super Zone") in Hong Kong's Northern Metropolis.

Specifically, as shown in the above chart, the suggestion is to move the Shenzhen River boundary line back a few kilometres south into Hong Kong, transforming the area between the red line and the blue line into a region that is within Hong Kong’s territory but outside its customs area, while simultaneously being outside Shenzhen’s territory but within its customs area. In this Super Zone, the central government and the governments of both regions can consider enacting legislation to implement a special border and customs management model of "inside Hong Kong territory but outside its customs" and "outside Shenzhen territory but inside its customs." This would facilitate the free movement of mainland enterprises and residents to engage in licensed production and consumption activities within the Super Zone.

The rationale for this suggestion is rooted in Hong Kong's historical role as a major bridge connecting Europe/the United States and the Chinese mainland. Looking forward, Hong Kong needs to undertake the role of connecting the Chinese mainland with ASEAN, Mexico, Central Asia, and other regions globally. However, Hong Kong lacks the talent and companies for engagements with countries under the Belt and Road Initiative, as these resources are primarily concentrated in the inland areas of Guangdong or the Yangtze River Delta region. Therefore, a place where such talents can communicate more freely with international investors and corporations is needed.

To support Hong Kong enterprises in developing emerging industries and pursuing cutting-edge technological innovation, the Hong Kong Special Administrative Region (SAR) and local governments in the Greater Bay Area (GBA) can also explore deeper cooperation by establishing a new and pragmatic "dual headquarters" operation mechanism for offshore enterprises around the world.

The vision is for the offshore enterprises registered in the Hong Kong Super Zone to establish a second operational headquarter in designated cooperation zones within the GBA, such as Hetao, Qianhai, Nansha, and Hengqin. GBA local governments, including the People's Government of Shenzhen Municipality, could consider entrusting the Hong Kong SAR Government to oversee these second headquarters' operations. This arrangement would allow both headquarters to be managed under Hong Kong laws and regulations. Tax revenues could be shared between Hong Kong and local governments or re-invested in the long-term construction fund of the Super Zone.

This arrangement effectively extends Hong Kong's management tools into the mainland, creating a chemical reaction. It implies the elimination of customs barriers between the first and second headquarters, similar to a company having two offices in different districts of the same city.

The institutional arrangements of the "International Economic Cooperation Super Zone" and the "dual headquarters" operation mechanism will allow mainland personnel and goods to move freely in and out of the Super Zone. This would significantly reduce operational costs for Hong Kong companies and multinational enterprises registered in Hong Kong, greatly increase the number of market entities served within the zone, and stimulate new productive activities and consumption by mainland residents and enterprises in Hong Kong. This would counterbalance the trend of Hong Kong residents consuming across the border in nearby mainland cities, helping the restoration and maintenance of Hong Kong's fiscal balance as well as industrial development.

Once customs barriers are removed between the Super Zone and mainland cities in the GBA, the movement of personnel and goods between the first and second headquarters will be unimpeded. This is similar to having offices in different districts of the same city, which will effectively expand Hong Kong's physical space for industrial development, truly integrating Hong Kong into the GBA and the national development agenda.

Simultaneously, this will expand the institutional space for industrial development and enhance the degree of internationalization for mainland cities within the GBA since it will attract many multinational companies to establish dual headquarters in the Super Zone and corresponding cooperative areas in the GBA mainland cities. Additionally, this will transform the GBA's development from an over-competitive "either-or" dilemma to a "1+1>2" model of institutional openness and real cooperation.

Establishing a Super Zone in the GBA would be as significant as China establishing the Special Economic Zone in Shenzhen 45 years ago, which helped to transform China from a centrally planned economy to a market economy, as it could help to make Hong Kong not only open to all foreign countries but also open to the Mainland China, greatly promoting the development of Hong Kong and the GBA. This initiative leverages not only Hong Kong's internationally oriented institutions, regulations, management tools but also the infrastructure, industry, and human resources strength of Shenzhen, Guangzhou, and the entire GBA.

This institutional innovation is not just a chemical reaction; it will be a nuclear fusion reaction that will attract global multinational companies, who, by coming here, can gain access to the entire Chinese market while enjoying the stability and transparency of Hong Kong laws, regulations, and industry standards and practices. Top talents will no longer need to work in Hong Kong; they can work for Hong Kong registered international companies while reside at the second headquarter in GBA mainland cities, overcoming Hong Kong's physical space limitations and high costs. If more space is needed, additional second headquarters can be established throughout GBA. This case exemplifies how we can enhance new quality productive forces through quality and practical institutional innovation.

Thank you!

Wu Yongping: An Emerging "Western Bloc" on the Taiwan Question

Issue 3, 2024 of the Reunification Forum, published by the China Council for the Promotion of Peaceful National Reunification, features an analysis of the "Western bloc" on the Taiwan question.

Why RMB internationalization is neither easy nor urgent

The internationalization of the RMB and its perceived challenge to the USD's dominance have been hotly debated topics. However, two prevalent misconceptions persist. The first is an underestimation of the obstacles, and the second is an overestimation of the priority Beijing assigns to this endeavor. These misconceptions are interlinked. While Beijing i…

Who's Afraid of Zichen Wang?

Zichen Wang is the chief editor of The East is Read and the founder of its sister, more prestigious newsletter Pekingnology. As Zichen Wang heads for Princeton, NJ to pursue a Master in Public Policy (MPP) at Princeton School of Public and International Affairs, his presence here will be missed but certainly not gone. For sure, beyond the Pacific and be…

|

|

| A guest post by

|