UNDP Report: Financing the Silver Economy in China

Empowering an Inclusive and Sustainable Ageing Society

The United Nations Development Programme (UNDP) and China Industrial Securities Co., Ltd published Financing the Silver Economy in China: Empowering an Inclusive and Sustainable Ageing Society on 11 December 2025.

Below is the Executive Summary and excerpted report.

Download the full report on the UNDP website.

Executive Summary

Population ageing is one of today’s most pressing global challenges, and proactively addressing it is essential for achieving inclusive growth and sustainable development. An aging population has multiple impacts on development and the SDGs – from a smaller labour force, to a new source of potential sustainable consumption. Policy implications include the impact of increased welfare needs from public finance, along with risks of inequalities widening, including gender divides.

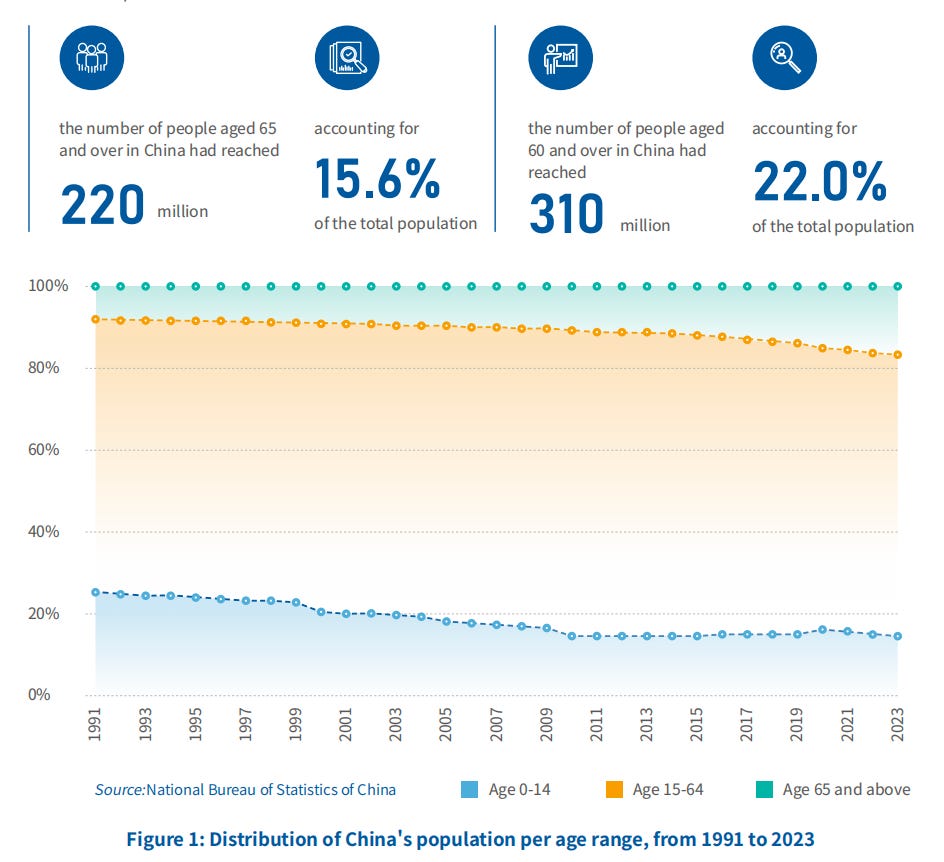

Since becoming an “aged society” in 2021, China’s demographic transition has accelerated. By the end of 2024, the number of people aged 65 and above had reached approximately 220 million (15.6 percent of the population), while those aged 60 and above exceeded 310 million (22.0 percent). Understanding and addressing this demographic shift is critical for long-term sustainable development.

Against this backdrop, the silver economy—comprising economic activities, products, and services designed to meet the needs of the aging population—is growing rapidly and holds significant potential for sustainable economic growth. Valued at around CNY 7 trillion in 2023, China’s silver economy is projected to grow to nearly CNY 30 trillion by 2035, underscoring its vast growth potential. Realizing this, however, requires robust financial support. The Chinese Government has listed “financial services for the silver economy” as one of the “Five Major Areas” of its financial agenda, signalling the vital role of pension and retirement finance in strengthening social security, improving livelihoods and upgrading industries.

This report reflects the diverse and evolving needs of older people and reviews the progress in China’s pension and retirement finance system. It examines how finance can enable the silver economy’s sustainable development, presenting opportunities in two main areas: i) for sustainable investment in the sector and, ii) for contributing to China’s evolving pension and retirement finance scheme.

The report enhances market information for investment opportunities, by exploring innovative approaches to direct financial resources towards areas aligned with sustainable development, using UNDP’s Sustainable Development Goals (SDGs) Investor Map methodology. Six priority investment opportunity areas (IOAs) in the elderly care sector are identified as strongly aligned to the SDGs: (1) smart and wearable devices for older people; (2) digital care service platforms; (3) community-based elderly care and nursing services; (4) palliative and hospice care services; (5) silver tourism; and (6) age-friendly and barrier-free home renovations. These IOAs respond to the increasingly diverse and personalized service needs of older people, while creating new momentum for upgrading the elderly care industry.

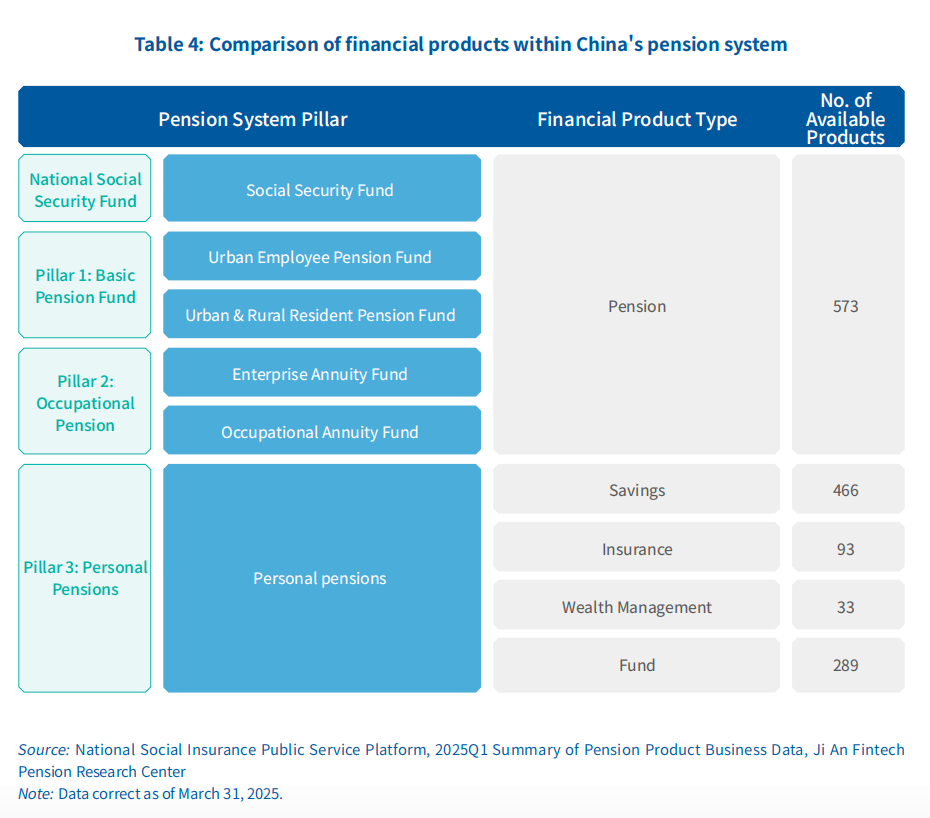

The level of pension and retirement security directly influences older peoples’ livelihoods and consumption power, by meeting their savings, wealth management and risk-sharing needs. As expectations for retirement security continue to rise, the financial sector has a role to play through evolving and innovating pension and retirement financial products. Realising the growing need and limited capacity of public funds in 2022, China launched its third-pillar personal pension scheme. This enables personal pension account funds to be invested in bank wealth management products, insurance products, and public mutual funds, providing participants with flexible, diversified investment channels for allocating pension assets. Drawing on international experience while adapting to its domestic context, China is well-positioned to develop a sustainable and inclusive pension and retirement finance system that strengthens financial security for its ageing population.

Population ageing presents not only a social challenge, but also an opportunity for economic transformation and social innovation. The silver economy—comprising a broad range of consumption and industrial activities serving older populations—offers significant market potential and social value in China. Finance will play a central role in allocating resources and diversifying risk in the process of transformation. It will also be vital to ensuring that such a silver economy grows in an inclusive and sustainable way—prioritizing women, low-income aged populations in rural areas and other vulnerable groups, to “leave no one behind”. Moving forward, collaborations among financial institutions, elderly care providers, government agencies, industry associations, the media, and other stakeholders are essential to strengthening the pension and retirement finance system. Only through cooperation across society can a sustainable silver economy expand, in China and beyond – protecting the planet, and some of its most vulnerable people.

Recommendations for Better Adapting to Demographic Ageing

Promoting high-quality, inclusive, and sustainable development of China’s silver economy will require coordinated action from multiple stakeholders, including financial institutions, elderly care providers, government regulators, industry associations, and media etc. Together, these actors can build a more robust and integrated pension and retirement financial ecosystem that supports both economic returns and SDG targets.

Cross-cutting Needs: Incorporating a Gender Lens in Pension and Retirement Finance

Women and men experience ageing differently, with marked disparities in retirement income, caregiving roles, and financial literacy. These differences should be considered when developing ageing and retirement finance in China’s context.

Caregiving roles. In China, women spend around 2.5 times more hours than men on unpaid care work. This unequal burden may reduce women’s labour force participation, lifetime earnings, and pension entitlements. For many elderly women, the responsibility of raising grandchildren further limits their ability to improve their financial security after retirement. Addressing this requires greater investment in affordable and accessible care services—by both government and the private sector. Many of the IOAs identified in Chapter Two offer opportunities to ease women’s unpaid care burden. Expanding formal care services not only redistributes care responsibilities more equitably across society, but also creates decent jobs in the care economy and professionalizes caregiving as a respected occupation.

Retirement income. Due to accumulated lifetime disadvantages, older women are more economically insecure than men. Evidence shows that among people aged 60 and above, Chinese women’s social pensions are roughly half those of men, primarily as a result of shorter working years, lower wages, and lower coverage of occupational pensions. To close this gap, pension design should explicitly account for such gender disparities. For example, Germany offers pension points for child-rearing during the first three years of a child’s life, allowing those years to count as contribution periods in the pension scheme even if employment is reduced or interrupted as a result of parental responsibilities.

Financial literacy. Gender gaps in financial knowledge are evident among older adults in China, with studies showing women score lower than men of similar age and education on financial literacy tests. This limits women’s ability to plan, save, and invest for retirement. Addressing this requires targeted outreach and training programmes, tailored to older women’s needs and learning styles. Closing the financial literacy gap empowers women to better manage retirement savings, reduces vulnerability to financial exploitation, and enhances autonomy in old age.

In summary, gender is a key cross-cutting factor in adapting financial systems to better support an inclusive and sustainable ageing society. Applying a gender lens—by recognizing unpaid care, closing gaps in pension and financial literacy—will help China create an enabling environment that supports all older people fairly and avoids perpetuating lifetime disparities between women and men.

Government: Creating an Enabling Environment to Attract Long-Term Capital

With its ability to shape both the overall business environment and the policy landscape around the industry, government plays two crucial enabling roles in the development of the silver economy. International experience shows that strengthening the pension system and refining the regulatory landscape are essential to improving the quality of financial services for the ageing population. Policymakers can support this by clarifying regulatory frameworks and industry standards in a way that ensures pension and retirement finance products achieve their intended purposes and protect consumer rights while leaving room for further innovation and experimentation. Through a balanced, innovation-friendly, and prudent supervisory approach, the Chinese government can provide a predictable and supportive business environment for all types of market participants.

At the same time, improving market access and enhancing the broader investment climate is needed to attract more long-term capital to the sector. This includes mobilizing and incentivizing pension funds, insurance funds, and corporate annuity funds to invest in elderly care, and implementing complementary policies that enhance the likelihood of strong investment returns. It also involves implementing changes to the regulatory framework for foreign investment in pension and retirement finance to bring more capital into the sector. In particular, the gradual easing of market entry restrictions and the creation of a fairer and more open market will enhance China’s attractiveness to global institutional investors to help meet the substantial financing requirements of the silver economy.

Financial Institutions: Diversifying Pension and Retirement Finance Supply, Enhancing Investor Education, and Adopting UNDP SDG Impact Standards

With their dual function in supporting the finances of retirees and the services they depend on in retirement, financial institutions are essential to enhancing the financial resilience of older persons and mobilizing investment into the silver economy. Financial institutions should further develop their products and services to better meet the distinct needs of individuals at different life stages. Banks and insurance companies are well-positioned to help individuals prepare for retirement through products like retirement savings accounts, long-term care insurance, and annuities. Meanwhile, security firms provide diverse solutions like target-date retirement funds and retirement-focused investment portfolios that enable retirees to preserve and grow their wealth.

Through innovation in financing instruments, financial institutions also have a leading role to play in the provision of long-term and diverse funding needed to support the development of elderly care services and industries. Instruments such as sector-specific bonds for elderly care projects, asset-backed securities (ABS), and dedicated investment funds are powerful tools for channelling capital into areas such as nursing homes, community-based services, and smart ageing technology. Through participation in international conferences, organizations, and partnerships, financial institutions can also help to attract external investment into China’s elderly care sector to supplement domestic funding gaps.

Alongside these two major directions, financial institutions are also important actors in improving investor knowledge and strengthening consumer protection, especially for older customers. Through community seminars, online education, and other forms of targeted outreach, these institutions can help improve financial planning and risk management knowledge among older populations and empower them to take greater control over their retirement finances and spending. At the same time, financial institutions also have a responsibility to enforce suitability standards, avoid misleading sales practices, and protect customers against financial fraud to safeguard the financial security of retirees.

Financial Institutions are encouraged to adopt the UNDP-initiated SDG Impact Standards as a guide and toolkit to frame their investment mandates, guidelines, and other policies in a way that enables them to operate more sustainably and contribute positively to SDGs by providing diversified pension and retirement finance solutions and enhancing financial education among aged populations.

Elderly Care Providers: Innovating Service Models and Enhancing Financial Integration

As the core service providers at the heart of the silver economy, organizations involved in the provision of elderly care are essential to supply-side development. In order to better cater to the increasingly segmented and complex needs of this growing population, relevant entities should focus on strengthening core competencies by adopting new technologies and attracting skilled professionals to further improve product and service quality.

Given the capital-intensive nature and long-term horizons involved when investing in the silver economy, care providers and other related businesses would benefit from diversifying their sources of funding to reduce dependence on single sources and improve their financial resilience. Specific recommendations include:

1. Leveraging the diversity of capital markets by exploring sources such as equity financing, initial public offerings, and other avenues to raise long-term capital and support ongoing innovation in services and products.

2. Utilizing instruments such as corporate bonds and industry-focused Real Estate Investment Trusts (REITs) to unlock more value from existing assets and ease liquidity constraints.

3. Actively collaborating with financial institutions to explore new integrated models that merge elderly care services with financial products and solutions.

Retirement community operators could also partner with banks, insurance companies and other financial institutions to create products and services that help older people live well. This could include offering loans for eldercare, developing long-term care insurance, and improving reverse mortgage options so older adults can use the value of their homes to support their care needs. Building on lessons from pilot projects, these efforts should combine financial tools with healthcare and daily care services, creating integrated solutions such as “healthcare plus finance” or “housing plus finance” to provide older people with more secure and comprehensive support.

Industry Associations and Media: Strengthening Communication and Public Engagement

Finally, within the pension and retirement finance ecosystem, industry associations and the media serve vital functions as facilitators and communicators. Industry associations, for example, can promote standardization and self-regulation by developing professional codes of conduct, training programs, and platforms for skills and knowledge sharing that support professional development. They can also use their international influence to foster cross-border collaboration and draw on best practices from abroad to continually improve the industry landscape. The media meanwhile can leverage its role as a source of information and a public watchdog to help increase public awareness and acceptance of different pension and retirement finance products and services. In-depth media coverage related to these products and services can help the public better understand market developments and investment risks while raising awareness of potential fraud and consumer rights violations. Media oversight will also help expose market misconduct and defend consumer rights. Through coordinated efforts between industry associations and the media, the sector can facilitate healthy public discourse and a strong market ecosystem that ensures more stakeholders recognize, support, and contribute to the sustainable development of pension and retirement finance and the broader silver economy.

Acknowledgements

We would like to thank the research teams, without which the delivery of this project would not have been possible.

China Industrial Securities Co., Ltd:

Huang Yilin, Wang Bin, Wang Han, Xue Cheng, Xu Yizhou, Wang Yijun, Yang Yating, Yan Xiaoxuan, Pu Zeyun, Yan Haitao, Wang Lianqing, Lu Yanjin, Jia Xiaojun, Zheng Zhaolei and Xu Suoer.

United Nations Development Programme:

Shi Rong, Wang Yali, Wu Lan, Qu Xinyi and Tian Yihan.

The authors would also like to thank Violante di Canossa (UNDP China) for research guidance; Lu Feifei and He Yingming (UNDP China) for inputs and research support; Hu Chen and Zheng Yujing (UNDP China) for research management support; Matthew Walsh for the English translation; and Grace Brown for editing.