Guan Tao on China's Course for RMB Internationalization

Former DG of State Administration of Foreign Exchange talks about the yuan's move from the periphery to the "secondary center" of int'l monetary system: history, opportunities, and challenges

The internationalization of the RMB is a hot topic. Today’s newsletter delves into the issue by presenting the second part of a highly technical videotaped lecture, 推动中国高水平开放的几个理论与实践问题 Several Theoretical and Practical Issues on Promoting China’s High-Level Opening-Up, by Guan Tao, Chief Economist with Bank of China International Holdings Co., Ltd (BOCI) Securities and former Director-General of the Balance of Payments Department of China’s State Administration of Foreign Exchange (2009-2015)

Guan gave the lecture on March 30, 2023, at Tsinghua University. The first part of the speech, on the yuan's exchange rate as an asset price, was published a few days ago in Pekingnology, a sister newsletter.

In the second part, fully translated below, Guan‘s key points include

The euro, not the dollar, has suffered the most in terms of internationalization since the 2008 crisis.

China has transitioned from non-internationalization to internationalization of the RMB through policy changes.

The RMB is now considered a secondary center currency, alongside the euro, yen, and pound.

Further internationalization faces both opportunities and challenges.

Opportunities for the yuan’s internationalization:

China's large and growing economy.

Gradual institutional opening and financial market development.

Increasing awareness of the risks of relying solely on the dollar.

Diversification of the international monetary system.

Challenges:

Network effects and path dependence of existing major currencies.

Smaller size and limitations of China's foreign exchange market.

Gap between China's financial market and mature overseas markets.

Need for further financial market opening and alignment with international rules.

Dependence on China's trade competitiveness and pricing power.

Potential impact of geopolitical tensions and de-globalization.

Overall:

The author argues that the RMB has made significant progress in internationalization and has the potential to become a more prominent global currency. However, there are still challenges to overcome, and the key to success lies in managing domestic affairs well and promoting economic development alongside financial reforms and opening-up.

We should have presented this valuable content, available since 2023, much earlier, but the content remains highly relevant almost a year later.

Please note all "last year” refers to 2022.

My second part discusses the opportunities and challenges of the internationalization of the Renminbi (RMB). It is often mentioned that after the 2008 financial crisis, the Federal Reserve implemented zero interest rates and three rounds of quantitative easing. Many people claimed that the dollar was doomed, its value would inevitably depreciate internationally, and its global status would be shaken. During the COVID-19 pandemic in 2020, when the Fed adopted zero interest rates and unlimited quantitative easing, it was again said that the dollar would enter a mid-to-long-term depreciation trend. However, I want to tell everyone that while subjective wishes are good, what is the objective reality? The results of the International Monetary Fund's Special Drawing Rights (SDR) reviews in 2015 and 2022 show that since the 2008 crisis, the currency that suffered the most in terms of internationalization was not the dollar, but actually the euro.

At the end of October 2015, the RMB was approved to join the SDR basket, becoming the third largest weighted currency with a weight of 10.92%, contributing 0.17 percentage points from the dollar, 1.07 from the yen, and 3.21 from the pound, with the euro contributing 6.47 percentage points.

Last year, after seven years, the valuation was reassessed, and the RMB's weight was increased by 1.36 percentage points, partly reflecting China's rising share in the export market, contributing about two-thirds, and one-third came from the increased use of RMB in financial transactions. We only talk about the increase in RMB weight, but in fact, during last year's reassessment, the weight of the dollar increased by 1.65 percentage points, more than that of the RMB.

Among the five basket currencies, what happened to the other three? The weights of the euro, yen, and pound were all adjusted downwards, with the euro experiencing the largest decrease, by 1.6 percentage points. Therefore, we can see that in both reassessments, the euro suffered more than the dollar. Why is that? In fact, a very important reason is that the status of international currencies is primarily determined by economic strength; a strong economy underpins a strong currency. We only see the Fed's quantitative easing and zero interest rates, but in fact, since the 2008 crisis, Europe and Japan have implemented negative interest rate quantitative easing, going further than the Fed in monetary policy.

We know that the fundamentals of the US economy are generally stronger than those of Europe and Japan. Before the outbreak of COVID-19, the US was experiencing its longest economic expansion post-war until February 2020 when the pandemic led to a brief recession, which was quickly followed by a return to positive growth. What about the eurozone and Japan? Before the pandemic, they were stuck in long-term economic stagnation and deflation. Therefore, concluding from quantitative easing that the dollar would depreciate and its global status would decline is incorrect. From an economic strength perspective, the US still holds a relatively strong position among developed economies.

If everyone pays a little attention, at the end of 2020 and the beginning of 2021, a very popular view in the market was that the dollar would enter a mid-to-long-term depreciation trend. I said at the time that this was incorrect. At the beginning of 2020, when the pandemic caused economic shutdowns and financial turmoil, market panic and a flight to safety briefly drove the dollar above 100, but as the panic over the pandemic gradually subsided after the end of March, the dollar fell, depreciating in 2020. I pointed out at the time that while the supporting role of safe-haven sentiment for the dollar weakened in 2021, whether the dollar would rise or fall in 2021 depended on whose economy recovered faster post-pandemic. In hindsight, the dollar did not weaken as the market had imagined in 2021 but rebounded by 6.7%, because the global economy experienced a V-shaped rebound post-pandemic, with the economic recovery in developed economies outpacing that in emerging markets, except China. Within developed economies, the US led in economic recovery, hence the appreciation of the dollar. The Fed did not raise interest rates in 2021, only starting to taper bond purchases at the end of the year, while the Bank of England began raising interest rates. Therefore, monetary policy alone cannot determine whether exchange rates will rise or fall, nor can it predict the impact on the international status of currencies.

Previously, I mentioned that a hot topic in the market last year was the reduction of US Treasury bonds by foreign investors. According to the US Department of the Treasury's report on international capital flows, by the end of last year, foreign holdings of US debt amounted to $7.34 trillion, a decrease of $426 billion from the previous year. Many people believe that foreign investors sold off $426 billion. This is incorrect, as we need to clarify the concepts of stock and flow in the balance of payments. Foreign holdings of US debt are a stock measure, which includes the impact of valuation factors. What was the situation last year? Last year, foreign investors cumulatively net-purchased $716.6 billion in US Treasuries, second only to the $724.4 billion in 2008. But why did it appear that foreign holdings of US Treasuries decreased? A significant reason is that inflation in the US led to rising Treasury yields and falling bond prices, requiring market value adjustments for stock measures, resulting in a negative valuation effect of $1.14 trillion. Some explain this as passive selling or reduction, which is somewhat far-fetched. For example, if the overall stock market is down, and the market value of the stocks we hold shrinks, it's not appropriate to say we've passively sold a certain amount of stocks. After clarifying the concepts of stock and flow, we find that the dollar is not as weak as many think. So far, the global challenge has been a dollar shortage, not a dollar disaster.

Many people are concerned about China's holdings of US Treasuries. China's holdings of US Treasuries last year decreased by $173.3 billion from over $1 trillion to $867.1 billion, leading to heated discussions about China selling off US Treasuries. What's the actual situation? From a flow perspective, last year China only net-sold $28.5 billion in US Treasuries, a 77% decrease in the scale of reduction from the previous year, 35% less than Japan's reduction during the same period. Our reduction in US Treasuries was mainly due to the negative valuation effect of $144.8 billion caused by falling Treasury prices. Importantly, after reducing holdings of US Treasuries, Chinese investors increased holdings of US institutional and corporate bonds. Last year, Chinese investors net-purchased $96.7 billion in US bonds (sum of Treasuries, institutional bonds, and corporate bonds), actually increasing exposure to the US, while Japan net-reduced its holdings of US bonds by $10.8 billion during the same period. So, we must clearly understand the basic concepts to prevent overinterpretation and avoid misjudgments. Many Chinese experts exhibited unnecessary worries about the US, saying no one wants U.S. assets, so the U.S. should be careful. But in fact, last year the world bought $1.67 trillion in US securities, including over $700 billion in US Treasuries.

When it comes to the internationalization of the RMB, I think looking at a currency's internationalization requires examining both policy and market factors. In terms of policy, China has already completed the transition from non-internationalization to internationalization of the RMB. Before the reform and opening up, China implemented a planned economy with a highly centralized foreign exchange management system, where the RMB's non-internationalization was an important part of strict foreign exchange controls. China neither allowed the RMB to be used for cross-border pricing and settlement nor permitted the entry and exit of RMB cash, which were important components of foreign exchange controls. However, after the reform and opening up, as the RMB's convertibility improved and capital account openness increased, China gradually relaxed restrictions on carrying RMB cash across borders, a change made in the 1990s. At the beginning of this century, China began encouraging the use of bilateral local currencies for pricing and settlement in border trade. At the end of 2003, the Chinese mainland launched a pilot project for personal RMB business in Hong Kong.

Hong Kong is a free financial market without foreign exchange controls, so there are no restrictions on which currency to use for pricing and settlement. However, before the end of 2003, without a formal banking clearing channel, RMB transactions between Hong Kong and the mainland were “fast in and fast out, with large flows but small stocks.” Because after Hong Kong banks accepted RMB deposits, they couldn't exchange them for HKD on the mainland, and the RMB deposits couldn't be transferred to the mainland, resulting in large flows without stocks. We launched the Hong Kong personal RMB business pilot at the end of 2003, for the first time using a formal banking clearing channel to regulate cross-border RMB circulation and use. And I think that was a significant attempt to use market-based means to transmit some of the capital and foreign exchange control requirements from the mainland to Hong Kong, a free financial market.

How did we do it at the time? We said that Hong Kong could handle RMB exchanges, deposits, and remittances, but we required limits. The Hong Kong regulatory authority said we are a free market, we can't set limits, at least not by issuing a notice from the HKMA saying, for example, that only 20,000 RMB worth can be exchanged per day, and only 50,000 RMB worth can be remitted; you can't do that.

But how did we solve it? We used market-based means, signing a clearing agreement with Bank of China Hong Kong, which included rights and obligations. Its obligation was to implement our limit management regulations, and its right was to exchange the RMB collected in Hong Kong for USD or HKD at the onshore RMB exchange rate and bring it back to Hong Kong, and the RMB deposits collected in Hong Kong could be transferred to the mainland. Bank of China Hong Kong, with our clearing agreement as the master agreement, would sign clearing agreements with Hong Kong RMB business participating banks. Hong Kong banks could freely choose whether to sign the agreement. If they signed a clearing agreement with Bank of China Hong Kong, they had to follow the limit-management regulations, and then the deposits collected could be transferred to Bank of China Hong Kong, which would then transfer them to the mainland, where the mainland would pay interest to Bank of China Hong Kong, which in turn would pay interest to the Hong Kong RMB business participating banks, which could then pay interest to depositors. The RMB collected by the Hong Kong RMB business participating banks could be sold to the Bank of China Hong Kong, which would then sell it to the mainland.

The HKMA would check whether the Hong Kong RMB business participating banks were following the clearing agreement, and if not, the HKMA could penalize them for being imprudent in their operations, thus forming a regulatory closed loop. We used market-based means to transmit some of the mainland's regulatory requirements to Hong Kong's free financial market. So, we can see that many things are not about whether to regulate or not, but how to regulate, as regulation requires art and skill.

2008 was an important starting point because the US subprime mortgage crisis evolved into a global financial tsunami, shaking confidence in the U.S. dollar. The Bank of Korea proposed a bilateral currency swap with China, marking an important starting point for the internationalization of the RMB. A milestone was the launch of the cross-border trade RMB pricing and settlement pilot at the end of 2009 (2008?), accelerating the pace of RMB internationalization.

In July 2010, the People's Bank of China and Bank of China Hong Kong revised the RMB business clearing agreement. The agreement stipulated that if the RMB was only used locally in Hong Kong, the mainland would not intervene, and local operations could handle related business; The mainland would only intervene in cross-border transactions between the mainland and Hong Kong. This essentially gave the RMB in Hong Kong significant room to circulate and be used. It was against this policy backdrop that the offshore RMB foreign exchange market in Hong Kong emerged.

At the end of 2014, the Central Economic Work Conference for the first time included the gradual promotion of RMB internationalization in a Communist Party of China (CPC) document. Previously, there was no mention of RMB internationalization; according to (former People’s Bank of China) Governor Zhou Xiaochuan, it was referred to as the 人民币在贸易与投资中的跨境使用 cross-border use of the RMB in trade and investment or 跨境人民币业务 cross-border RMB business.

Before 2014, China’s official documents did not mention RMB internationalization, although there was much discussion in non-official circles, but not officially. At the end of 2014, the Central Economic Work Conference first proposed "gradually promoting RMB internationalization," and at the end of 2015, the Fifth Plenary Session of the 18th CPC Central Committee included "gradually promoting RMB internationalization" in the "13th Five-Year Plan." In January 2018, the "Notice on Further Improving RMB Cross-Border Business Policy to Promote Trade and Investment Facilitation" stated that all cross-border transactions legally eligible for foreign exchange settlement could use RMB settlement. At the end of 2020, the recommendations for the "14th Five-Year Plan" from the Fifth Plenary Session of the 19th CPC Central Committee proposed "cautiously advancing RMB internationalization." So, we can see that China, unlike many countries, gradually promoted currency internationalization through explicit state policies, although the terminology used for RMB internationalization varied at different stages, initially "gradually advancing" and later briefly changed to "cautiously advancing."

Even if policy encourages currency internationalization, whether a currency is internationalized still depends on its acceptance and recognition internationally. There's a common view in the market that after the RMB exchange reform on August 11, 2015, RMB internationalization regressed, which is a misunderstanding. Why? In fact, after the exchange reform on August 11, 2015, there was a major adjustment in the strategy for RMB internationalization. Before that, onshore regulation was strict, our financial markets were not open, and if you wanted to hold RMB financial assets, you could only make RMB deposits in Hong Kong or buy Dim Sum bonds there. However, after the exchange reform on August 11, 2015, we accelerated the opening of the onshore financial market, allowing direct purchases of stocks and bonds domestically.

By the end of last year (2022), the share of stocks and bonds in foreign holdings of domestic RMB financial assets reached 69%, up from 27% at the end of 2014. Why? Before 2014, if you wanted to hold RMB financial assets, you could only do so in Hong Kong, where Hong Kong absorbed non-resident RMB deposits and then transferred them to the mainland or made loans there, so before 2014, foreign holdings of RMB financial assets were mainly in the form of deposits and loans. However after the exchange reform on August 11, 2015, with the opening of the onshore financial market, everyone could hold stocks and bonds - a significant change.

Moreover, we see that the degree of acceptance and recognition of RMB internationalization internationally is increasing, with the RMB becoming the second largest cross-border payment currency domestically from 2011, the fifth largest reserve currency, foreign exchange transaction currency, international payment currency, the second largest trade financing currency, the sixth largest international banking liability currency, and the tenth largest international bond and securities currency.

If we categorize the international monetary system into center and periphery, the RMB is moving from the periphery towards the center. If we further differentiate into center currency, secondary center currency, and peripheral currency, the RMB has now entered the second tier, that is, a secondary center currency, similar to the euro, yen, and pound. Of course, we are mainly large in volume, and the quality of internationalization still lag behind traditional major international currencies.

We've already talked about how, from a policy perspective, the RMB has completed the transition from non-internationalization to internationalization, but many countries, such as Singapore, restrict currency internationalization. Why? An important reason for Singapore is that it's a small open economy, and if its currency becomes internationalized, large inflows and outflows of capital can easily cause significant fluctuations in local financial asset prices and exchange rates, so they are reluctant to actively promote currency internationalization.

But China is different; it's a large country. Last year (2022), the RMB exchange rate fluctuated significantly, fully demonstrating China's ability as a large open economy to withstand risks. In 1998, China's capital account (including net errors and omissions) deficit was $25 billion, equivalent to 2.4% of GDP. In 2022, the capital account (including net errors and omissions) deficit was $317.6 billion, only equivalent to 1.8% of GDP. This reflects that as the economy's size increases, its capacity to absorb shocks significantly strengthens.

Moreover, because we have a large financial market size in the onshore market, our ability to absorb various shocks has also significantly strengthened. As we mentioned earlier, before the exchange reform on August 11, RMB internationalization was mainly driven by the offshore market, with a large amount of financial assets held overseas in the form of RMB deposits. When the RMB unexpectedly weakened at the time of the exchange reform, it led to a decline in Hong Kong's RMB deposits, resulting in significant depreciation pressure on the offshore RMB exchange rate, which also intensified depreciation expectations for the onshore RMB exchange rate.

What was the situation last year (2022)? Last year, in February and March, Hong Kong RMB deposits decreased by over 100 billion RMB per month, and we were still discussing the "strong dollar, stronger RMB" market, because at the end of February, when the Russia-Ukraine conflict broke out, the dollar appreciated as a traditional safe-haven currency, and most non-dollar currencies depreciated against the dollar, but the RMB remained strong relative to the dollar. We were even speculating at the time that the RMB was a safe-haven currency. This example is to illustrate that the offshore market has limited capacity and prices can experience significant fluctuations, but even now, with foreign holdings of onshore RMB financial assets far exceeding the offshore market, due to the larger capacity of the onshore market, it's difficult for foreign capital to cause significant turbulence.

In the past, people often said that domestic asset prices in China were relatively high, and if we open up, there will be a large outflow of capital. But in fact, the experience of two-way opening in recent years shows that this view does not hold. Domestic investment preference exists after capital account opening. The most typical example is the simultaneous opening of northbound and southbound funds through the Mainland-Hong Kong Stock Connect. Although for various reasons, the cumulative net purchase volume of the Hong Kong Stock Connect (southbound) is slightly larger than that of the Shanghai and Shenzhen (northbound) Stock Connects, the gap is at most five or six hundred billion RMB, and this is the cumulative gap from 2014 to now, without the situation everyone was worried about occurring. The underlying reason is that after a capital account opening, investors have a domestic investment preference. Now that we open our doors and allow domestic investors to buy US and Hong Kong stocks, many investors are thinking hard about whether they have the ability to make money in those markets. So, we gradually accumulate experience through channel-based, gradual opening, becoming more and more confident in opening up.

At the end of 2020, the proposal for RMB internationalization at the Fifth Plenary Session of the 19th CPC Central Committee was "cautiously advancing RMB internationalization." But two years later, after experiencing significant fluctuations in the RMB exchange rate last year, the expression changed to "orderly advancing RMB internationalization" at the 20th National Congress of the CPC. "Orderly" compared to "cautious," I think, is more positive in policy because "cautious" means being both prudent and careful, while now we need to coordinate development and security, which is called "orderly advancing."

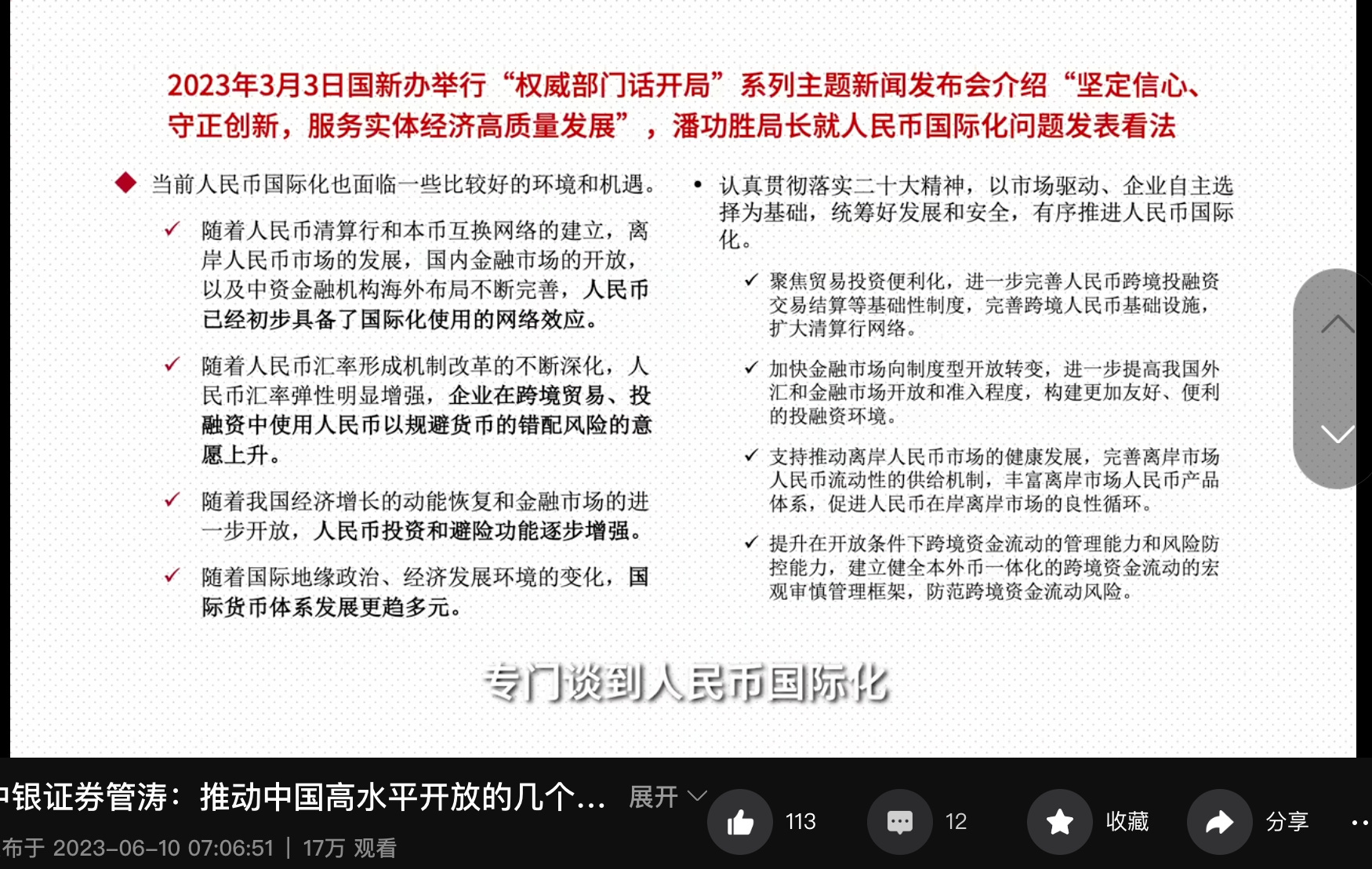

At the press conference of the State Council Information Office on March 3 this year, Mr. Pan Gongsheng, the head of the State Administration of Foreign Exchange [Zichen’s note: now the Governor of China’s central bank], specifically talked about RMB internationalization. He mentioned that RMB internationalization currently faces a good environment and opportunities, including the RMB already having a preliminary network effect for international use, enterprises' increasing willingness to use the RMB in cross-border trade and investment financing to avoid currency mismatch risks, the gradual strengthening of the RMB's safe-haven function, and the diversification of the international monetary system. He also talked about what to do next, including improving the financial infrastructure for RMB internationalization, expanding the clearing bank network, promoting the transition of financial markets to institutional opening, supporting the development of the offshore RMB market, and enhancing the management and risk prevention capabilities for cross-border capital flows under open conditions.

In my personal understanding, the following opportunities exist in the next step of promoting RMB internationalization:

First, China has a systemically important economic and financial system. You can't say you're an international investor if you don't invest in China. I believe that as long as China's economy does not encounter problems, RMB financial assets will still be very attractive to foreign investors.

Second, the report of the 20th National Congress of the CPC once again emphasized the gradual advancement of institutional opening, which is an important content of China’s high-level opening, that is, our transaction rules and regulatory rules will gradually align with the highest international standards.

Third, in recent years, we have gradually increased the marketization of the exchange rate, giving us more confidence and foundation in RMB internationalization. Just now I have repeatedly emphasized that rigid exchange rate arrangements and financial opening are dangerous policy combinations, but now we have overcome this hurdle.

Fourth, China has insisted on implementing normal fiscal and monetary policies in recent years, which helped increase the credit of the RMB. Especially recently, due to the rapid inflows and outflows from the previous US fiscal and monetary stimulus, the recent turmoil in the European and American banking sectors has faced backlash from previous liquidity injections. I believe the aftermath of this incident has not passed, and everyone will have deeper thoughts on the macroeconomic policies of these developed countries. In this round of crisis response, the policies of the Chinese government have been relatively successful.

The last is the multipolar development of the international monetary system. From an economic perspective, it means the United States' position in the international economy and trade is declining, but the international community's dependence on the dollar is still too great, causing the Federal Reserve's monetary policy, whether loose or tight, to have huge spillover effects. This round of aggressive rate hikes by the Fed not only caused great harm to emerging markets and developing countries, but developed economies also suffered a lot. Why did the ECB eventually follow up with rate hikes? Christian Lagarde clearly stated last (2022) July that one important reason was the euro's excessive depreciation against the dollar, which, combined with the rise in commodity prices, increased the eurozone's imported inflation pressure. Japan, which had not intervened for many years, also intervened in the market in September and October last year (2022) due to imported inflation pressure. This largely reflects the risks brought by the Fed's monetary policy. In recent years, some major reserve currency-issuing countries have weaponized their currency, also shaking the credit of the international monetary system.

But we must also see that challenges objectively exist.

First, the international monetary system has network effects and path dependence. Once people form a habit of using a certain international currency, they will not easily change this habit, and the more that currency is used, the lower the transaction costs, posing a significant challenge to later emerging international currencies.

Second, China's foreign exchange market is relatively small, and institutional arrangements need to be improved. Although last year's global foreign exchange market survey showed a significant increase in RMB foreign exchange transactions, it is still smaller than the main international currencies, and the variety is not rich, with many restrictions.

Third, currency internationalization needs to provide convenience and attract people to hold RMB financial assets, but there is a relatively large gap between China's financial market and overseas mature markets.

Fourth, China's financial market opening needs to be further improved. Institutional opening needs to align with the highest international economic and trade rules. The highest rule for capital account opening is a negative list, which we cannot achieve in the short term, but at least what we should do is not easily retract opening policies, which requires raising the legislative level to gain market trust. Everyone is worried that a "red-headed document" or even a window guidance could decide the fate of a transaction, which would affect confidence in RMB financial assets.

Fifth, using local currency for pricing and settlement in cross-border trade depends on our competitiveness and pricing power in trade, which presents a significant challenge for us.

In addition, as we mentioned earlier, the multipolar development of the international monetary system is both an opportunity and a challenge for RMB internationalization. Currently, there is a trend of intensified competition among major powers and the risk of de-globalization and de-sinicization, which at certain times and in certain aspects can also affect people's choice to hold RMB financial assets.

The main conclusion of this part is that we must soberly recognize that over the past decade, the international currency whose status has been most affected is the euro, not the dollar, which has not declined but actually increased, especially last year when the global market faced a triple hit in stocks, exchange rates, and bonds, resulting in a dollar shortage rather than a dollar disaster.

Second, as a large open economy, China has already completed the policy transition from non-internationalization to internationalization of the RMB, and in recent years, the international acceptance and recognition of the RMB have continuously increased. The most important thing for the RMB is to consolidate and enhance its position among secondary center currencies.

The last is that orderly advancing RMB internationalization faces both opportunities and challenges. The key is to do our own things [manage our domestic affairs] well, with the primary task being to keep the economy operating within a reasonable range. A strong economy underpins a strong currency. We should not internationalize for the sake of internationalization; we must make internationalization serve domestic reform and opening up and economic development. Of course, we also need to improve macroeconomic governance, vigorously develop the domestic financial market, and steadily promote institutional opening.